BlackRock has upped its overweight of inflation-linked bonds, a move the giant asset manager said it made in March to “quickly take advantage” of the market pricing in a lower cost of living despite persistent price pressures.

Last month bond yields dropped after the sudden failure of Silicon Valley Bank and Signature Bank, as investors bet the fallout would lead the Federal Reserve to pivot from interest rate hikes and battling inflation to rate cuts in an anticipated recession.

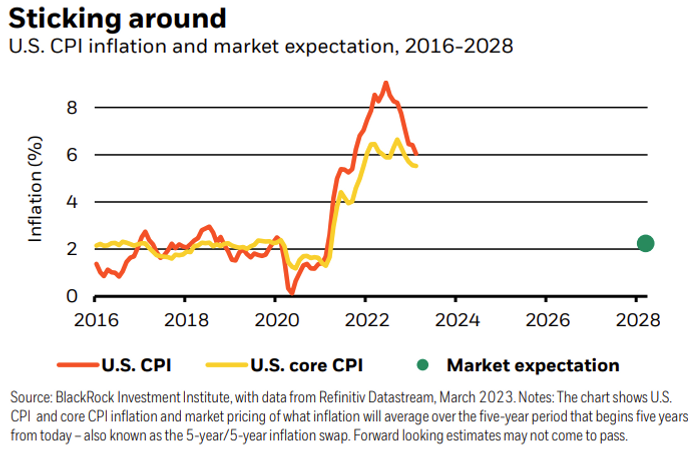

“U.S. core inflation is not on track to fall to the Fed’s 2% target, like markets expect,” BlackRock Investment Institute strategists led by Jean Boivin said in a note dated April 10. The market’s pricing of future inflation, seen in the “breakeven” rate, narrowed in March, signaling investors saw the high cost of living in the U.S. falling to 2% due to the banking-sector turmoil and a nearing recession, their note shows.

BlackRock

BLK,

which already was tactically overweight inflation-linked bonds, said it “used the repricing to go more overweight.”

The strategists expect “sticky inflation” will prevent rate cuts in 2023. A tight labor market is “boosting wage growth,” adding to price pressures, they said, while “some goods inflation is already ticking back up.” They also pointed to the rise in prices in services “making core inflation stubborn” and said potential supply shocks, “like the surprise OPEC+ oil production cut,” may trigger “brief spikes in headline inflation.”

On Wednesday, investors will get a fresh reading on inflation in March from the consumer-price index, including core data excluding energy and food prices.

As for the labor market, the U.S. economy added 236,000 jobs in March, with the unemployment rate dipping to 3.5%, according to data released April 7 by the Bureau of Labor Statistics.

“Bond yields rose after data showed a still-tight U.S. labor market,” the BlackRock strategists said. “We think that keeps inflation sticky and makes Federal Reserve rate cuts this year unlikely.”

Treasury yields have been climbing so far this week.

The yield on the 10-year Treasury note

TMUBMUSD10Y,

rose 1.9 basis points Tuesday to 3.433%, while two-year Treasury yields

TMUBMUSD02Y,

climbed 5.2 basis points to 4.056%, according to Dow Jones Market Data.

BlackRock’s head of iShares investment strategy for the Americas, Gargi Chaudhuri, told MarketWatch in an interview last week that the iShares TIPS Bond ETF

TIP,

may be a “good addition” for portfolios in terms of a “tactical” allocation on concerns elevated inflation could linger higher than the market was anticipating. The fund tracks an index of U.S. Treasury inflation-protected securities, or TIPS.

‘New playbook’

In its note, BlackRock Investment Institute tracked the consumer-price index, core CPI data and the “market pricing of what inflation will average over the five-year period that begins five years from today” — a measure known as the “5-year/5-year inflation swap.”

BLACKROCK INVESTMENT INSTITUTE NOTE DATED APRIL 10, 2023

In the past, inflation-linked government bonds “behaved more like risk assets” in economic downturns, “underperforming nominal government bonds in economic downturns,” the BlackRock strategists said.

Last month, investors seemed to be following that “old playbook” on recession and bank-stability worries, but “we think U.S. inflation will remain above the Fed’s target for some time,” they said.

While a recession would help cool inflation, BlackRock expects the Fed will stop hiking rates once economic damage becomes “clear” and before a downturn turns “severe,” according to the note. “That means it won’t have done enough to create the deep recession needed to achieve its inflation goal, so it will be living with some above-target inflation.”

A pause in Fed rate hikes won’t necessarily be immediately followed by cuts. In BlackRock’s view, investors pricing in “repeated rate cuts” may be anticipating a “rescue” by central banks while underestimating the persistence of inflation.

“We wield our new playbook and seized the opportunity to add to our existing tactical overweight to inflation-linked bonds in March – one of our highest conviction views,” the strategists said. “We think market pricing is underappreciating persistent inflation and took advantage of the dip in expected inflation in March to up our overweight.”

This post was originally published on Market Watch