It’s been an incredible year for the Rolls-Royce (LSE: RR.) share price. During the last 12 months, the stock has jumped a monumental 140.4%.

We’ve seen its fine form continue recently. In the last month, the stock has climbed 5.9%. It’s up 6.6% in the last five days alone.

But now sitting at £5.28 a share, what’s next in store for the British icon? While it may seem like Rolls stock can’t slow down, is there a threat that it has gone too far?

Before we delve into that, I want to explore what has been the catalyst behind its share price soaring in the last week or so. The reason is that Rolls was chosen by CEZ Group, the Czech state utility company, as the preferred choice for its small modular reactor (SMR) programme out of seven potential candidates.

Investors have been getting excited about Rolls’ SMR business for a while now. So, it’s no wonder its share price jumped when this deal was announced.

Valuation

But with its recent rise pushing the share price comfortably past the £5 mark, is there any room for further growth?

There are a few ways to go about answering that question. Let’s start by looking at the stock’s valuation.

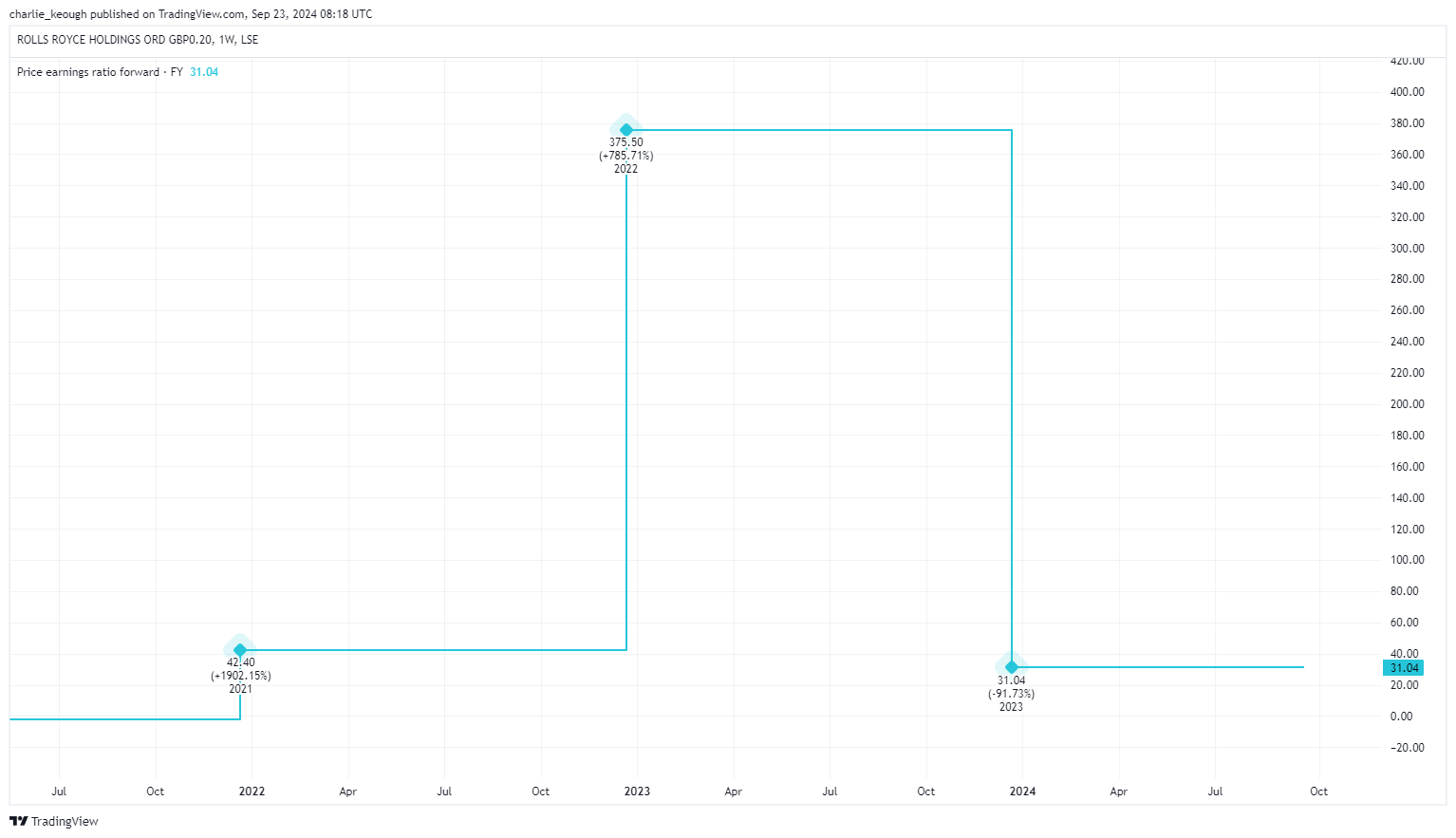

It currently trades on a price-to-earnings (P/E) ratio of 19.1. That’s above the FTSE 100 average of around 11. As seen below, when looking ahead its forward P/E rises to 31.

