The past few years have been strong ones for the BAE Systems (LSE: BA) investment case. During that period, BAE Systems shares have risen 160%.

Last year saw record turnover, while profits reached almost £2bn. For a company with a market capitalisation of under £40bn that looks fairly impressive to me.

It also means that the shares trade on a price-to-earnings (P/E) ratio of 20. That is at the high end of the valuation range I would normally consider for a company in a mature industry, but if the business is high enough quality I would consider it.

Strong business prospects

The wind has been in the aerospace and defence contractor’s wings for the past several years. From a rebound in demand for civil aviation to surging demand for defence and warmongering equipment from a wide variety of governments worldwide, BAE and many of its peers have been in clover.

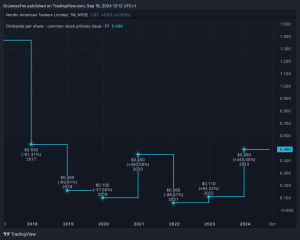

The company’s sales last year rose 9%, free cash flows surged 33%, and basic earnings per share were up a fifth. That performance meant the company felt confident to boost its dividend per share by 11%. Given the share price has risen faster than that, though, the yield is now 2.3%. That is reasonable in my view but not particularly exciting and is well below the current FTSE 100 average.

The company’s order intake last year barely grew but was still an impressive £38bn. That meant the order backlog grew £11bn to £70bn.

There is plenty for the firm’s workers to be getting on with for now. It sees strong ongoing growth prospects and grew its workforce by over 6,000 last year.

This is an industry built on proprietary technology and often complex long-term relationships, with few or no competitors for a lot of what the business does. That bodes well not only for future demand but also for ongoing profitability.

Shares look reasonably priced

What about the price outlook for BAE Systems shares?

Although the P/E ratio is not cheap, it strikes me as reasonable. Given the order book and ongoing strong customer demand, I think the company can likely grow profits over the next few years. That would mean the prospective P/E ratio is lower. If that comes to pass, I expect the shares could move up further.

But at some point, that demand may shift. As we saw during the pandemic (more obviously with Rolls-Royce, but also with BAE Systems), demand from civil aviation customers can move around significantly.

Military spending is robust for now and looks set to stay that way for the medium term, in my view. But once European armed forces rebuild their previously depleted equipment levels, demand could drop back closer to where it stood a few years ago.

The order backlog also bothers me. Yes, BAE Systems is selling its products so effectively. But a large order book brings the risk of costly delays in delivery.

Critically, I do not like the business BAE Systems is in. Each investor has their own ethical benchmark and while cigarettes pass mine, global military equipment sales do not. So, I have no plans to add BAE Systems shares to my portfolio.

This post was originally published on Motley Fool