It’s almost unheard of for the U.S. Senate to pass anything these days, much less to do so unanimously.

But earlier this month they unanimously passed a resolution honoring National Retirement Security Week, which is the third week of every October. This week, in other words. (Actually, they honored National Retirement Security Month, which is what the third week of October has metamorphosed into.)

By passing the resolution, the Senate called “on States, localities, schools, universities, nonprofit organizations, businesses, other entities, and the people of the United States to observe National Retirement Security Month with appropriate programs and activities.”

Though the resolution was short on details, the Senate’s resolution did specify that one of its main goals was “increasing the… personal financial literacy of all people in the United States.”

There can be little doubt that much work needs to be done in this regard. Consider a report released a couple of weeks ago by the TIAA Institute and the Global Financial Literacy Excellence Center (GFLEC) at the George Washington University (GW) School of Business. U.S. adults on average were able to answer only about half of 28 basic personal finance questions.

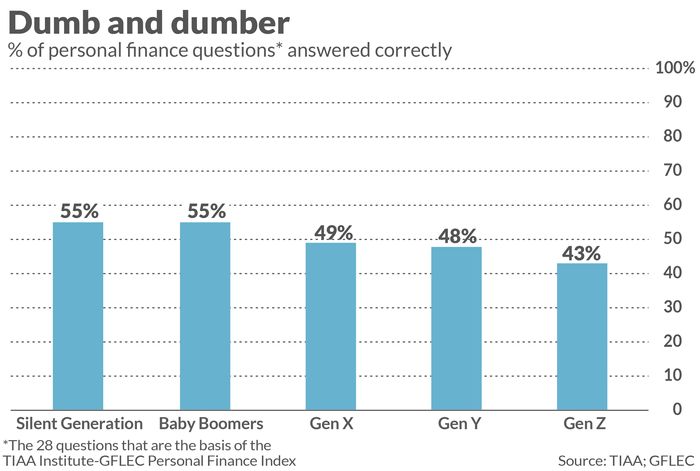

The breakdowns by generation are displayed in the accompanying chart. Members of the Silent Generation (75 and older) and baby boomers (ages 56 to 74) came out on top, but only barely. They on average got 55% of their answers correct, compared to averages below 50% for the other three generations.

But there is no reason for these graybeards to be smug. Though the usual pattern is for us to become more financially literate as we grow older, there is only a 12-percentage-point spread between the most and least financially literate generations. So one could just as easily criticize those older generations for not acquiring even greater financial literacy as they aged.

How to become more financially literate

The TIAA/GFLEC report also provides insight into what increases financial literacy. And what they found is hardly a surprise: Education. On average across all five generations, those who had received any financial education correctly answered 60% of the personal finance questions. That compares to 46% among those who had received no such education.

This financial education that so improved financial literacy is not necessarily something that gets taught in college. Those who attended college correctly answered 45% of the TIAA /GFLEC questions, on average, versus 39% among those who had not attended college—an improvement in financial literacy of just 6 percentage points. That’s significantly less than the 14 percentage improvement in financial literacy for having received any financial education.

So there’s hope even if you never went to college or got your diploma. But you definitely should take a personal finance class if you’ve never done so before—or seek out the advice of someone who has.

Overconfidence and illiteracy—a toxic mix

There’s another way to become more financially literate, or at least ameliorate the negative effects of being illiterate. And that’s to become more humble about what you know—or think you know.

That might seem counterintuitive. But researchers have found that there’s an inverse correlation between illiteracy and overconfidence, which means that those who know the least about finance tend to be surer of themselves than those who know the most. I devoted a Retirement Weekly column in June to research that documented this inverse correlation.

As Socrates reportedly said, “I am the wisest man alive, for I know one thing, and that is that I know nothing.”

The bottom line? The optimal combination of financial characteristics that we should cultivate is having a high degree of both financial sophistication and humility. That’s unfortunately all too rare, and represents a suitable goal for National Retirement Security Week.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

This post was originally published on Market Watch