The Lloyds (LSE: LLOY) share price had been stagnant for what felt like forever. But in recent times, it seems to have kicked into gear.

The stock is up 19.5% this year. In the last 12 months, it has risen 36.9%, far outperforming the FTSE 100. That now means Lloyds has returned 7.2% over the last five years from 54.3p back then to 58.1p today.

But what could be in store for it? Right now, it seems like the Footsie stalwart can’t slow down. But is that really the case?

Broker forecasts

Well, one way to go about answering that is to look at analyst forecasts. It’s worth noting that broker forecasts must be taken with a pinch of salt. They can often be wrong. Even so, I still think they can provide a good guide.

Eighteen analysts offering a 12-month target price for Lloyds have an average price of 61.9p, which is 6.4% higher than its current price. Of those, the highest target is 74p, which is a 27.3% premium.

Room for growth?

So, analysts see Lloyds keeping up its fine form over the coming year. But what suggests that there’s still room for growth in its share price?

One factor is that the stock looks like good value for money right now, even after its recent surge. It currently trades on a price-to-earnings (P/E) ratio of 8.3. I must admit that all FTSE 100 banks seem to be trading at good value right now. Nonetheless, that’s still below the index average of 11.

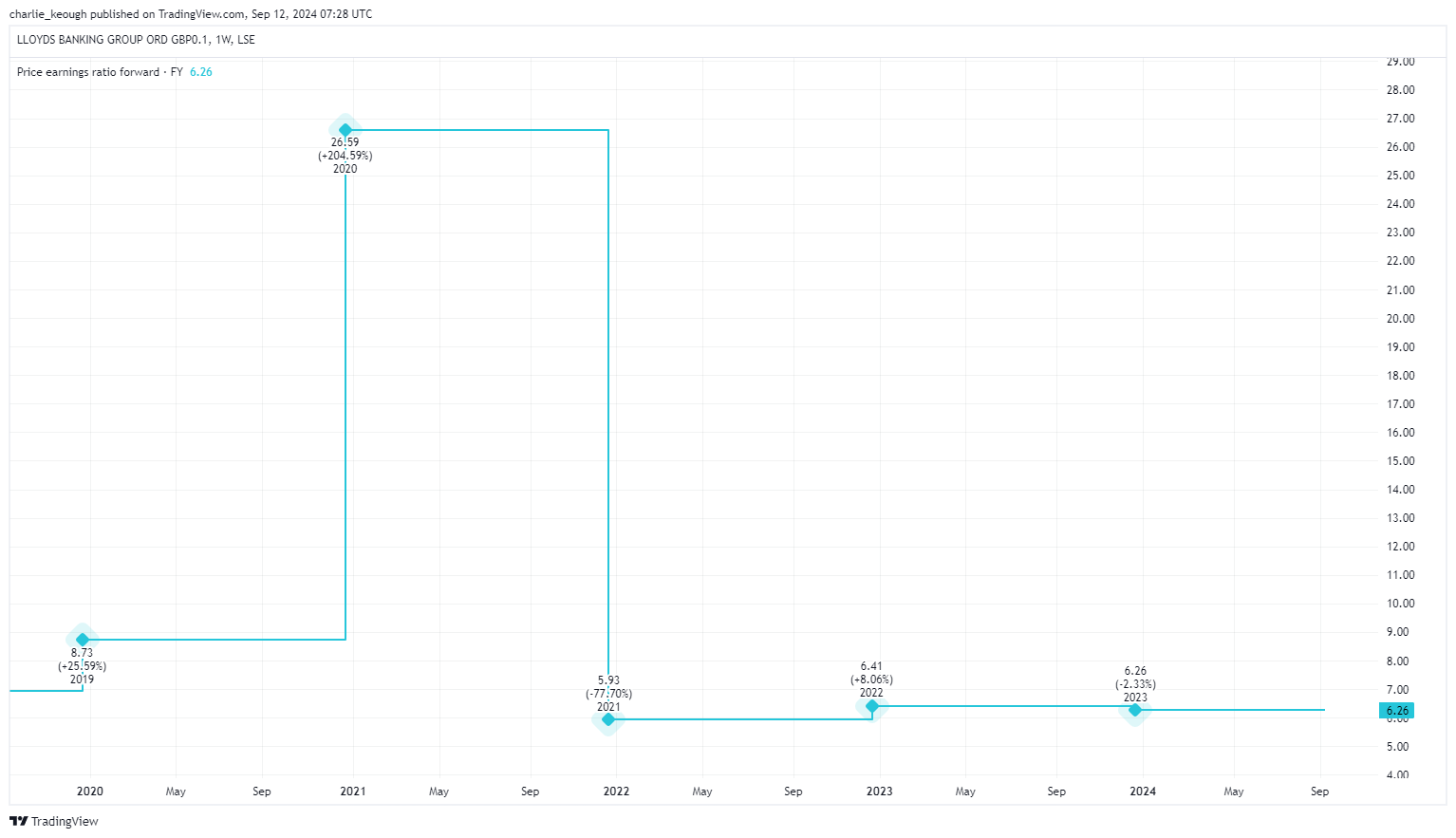

What’s more, as seen below, its forward P/E is just 6.3. Going from that, Lloyds looks like it has the potential to be cracking value at its current price.