Created with TradingView

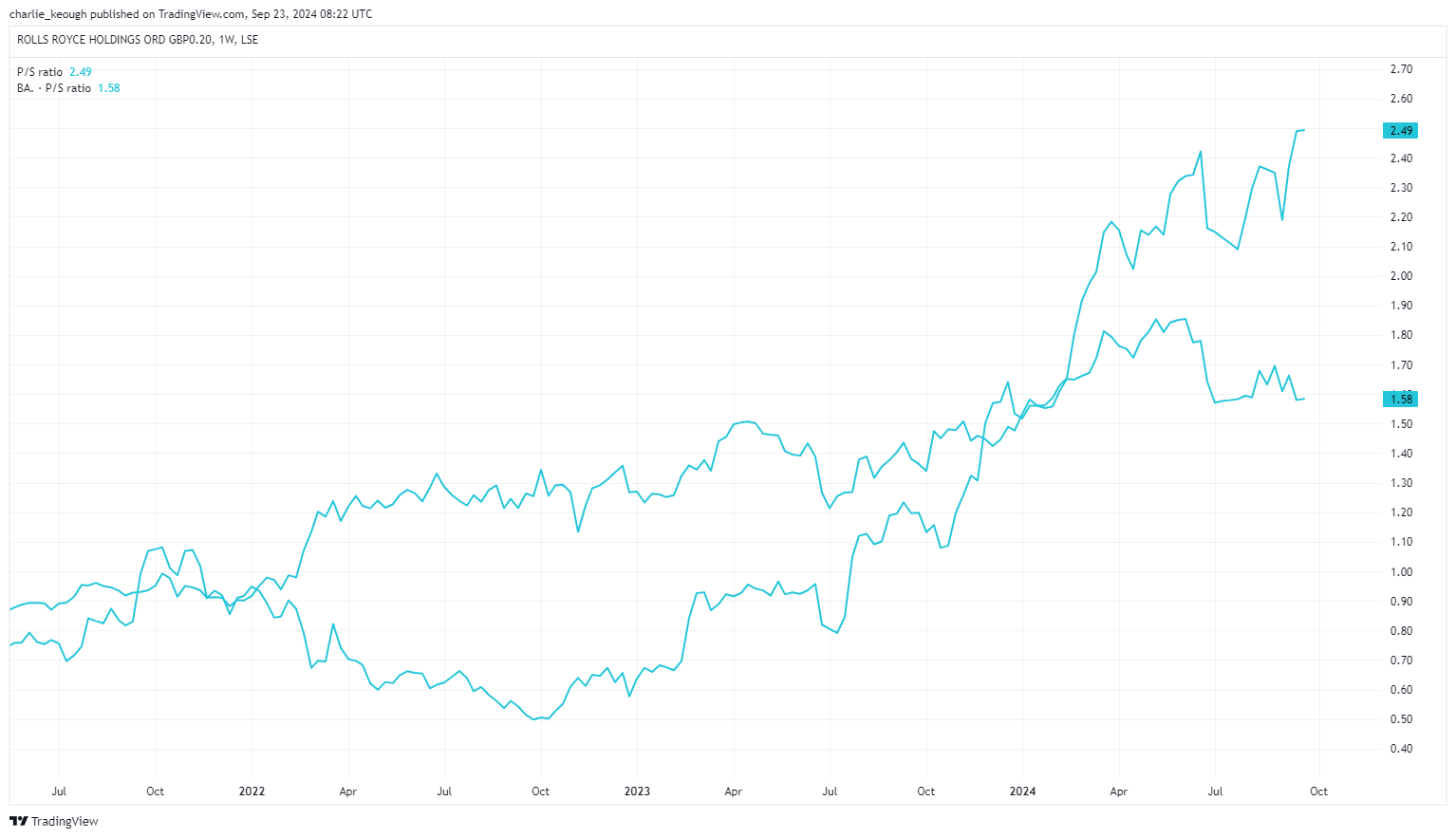

Then there’s its price-to-sales (P/S) ratio. As the chart below highlights, its current P/S is 2.5. That’s slightly above FTSE 100 competitor BAE Systems (1.6).

Created with TradingView

More to come?

Based on that, it’s possible to argue that Rolls-Royce is overvalued. But what do the experts see the stock doing in the times ahead?

Fourteen analysts offering a 12-month target price for it have an average price of £5.81, representing a 10.2% premium from where the stock sits today.

Of course, analysts’ predictions can be wrong. However, it’s clear that on the whole, they believe it can keep creeping upwards.

The bigger picture

I can see why. The business has produced a great U-turn from where it was during the pandemic. Under CEO Tufan Erginbilgic, the firm has transformed back into the powerhouse it once was.

Under his leadership, profits have soared. In its most recent half-year update, Rolls posted an operating profit of £1.1bn, up 74% from the same period last year. Looking more long term, the company is targeting £2.8bn in operating profit by 2027.

Of course, that won’t come without challenges. For example, supply chain issues could prove to be a stumbling block. In its update, it highlighted that it expects up to a £200m cash impact to these issues on its free cash flow for the year. There’s the threat that this risk will continue in the next 24 months as well.

But even despite these challenges, this is a stock I like the look of today. While its valuation may look a tad expensive, I’m happy paying for quality. And with Rolls-Royce, I think it has plenty. I’m hoping to have some cash this month so I’ll be picking up some shares.

This post was originally published on Motley Fool