The Rolls-Royce (LSE: RR) share price continued its incredible ascent in August by powering above 500p. This meant the FTSE 100 stock had surged over 600% in just 22 months!

However, after an 11% rise in August, the start of this month has brought significant turbulence. Yesterday (2 September), the share price dipped 6.5% to 464p. As I type though, it’s rebounded 3.1% to 478p.

What’s going on here?

Grounded aircraft

Yesterday’s decline followed an incident where a Cathay Pacific Airways flight from Hong Kong to Zurich experienced issues, forcing it to circle twice over the sea to dump fuel before landing safely.

The A350-1000 aircraft was powered by Rolls-Royce’s XWB-97 engines and the problem appears to be related to a fuel nozzle. In response, numerous flights have been cancelled by Hong Kong’s Cathay Pacific as fleet-wide precautionary checks and repairs are carried out.

This does highlight how problems like this can suddenly crop up and cause investors to panic. If there was a major engine architecture fault, the financial liability would likely be significant.

Indeed, Rolls took a huge hit in 2018 when it had to inspect and repair engines after discovering cracks in turbine blades.

Fortunately, this doesn’t appear to be anywhere near as serious. The airline operator says it expects the grounded planes to be out of service for just “several days“. Hence the rise in Rolls-Royce shares today.

Incredible business performance

Back in August, the firm won an order from Cathay Pacific for 60 Trent 7000 engines. It will make the airline the world’s largest operator of this engine model, which is expected to reduce emissions by 14% in combination with Airbus‘s A330-900 aircraft.

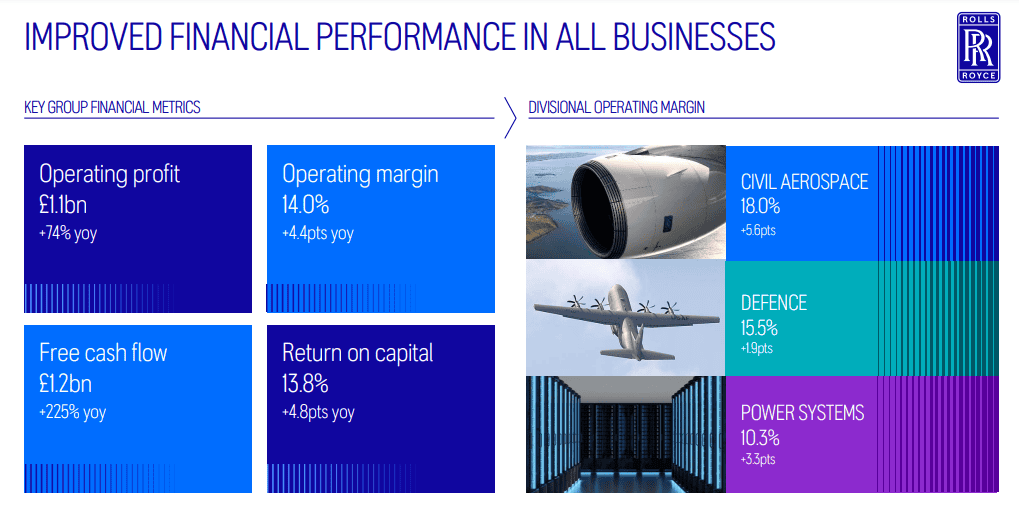

This announcement builds on incredible commercial momentum at the company. In H1, we saw financial improvement across all areas.

By the end of 2024, management expects to have cumulatively delivered more than 75% of its mid-term operating profit target (£2.5bn–£2.8bn).

Meanwhile, net debt has been reduced to its lowest position in more than five years, which has enabled the return of the dividend.

This progress is reflected in the stock’s valuation. The forward price-to-earnings ratio is around 28 (a hefty premium to the FTSE 100). So there’s still a lot of optimism baked into the share price.

The growth story still looks strong

On the engine issue, brokers don’t seem overly concerned for now. Deutsche Bank, for example, reckons the financial impact will be manageable: “While the news raises some concerns, our preliminary analysis is that the financial liability could be contained. Hence, our positive view of the equity story is unchanged.”

The bank maintained its own target price of 555p, which is 16% above the current level.

Looking ahead, I’m still bullish. The number of aircraft is expected to double over the next 20 years due to surging global travel. This growth will likely lead to a significant increase in Rolls-Royce’s engine fleet and the lucrative aftermarket services that come with it.

Last month, I bought more shares for the first time in 18 months. I’m happy to hold that position for the next few years as this long-term growth story hopefully plays out.

This post was originally published on Motley Fool