For years I’ve been worried about dividends from BT Group (LSE: BT.A) shares. I’ve always looked at the company’s capital expenditure (capex), and its high net debt levels, and wondered how long it could keep the cash payments going.

But then, BT keeps managing it. And even though the share price is up a bit this year, we’re still looking at a forecast dividend yield of 5.6%.

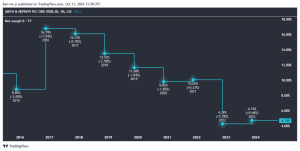

Dividend forecasts

If those dividends keep on going at their current levels, we might have a nice long-term income investment here. And if current broker forecasts are anything to go by, they look good, at least until 2027.

The figues in the table below are all based on a BT share price of 142.5p, at market close on 4 October. They show 2024’s results, with the next three years of forecasts.

| Year | Dividend | Change | Yield | EPS | Cover | P/E |

| 2024 | 8.0p | +3.9 | 5.6% | 8.6p | 1.1x | 16.6 |

| 2025 | 8.2p | +2.5% | 5.8% | 14.3p | 1.7x | 10.0 |

| 2026 | 8.3p | +1.2% | 5.8% | 15.3p | 1.8x | 9.3 |

| 2027 | 8.2p | -1.2% | 5.8% | 15.3p | 1.9x | 9.3 |

Why do I think BT dividends might be safer now? It’s partly because the company says it’s passed the point of peak capex for full-fibre broadband. And it’s partly because forecasts show strong enough earnings to provide decent dividend cover.

Rising debt

That debt hasn’t gone away though. In fact, net debt is a bit higher this year. It’s up 3.1% to £19.5bn, from £18.9bn a year previously. Anlaysts expect it to grow a bit more in the next few years too.

I think it pays to take a moment to let that sink in. BT’s net debt is about the same as its total annual revenue. And it’s 2.4 times the 2023-24 full-year EBITDA.

I’ve often thought it would be better to use surplus cash to reduce the debt rather than pay dividends. But it looks like it wouldn’t have a huge effect.

Dividend cost

In the last full year, dividends cost £759m. Debt repayments in the period came to £1.68bn, with £865m paid in interest.

So the dividend cash amounted to only 3.9% of BT’s net debt. I find that both reassuring and scary. It makes me think BT’s likely to keep paying the dividends, because they don’t actually cost that much by comparison. But it gives me a feel for just how big the debt is.

Progressive

The board said: “We reconfirm our progressive dividend policy which is to maintain or grow the dividend each year“. But it added some stuff about “taking into consideration a number of factors“.

This highlights that there’s never a guarantee when it comes to dividends. And investors have to be aware that the cash just might not turn up.

I’m still torn over whether to buy BT shares. I really do fear that the debt could come back and bite. It’s been built up by the massive cost of fibre rollout. And BT seems to be pinning its hopes on big takeup. I fear customers might be slow to switch.

But a long-term reliable yield would be really nice.

This post was originally published on Motley Fool