Shares of United Parcel Service Inc. delivered healthy gains Thursday, after Stifel Nicolaus analyst Bruce Chan said their recent selloff, despite a continued strong fundamentals and e-commerce growth, has presented investors with a “good opportunity” to buy.

The package delivery giant’s stock

UPS,

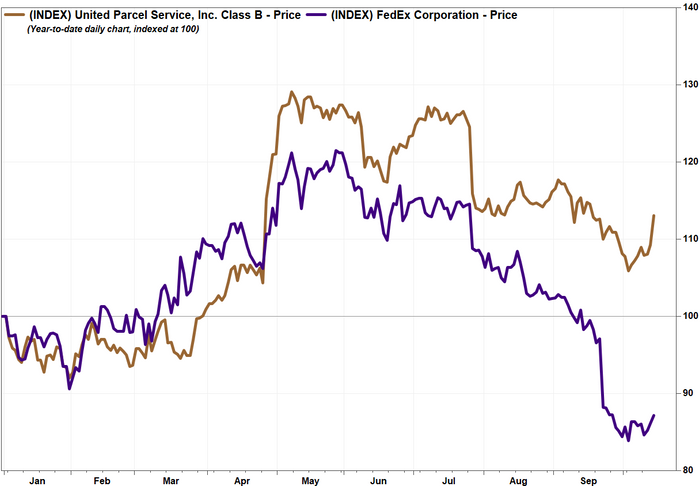

rose 3.7% in morning trading. It has now bounced 6.9% since closing at a 5 1/2-month low $178.42 on Oct. 4, but was still 12.3% below its May 7 record close of $217.50.

Stifel’s Chan raised his rating to buy, just about four months after downgrading to hold, saying “there’s a lot to like about the fundamental UPS story right now.” He boosted his stock price target to $224 from $210.

“Despite tough [year-over-year comparisons], e-commerce continues to drive secular volume growth in the company’s core small package unit, and continued yield management focus is a boon in an environment with ample near-term rate momentum, in our view,” Chan wrote in a research note to clients.

He added that a disciplined capital allocation strategy, as part of the company’s focus on being “better not bigger,” has helped set UPS to deliver in an “extremely tight” operating environment, while rival FedEx Corp.

FDX,

is likely to struggle for at least a quarter or two.

“Management picked a heck of a backdrop to refocus on yield…with significant capacity tightness bolstering rates and surcharges, and demand and network disruption driving shipper capitulation to said increases, in our view,” Chan wrote.

UPS’s stock was up 29.2% on the year at the time of its record close in May. Now, they up 12.8% this year, while rival FedEx’s stock has dropped 12.9%. In comparison, the Dow Jones Transportation Average

DJT,

has gained 18.7% and the Dow Jones Industrial Average

DJIA,

has advanced 13.9% year to date.

“With strong free cash flow and a healthy dividend yield, valuation has been our only hangup,” Chan wrote.

UPS’s implied dividend yield is 2.14%, well above the implied yields for FedEx of 1.33% and the S&P 500 index

SPX,

of 1.37%.

FactSet, MarketWatch

UPS is scheduled to report third-quarter results on Oct. 26, before the opening bell. The FactSet consensus for earnings per share is for a rise to $2.55 from $2.28 a year ago, while revenue is projected to rise 6.5% to $22.58 billion.

The company has beat EPS expectations for the past five quarters, while FedEx missed the past two quarters.

This post was originally published on Market Watch