Broker-dealer LPL Financial no longer expects the benchmark 10-year Treasury yield to climb as high as 2% by year-end.

Instead, sharp interest from foreign buying in haven U.S. government debt and economic weakness prompted by the coronavirus’ delta variant have led Lawrence Gillum, LPL’s fixed income strategist, to revise lower his firm’s expected year-end range for the benchmark to between 1.5% and 1.75%.

“Higher inflation expectations, less involvement in the bond market by the Federal Reserve (Fed), and a record amount of Treasury issuance this year were all reasons we thought interest rates could end the year between 1.75% and 2.0%,” Gillum wrote in a recent note.

The successful rollout of COVID-19 vaccines in early January were part of the reason for Gillum’s earlier 10-year yield

TMUBMUSD10Y,

forecast, fueling expectations for a reversal of pandemic lockdowns, climbing gross domestic product growth and rising long-term Treasury rates.

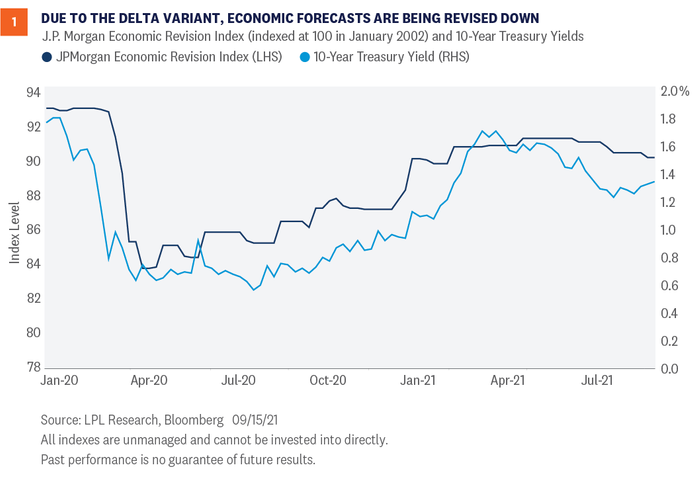

“However, due to the persistence of the delta variant, we are starting to see GDP growth forecasts revised lower. That has kept interest rates relatively anchored at current levels,” according to Gillum, who included the following chart tracking economic growth to underscore the point.

Economic forecasts revised lower on delta variant concerns.

LPL Research, Bloomberg

On Tuesday, the 10-year rate rose to 1.323%, after concerns about Chinese property giant Evergrande Group

3333,

sparked a flight to safety on Monday and the biggest one-day tumble for Treasury yields in about six weeks.

Persistently low global rates on government and corporate bonds also have attracted foreign investors looking for a bit of yield to Treasurys.

“Aging demographics and strong social-support programs have made many Japanese and European investors look outside of their home countries to help fund underfunded pension schemes,” Gillum wrote.

“Currently, there remains nearly $15 trillion in negative-yielding debt globally, which makes the 1.33% 10-year Treasury yield (as of September 16) look extremely attractive.”

This post was originally published on Market Watch