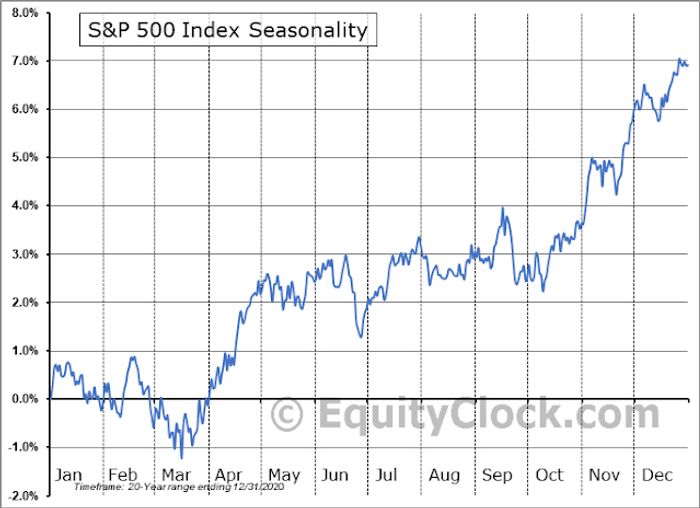

What are the odds of a melt-up for U.S. stocks for rest of 2021? If history is any guide, stocks can be expected to bottom in early October and begin a period of seasonal strength into year-end.

Ned Davis Research recently sketched a bullish scenario into year-end for global equities by pointing out that the fourth quarter has been the strongest over the past few years.

Risk appetite indicators have been steadily improving, but haven’t risen sufficiently to flash a buy signal just yet. These readings are consistent with my fourth-quarter sector review, which also found signs of cyclical and reflation strength, but no broad-based confirmation.

Supportive sentiment

The sentiment backdrop is becoming more supportive of an advance, though readings haven’t fallen to panic extremes. For example, the NAAIM Exposure Index, which measures the sentiment of registered investment advisers, plunged recently but didn’t break the 26-week Bollinger Band. A penetration of the low Bollinger Band has been a strong buy signal in the past.

These conditions lead me to believe that risk/reward in U.S. stocks now is tilted to the upside. The maximum drawdown of the S&P 500

SPX,

from its highs is -5%. It’s conceivable that stocks could pull back, but another 2%-3% of weakness is likely to spark panic levels in many sentiment models. While I am cautiously bullish, I am not ready to go all-in just yet.

Supply chain bottlenecks

Won’t rising energy prices create inflationary pressure and force the Fed to act? Fed Chair Jerome Powell testified that inflationary pressures were expected to be transitory because of supply chain bottlenecks, but allowed that the transitory period may last longer than expected.

The headlines may see rising hysteria over shortages in the coming weeks as Christmas nears and products aren’t available in plentiful supply. In reality, the shortages are attributable to a supply shock owing to rising demand in the face of limited manufacturing and transportation capacity. Central bankers raising interest rates won’t make the semiconductor shortage go away, nor will it expand shipping and trucking capacity.

Although there are many bottlenecks, in particular in transporting materials to factories, and goods from factories to sellers, orders for goods that will last a (relatively) long time continue to get better. There is simply no downward pressure on the producer sector of the U.S. economy at this time.

The next important data release will be the November jobs report. How will the juxtaposition of COVID cases, the expiry of emergency assistance programs, supply chain bottlenecks, and widespread reports of labor shortages affect the employment situation? Powell stated after the last FOMC meeting that it would take a large miss on the November report for the Fed to rethink its plans to taper its QE purchases. This is what reflation looks like.

Fiscal wild cards

On the other hand, investors will have to deal with the confusing fiscal picture out of Washington. This time, there are simply a lot of balls in the air and many moving parts to fiscal policy. Each issue is separate but related and any one of them could go off the rails and affect fiscal policy and unsettle the markets.

- Funding the federal government, which can be done with a Continuing Resolution in the short run

- The debt ceiling

- The infrastructure bill

- The budget reconciliation process.

Here is how President Joe Biden’s proposals could affect future policy and change the lives of Americans:

- Transportation: Electric vehicle (EV) subsidies, spending for EV infrastructure like public charging stations, public transport subsidies, especially for rail travel.

- Healthcare: Expand Medicare coverage to dental, vision, and hearing benefits, free Medicaid coverage for more lower-income Americans, lower drug prices.

- Child care and education: Free day care for lower-income Americans, two years of free preschool before kindergarten and two free years of community college, and 12 weeks of paid family leave to tend to a sick family member.

I have no idea of how this wish list will play out in the tug-of-war in Washington. Make no mistake that the legislative skills are there for a deal to be done. House Speaker Nancy Pelosi is a vote counter par excellence, Democratic Senator Majority Leader Chuck Schumer understands his caucus, while Biden enjoys wide approval among Democrats and has a strong legislative record in the Senate.

In all likelihood, the Democrats’ ambitious agenda will be watered down. As an example, Biden’s original proposal was to raise the corporate tax rate from 21% to 28%, though expectations were scaled back to 25%. PredictIt odds show that the chances of no tax increase or a sub-25% tax rate are rising. As a 25% rate has been largely discounted by the market, a lower tax rate would be a welcome surprise for equity investors.

Putting it all together, the stock market may be setting up for a period of positive seasonality into year-end, which would be sparked by a reflationary boom. Yet a number of important cyclical tripwires have not been triggered. At a minimum and in the short-term, the S&P 500 needs to rally and regain its 50-day moving average as it tests the Evergrande-panic lows.

Cam Hui writes the investment blog Humble Student of the Markets, where this article first appeared. He is a former equity portfolio manager and sell-side analyst.

Also read: September was a terrible month for stocks. Here’s what you can expect in October.

More: Evergrande crisis and the U.S. debt-ceiling showdown could give stock investors a buying opportunity

This post was originally published on Market Watch