The fate of this year’s wild bank stock rally may depend on whether the major U.S. banks manage to show signs of increased loan activity in their third-quarter results that kick off next week.

With the prospect of rising interest rates helping banks widen their net interest margin — the profits they make on lending — bank stocks have outpaced the broader market all year.

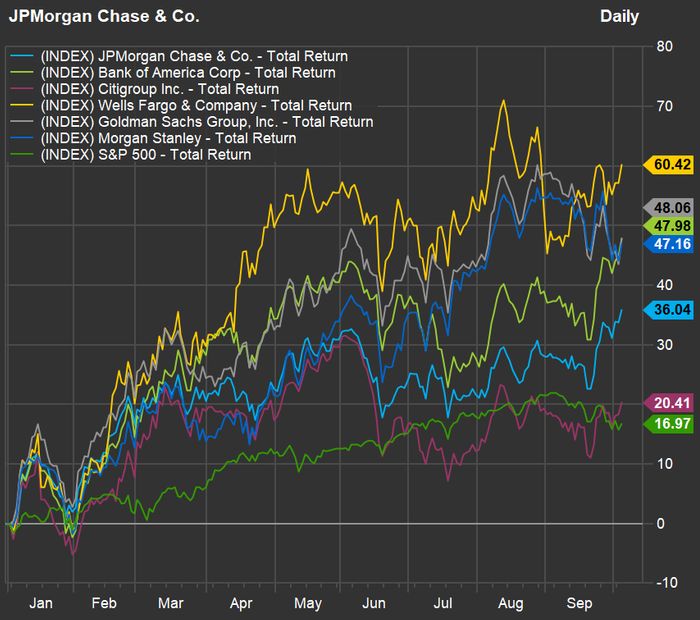

Source: FactSet

As of Wednesday’s close, JPMorgan Chase

JPM,

is up 33% in the year to date, while Bank of America

BAC,

has advanced 46%, Goldman Sachs

GS,

is up 47%, Morgan Stanley

MS,

has jumped nearly 45%, Wells Fargo & Co.

WFC,

has rallied nearly 59% and Citigroup

C,

has posted a more moderate gain of nearly 18%. By contrast, the S&P 500 is up by 16.2% this year.

Signs of an interest rate increase remain sketchy, however, as the Fed continues to signal a tightening cycle at some point, while economists predict it may happen sooner rather than later. But with the economy picking up from year-ago levels, banks have been relative darlings on Wall Street as they recovered from their 2020 losses during the COVID lockdown. Investor optimism around bank and other stocks has been under the microscope of late, however, with big selloffs in some sessions.

Wall Street targets for banks

With earnings now on tap for the megabanks as shown in the chart above, investors would do well to view per-share earnings carefully, because banks have been shifting loan loss reserves that they built up in the early days of the COVID pandemic to their bottom line as the economy has improved. This practice allows banks to operate within regulatory boundaries around loan loss reserves, while providing a lift to beat their quarterly EPS estimates.

See now: Bank stocks are cheap — here are the 20 best players in the industry

“Last year, they wrote a big number in for loan loss reserves and this year, they assume the economy is soaring, so they write a small number of loan loss reserves,” said bank analyst Dick Bove of Odeon Capital Group. “This in turn gets reflected in a big EPS number.”

Analysts and investors appear to be aware of that move, however, since the stock prices of big banks failed to pop significantly after they reported second-quarter earnings three months ago.

A big challenge facing banks is whether they can show an uptick in loan activity as they lose market share to non-bank lenders, while consumers have been avoiding additional debt outside of brisk auto purchase activity.

“So far this year, the banks haven’t been increasing their lending to businesses or, in fact, to the home mortgage market,” Bove said. “Their holdings of these two loan portfolios, which represent 44.4% of their total loans, are down in both cases. The story is more positive in the consumer loan sector due to the surge in auto loans. However, when all portfolios are considered, bank loans are down today versus a year ago.”

On the bright side, however, banks more focused on capital market underwriting and advisory services for mergers and acquisitions remain in a stronger position against a background of record deal-making. This trend helps banks such as JPMorgan Chase, Morgan Stanley and Goldman Sachs as dominant names in these arenas, with exposure as well by Bank of America’s Merrill Lynch unit, Bove said.

For its part, Edward Jones has three bank stocks on its focus list: Bank of America, JP Morgan Chase and regional bank Truist

TFC,

Edward Jones banking analyst James P. Shanahan said BAC is more attractive because it is well positioned to benefit from rising interest rates. JPMorgan Chase stands out for its diversification, including strong contributions from markets-related activities, while Truist offers value relative to its peers.

“In our view, the biggest catalyst for the banks is loan growth, particularly commercial loan growth, followed by rising interest rates,” Shanahan said. “One of the biggest challenges for the banks is that they had credit costs coming out of the pandemic, and they unwound that, so the reserves weren’t needed. As we got later into the recovery, the focus shifted to deposit growth and excess liquidity.”

With corporations issuing bonds instead of taking out loans, and consumers using stimulus money to pay down credit cards, banks have faced downward pressure on loan growth.

See also: Home equity has hit a record high. How can you best take advantage of your home equity gains?

“The banks would do better if they could redeploy low cost deposits they raised during the pandemic into higher yielding loans,” Shanahan said.

However, big companies may be nervous about borrowing and investing in plant equipment due to uncertainty about the Delta variant, concern over rising interest rates, as well as potential tax law changes from Congress.

Households remain cautious as they face high unemployment relative to pre 2020, but it is possible that consumers will start to use their borrowing capacity on credit card and companies will start to borrow at a healthier pace in late 2021 or next year.

See: Affirm’s ‘super-app’ ambitions win praise as company plots debit, crypto moves

Among the six megabanks, analysts continue to bestow the most buy ratings on Goldman Sachs and Morgan Stanley, with 17 buy ratings each, followed by 16 buy ratings for Citi, 15 buy ratings for JP Morgan Chase, and 11 for Wells Fargo, which has been plagued by the most regulatory problems of the major banks.

Citigroup stands out as the most affordable bank stock as it’s trading at 0.8 times its book value, the lowest multiple among the six megabanks, according to FactSet Data. Its forward price to earnings ratio of 9.7 also ranks as the lowest, followed closely by a 9.8 for Goldman Sachs as of Monday’s close. Bank of America’s 15.3 forward price to earnings ratio ranks as the highest in the group.

Don’t miss: Citizens is shedding ‘Bank’ from its name as it stretches beyond its regional roots for a national presence

Oppenheimer analyst Chris Kotowski said the firm’s recommended list for banks includes Bank of America, Citigroup, Goldman Sachs, Jefferies

JEF,

and U.S. Bancorp

USB,

The large banks covered by Oppenheimer have been yielding an average of 2.4% versus 1.3% for the S&P 500, he said. Either looking back by 10 years, five years, or three years, banks have grown their dividends roughly three times the pace of the S&P.

Kotowksi on Sept. 29 increased Oppenheimer’s 2022 earnings estimates for banks by about 1% to 2% on expectations that credit quality will surprise in the upside.

“The key thing to watch for in this and coming earnings reports will be the resumption of net interest income growth,” he said. “While it probably won’t happen in a meaningful way this quarter, it should be another stable

quarter after net interest income bottomed in 3Q20.”

This post was originally published on Market Watch