Treasury yields rose Monday ahead of a Federal Reserve meeting this week that’s fully expected to see policy makers announce the tapering of monthly asset purchases amid rising investor expectations the central bank will tighten more aggressively in response to inflation pressures that have been more persistent than expected.

What are yields doing?

-

The yield on the 10-year Treasury note

TMUBMUSD10Y,

1.581%

rose to 1.579%, compared with 1.555% at 3 p.m. ET on Friday. Yields and debt prices move in opposite directions. -

The 2-year Treasury note yield

TMUBMUSD02Y,

0.513%

was at 0.509% versus 0.491% on Friday afternoon. -

The yield on the 30-year Treasury bond

TMUBMUSD30Y,

1.962%

was 1.961%, after ending Friday at 1.941%.

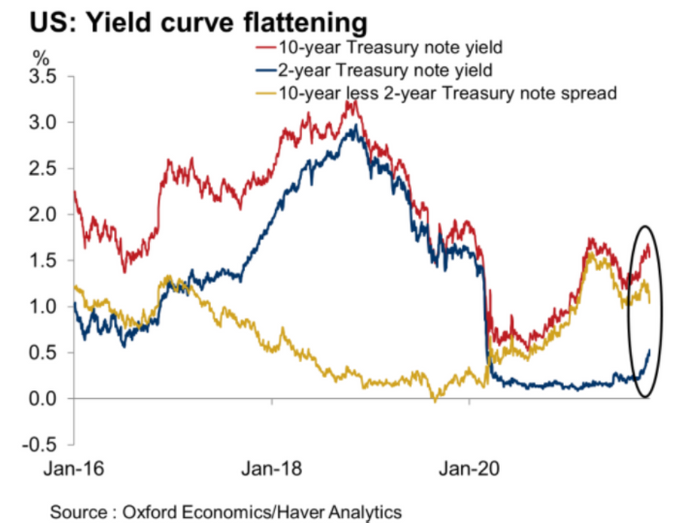

Oxford Economics

The yield curve, a line plotting yields across all maturities, flattened significantly in October (see chart above), a move that accelerated last week. Yields rose sharply at the short end of the curve, with the 2-year rate rising 20.2 basis points in October, the sharpest monthly rise since April 2018, according to Dow Jones Market Data. The 10-year yield fell 9.9 basis points last week, its largest such fall since the week ended July 2.

What’s driving the market?

The Federal Reserve will conclude a two-day policy meeting on Wednesday. Policy makers are fully expected to announce that the central bank will be scaling back its monthly asset purchases, with Fed watchers looking for a timetable that would fully wind down the buying program by June. At the same time, Fed Chairman Jerome Powell is expected to emphasize that the conclusion of the asset buying program won’t lead immediately to rate increases.

Read: Fed seen announcing start of a ‘taper’ of bond purchases this week

Nevertheless, market participants, focused on more persistent than expected inflationary pressures, have significantly moved forward expectations for rate liftoff to as early as June, helping to drive the steepening of the yield curve from the short end.

See: What Federal Reserve tapering means for markets

Investors will also be paying close attention to how the Fed, which has insisted rising price pressures would prove “transitory,” addresses the inflation backdrop, including whether or not it recasts its policy statement.

The economic calendar on Monday includes the final October reading of the Markit manufacturing purchasing managers index. The Institute for Supply Management’s closely watched manufacturing index is due at 10 a.m. Eastern. At the same time, data investors will get a look at September construction spending figures.

What are analysts saying?

“Markets are now implying a whopping three hikes in ’22, another 2+ in ’23 and maybe none in ’24,” wrote analysts at Jefferies. “It appears we went from ‘inflation is transitory’ to ‘the Fed could do something panicky’ real quick.”

“Reflecting more aggressive near-term tightening expectations, the 2-year Treasury yield has jumped 25 basis points since the end of September to 0.53%, the highest level since March 2020. The 10-year Treasury yield has held essentially steady, leading to a flattening in the 10 – 2-year Treasury yield spread to 106 basis points. This flattening reflects concern that the Fed will make a policy mistake by raising rates too quickly, slowing economic activity and that inflation will ease significantly in the 5-to-10-year range,” wrote economists Kathy Bostjancic and Gregory Daco of Oxford Economics, in a note.

This post was originally published on Market Watch