Created with TradingView

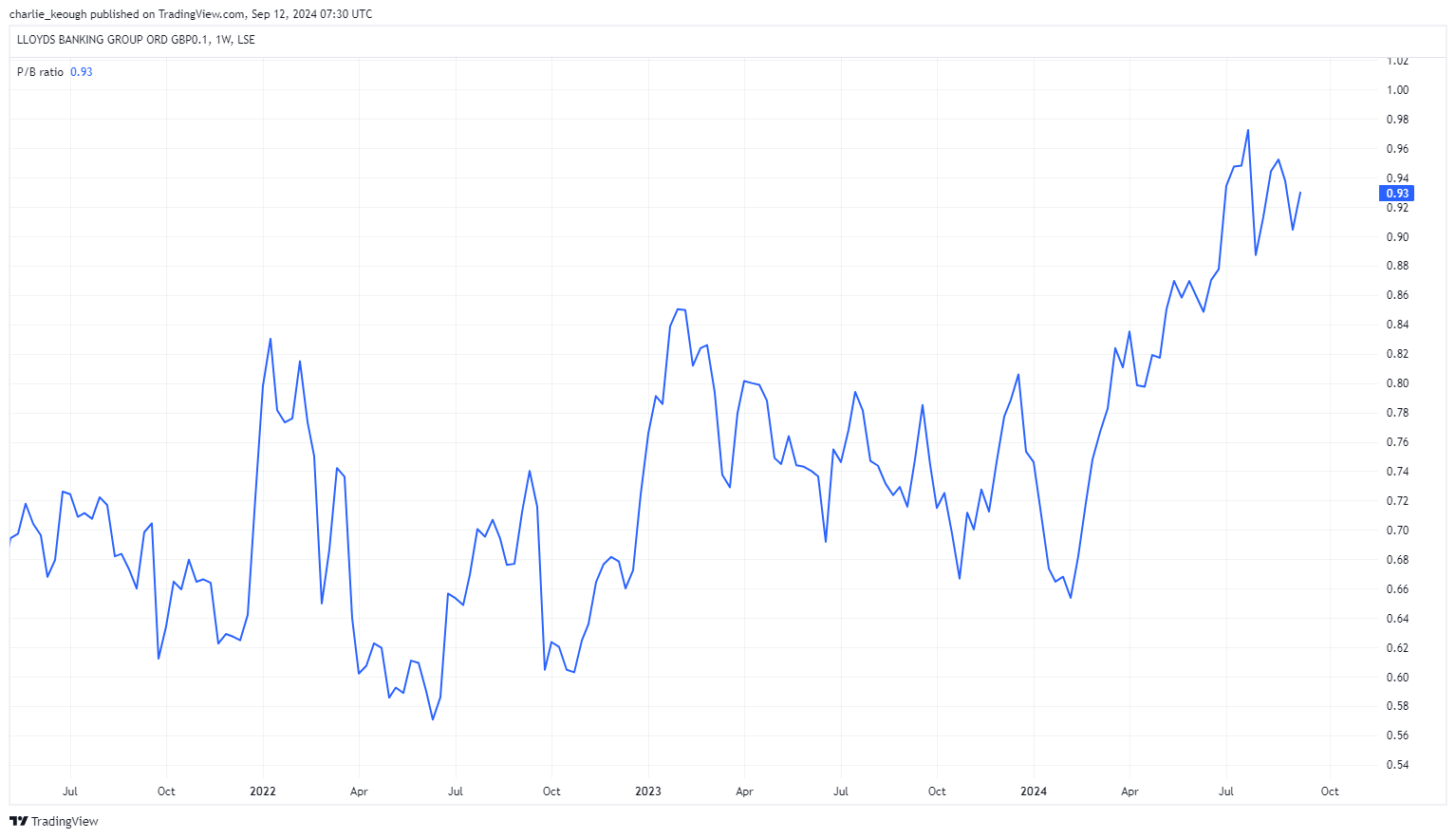

There are other valuation methods I can also use to assess Lloyds. For example, a common metric for banks is the price-to-book (P/B) ratio. As the chart highlights, the Lloyds P/B is currently just above 0.9, where 1 is considered fair value.

Created with TradingView

Based on that, I reckon we could continue to see the share price rise in the coming months.

Challenges ahead

However, volatility in the stock market is inevitable. Share prices never move up in a straight line. Therefore, I’m expecting Lloyds to face some challenges in the times ahead.

One of these will be falling interest rates. We saw the Bank of England make its first cut back in August and more are expected in the months ahead. While falling rates should more widely boost investor sentiment, it will harm Lloyds’ margins.

That’s because lower rates mean the bank can’t charge customers as much when they borrow money. We saw this in the first half of the year, when its net interest margin slipped from 3.18% to 2.94%.

On top of that, there’s the ongoing investigation by the Financial Conduct Authority surrounding a car finance scandal. Lloyds has set aside £450m to cover potential costs, but this could end up rising.

I’d buy today

But even with those risks considered, I think Lloyds could make a great long-term buy today. If I had the cash, I’d happily snap up some shares. While I’m expecting some peaks and troughs, I think its cheap valuation suggests there’s still room for future growth.

This post was originally published on Motley Fool