The IAG (LSE:IAG) share price was vastly undervalued, according to City and Wall Street analysts. When I covered the stock in early August, the airline operator was trading at a 42.8% discount to the average share price target.

So, why has the stock started moving toward its share price target? And will it go higher from here?

Let’s explore.

New catalysts

There are several reasons the IAG share price is trading higher.

First is the decision, reported on 1 August, to scrap the proposed takeover of Air Europa. This removes significant regulatory risks, particularly from the European Union’s antitrust regulators, and alleviates concerns about potential fines and operational disruptions.

A day later, IAG reported strong financial results for the first half of 2024, with revenues increasing by 8.4% year on year to €14.7bn and operating profit rising to €1.3bn.

The company, which owns brands like British Airways and Iberia, also achieved a substantial reduction in net debt, down 31% to €6.4bn, further strengthening the balance sheet.

New dividend, solid outlook

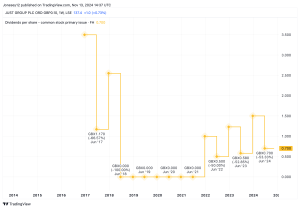

In a boost for shareholders, IAG also announced a return to dividend payments with a €0.03 interim dividend. While that’s great for investors, it also signals management’s confidence in the company’s financial health.

Looking forward, management reinforced this confident outlook with a growth strategy that includes a capacity increase of 4%-5% through 2026 and an ambitious target for operating margins of 12%-15%.

Analysts project earnings growth of 4.8% annually until 2026, supported by strong demand in core markets like North America and Latin America.

This isn’t a world-beating pace of growth, but airlines are cyclical. We’ve recently experienced two years of incredibly strong fare growth, which in the long run, is unsustainable.

And for context, Ryanair announced a 46% fall in Q1 profits in July, noting that summer fares would be materially lower.

As such, analysts’ forecasts for IAG looks pretty strong.

The bottom line on IAG

If there is a slowdown in demand for air travel, IAG may be better positioned than its low-cost peers. That’s simply because it has a more varied offering, catering to business travel and offering more seating options.

That’s something I really like about IAG.

I also like that it’s less reliant on Boeing than Ryanair and most US-listed airlines. Boeing’s quality and delivery issues have resulted in lower capacity across the industry.

So, there must be something worth worrying about? Well, debt is a concern. Net debt sits around €6.4bn, and that’s around half the market cap.

Currently, servicing that debt doesn’t appear problematic, but if we were to see some shocks — e.g., a significant jump in fuel prices — and earnings were to fall, debt would become more problematic.

Nonetheless, I’m personally still bullish on IAG. I’m expecting modest earnings growth from a company that trades at just 5.3 times forward earnings and an EV-to-EBITDA ratio of 3.2 times.

It might be a little pricier than easyJet, but it has a more varied offering, and it’s a lot cheaper than Ryanair and other US stocks.

This post was originally published on Motley Fool