Shares of Zoom Video Communications Inc. sank toward its first sub-$200 close in 18 months on Tuesday in the wake of fiscal third-quarter results, as some Wall Street analysts expressed concern over customer growth even as the videoconferencing-service company extended its streak of profit and revenue beats.

The stock

ZM,

plunged 18.0% in morning trading, putting it on track for the lowest close since May 29, 2020. It was also in danger of the suffering the biggest one-day selloff since going public in April 2019, as it was ahead of the current record 17.4% closing drop on Nov. 9, 2020.

The company reported late Monday fiscal third-quarter earnings and revenue that rose above expectations. The company has beat on both metrics every quarter since the first earnings report in June 2019.

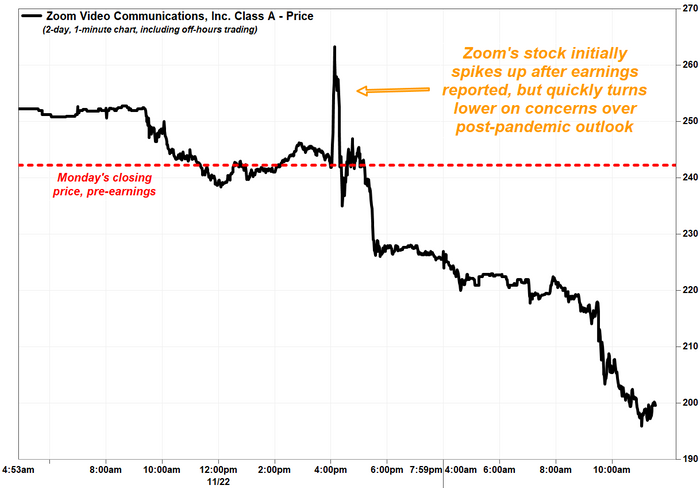

The stock had briefly spiked higher right after the results were released before reversing course.

Don’t miss: Zoom’s stock swings lower on fourth-quarter prospects after initially rising on revenue and earnings beat.

FactSet, MarketWatch

The issue for analysts and investors, however, was the customer additions, as well as uncertainty over growth expectations in a post-pandemic world.

The company reported 512,000 customers with more than 10 employees at the end of the quarter to Oct. 31, up 18% from the same period a year ago, but that growth decelerated from 36% at the end of the second quarter and from 87% at the end of the first. And customers with more than 10 employees made up 66% of total revenue, up from 64% last quarter and 63% the quarter before that.

Analyst Siti Panigrahi at Mizuho slashed his stock price target to $300 from $350, but kept the buy rating he’s had on the stock for the past 13 months as his new price target still implied more than 50% upside potential from current levels.

Panigrahi said Zoom cleared “a lowered bar” with its results, amid strong enterprise and Zoom Phone growth, and a better-than-expected online business with improved churn. Although he believes Zoom’s products will remain “integral” to hybrid work environments for the foreseeable future, “the company’s post-pandemic durable growth profile remains somewhat unclear.”

He continues to expect Zoom’s online business to decline as a percentage of total revenue given “post-pandemic normalcy” and greater enterprise penetration. However, he urged investors to “more heavily weight Zoom’s continued enterprise gains and consider Zoom’s de-risking by lower online segment expectations.”

In all, no less than 13 of the 30 analysts surveyed by FactSet who cover Zoom lowered their stock price targets after the earnings report. The average target is now $309.27, down from $350.33 at the end of October.

FactSet

J.P. Morgan’s Sterling Auty kept his rating at overweight, which he raised to overweight last month, and left his price target at $385, which implied more than 90% upside.

While growth in customers with more than 10 employees in the latest quarter disappointed — Auty was expecting 518,785 customers — and the percentage of revenue from customers with less than 10 employees continued to decline were “issues,” he said there were still plenty of positives, including growth despite the tough year-over-year comparisons and the outlook for the Zoom Phone.

“We believe this is the set up that points to bottoming in growth and re-acceleration as we head through next fiscal year that underscored our recent upgrade,” Auty wrote.

Among the non-bulls, Deutsche Bank’s Matthew Niknam reiterated his hold rating but cut his stock price target by 20% to $280, saying the company “zoomed to scale last year, but post-pandemic growth is a different story.”

He feels the next chapter in Zoom’s story yields moderating growth and profitability headwinds.

“While we’re positive on Zoom’s strategic initiatives and investments in key growth areas, we find it tougher to like a stock with more sharply decelerating growth and incremental pressure on profitability,” Niknam wrote. “We thought [fiscal third-quarter] results did little to change the narrative on either side, with bulls likely pointing to strength in enterprise and margin upside this quarter, and bears flagging negative trends in forward growth and [free cash flow].”

FactSet, MarketWatch

Analyst Matthew Harrigan at Benchmark affirmed his hold rating, and while he doesn’t have a formal price target on the stock, he lowered his “fair value” suggestion falls to $238 from $253. He said while he’s “wary” on a likely muted revenue outlook for the next fiscal year, he’s “actually are more encouraged” on the company’s long-term growth potential.

“Stock perception and upside could improve as the market gathers conviction on new elements like Zoom’s Video Engagement center,” Harrigan wrote. “The long-term Work-from-Anywhere trend appears favorably intact even as it attracts antipathy from CEOs in financial services and other sectors.”

Zoom’s stock has now shed 53.8% year to date, while the SPDR S&P Software & Services exchange-traded fund

XSW,

has rallied 24.5% and the S&P 500 index

SPX,

has climbed 24.5%.

This post was originally published on Market Watch