In a recent study, we used our updated National Retirement Risk Index (NRRI) to see whether households have a good sense of their own retirement preparedness — do their expectations match the reality they face? That is, do households at risk know they are at risk?

Understanding households’ self-assessed retirement preparedness is important because households that are not worried enough will not save enough and households that are too worried will unnecessarily sacrifice their preretirement standard of living.

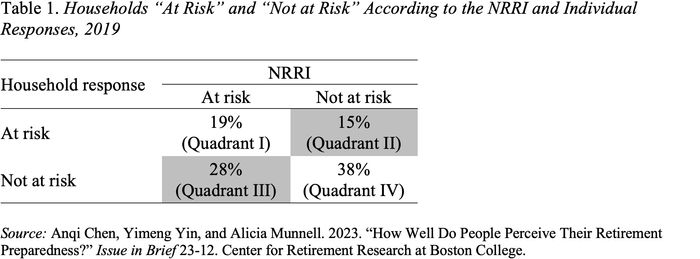

The Survey of Consumer Finances (SCF), which is used to construct the NRRI, asks each household to rate the adequacy of its anticipated retirement income. The question’s response scale is from one to five, with one being “totally inadequate,” three being “enough to maintain living standards,” and five being “very satisfactory.” Thus, any household that answers one or two considers itself to be at risk.

We compared each household’s self-assessed risk with the household’s estimated risk from the NRRI. The results show that for 57% of households their self-assessment agrees with the NRRI (Quadrants I and IV in Table 1); 43% of households get it wrong (see the shaded portions). We found 15% (Quadrant II) are “too worried” – they report being inadequately prepared but the NRRI says that they are not at risk; while 28% (Quadrant III) are “not worried enough.”

The question is why do households get it wrong? Results by income show that high-income households — perhaps overreacting to the impact of the strong economy on housing and stock prices during the 2013-2019 period — are the most likely to be “not worried enough” and low-income households are the most likely to be “too worried” (see Table 2).

The analysis used regressions for each income group to explain the relationship between various factors and the probability of households ending up being “not worried enough’ or “too worried.” Households that were overly optimistic about the economic recovery or overestimated how much income their assets could provide were more likely to be “not worried enough.” Their overconfidence may lead them to underestimate possible risks. Therefore, it is not surprising that households with higher housing debt-to-asset ratios, relatively low asset balances in 401(k)s and other defined-contribution (DC) plans, and two earners but only one saver were more likely to be “not worried enough” (see Figure 1).

Unlike overly optimistic households, those who are “too worried” are not aware of how much income they will have in retirement and perhaps have less optimism in the asset markets. Characteristics that capture these factors — such as risk aversion, married one-earner households, homeowner, and low self-assessed financial knowledge — predicted households’ likelihood of being “too worried” (see Figure 2).

The bottom line is that 47% of today’s working households are at risk: 19% know it and 28% don’t. Both groups need help.

The key message, however, is nearly three-fifths of households have a good gut sense of their financial situation and, in the aggregate, households’ self-assessments closely mirror the results produced by the NRRI. These findings suggest that inadequate retirement preparedness is indeed a widespread problem.

This post was originally published on Market Watch