BERKELEY, Calif. (Project Syndicate)—The Congress has just taken an important step toward implementing President Joe Biden’s fiscal plans, by passing a signature $1 trillion infrastructure bill. Now we will see whether the Congressional Budget Office (CBO), in its nonpartisan wisdom, agrees that the companion plan for $1.75 trillion in social and climate-related spending is fully financed by additional taxes and other “pay fors,” as moderate Democrats evidently require.

At one level, this is precisely the debate the country needs. It is a debate, fundamentally, about what kind of society the United States should be and about the appropriate role of government. Should government, to address inequality, provide more support for child care because it enables women to enter the labor force and fosters healthy childhood development, especially among disadvantaged youth? Or should it avoid doing so, as some argue, because taking child care out of the household weakens families?

Similarly, should the federal government, to combat climate change, invest in a network of charging stations for electric vehicles, just as it invested in the interstate highway system? Or is this a problem that can be left to the market, notwithstanding the existence of network effects?

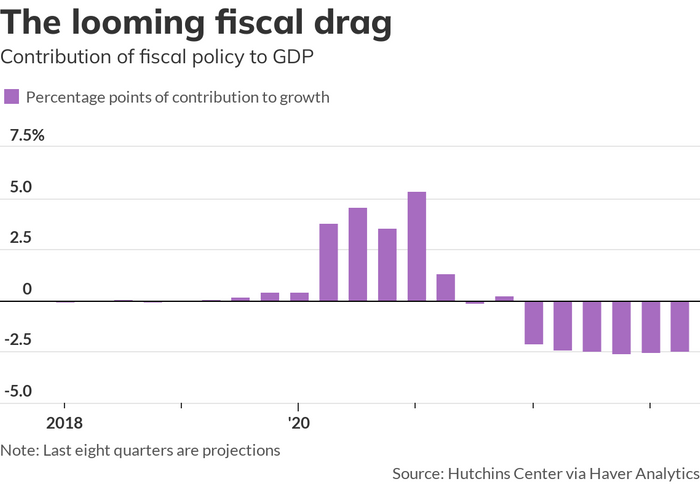

“This is an alarming amount of “fiscal drag.” Everyone is fixated on inflation and the Federal Reserve, but maybe they should be asking how, with the government vaporizing 9% of GDP, this lost spending will be made up.”

Warrantless fears

Recent debates remind us that there is less than full agreement on the desirability of such programs. But where there should be agreement is on how best to finance them. And here the debate has been derailed by warrantless fears of fiscal disaster.

Republicans and so-called moderate Democrats insist that neither physical nor social infrastructure should be deficit-financed. Having doled out trillions of dollars in pandemic relief, the U.S. already has yawning deficits and crushing debts. In the view of opponents, it cannot afford more.

What this argument misses is that here the debate is about public investment, not only transfer payments and public consumption. Productive public investments pay for themselves if they grow the denominator of the debt/GDP ratio. This is most obviously the case of physical infrastructure that makes it easier to offload containers, truck them to warehouses, and distribute their contents, enabling producers to realize the efficiencies of global supply chains. Better infrastructure boosts gross domestic product, which means more tax revenues for servicing and retiring debt.

More productive workforce

But the point applies equally to investment in social infrastructure: Pre-K and lifelong learning yield a more productive workforce. It also applies to investments in climate-change abatement and adaptation insofar as these expenditures prevent destructive climate events that cause GDP to fall.

The debate about these programs tends to be framed in terms of values. But it should also be a debate over rates of return and about which investments pay for themselves. European countries, including Germany, are having this discussion. Why the U.S. is not having it is something of a mystery. Or maybe it’s less a mystery than yet another indication of the difficulty of having any rational, informed congressional debate, whatever the issue.

But wouldn’t more deficit spending create excess demand, aggravating an already worrisome inflation problem? In fact, many earlier programs fueling the deficit are set to expire at the end of the year. CBO calculations project that the deficit as a share of GDP will fall from 13.4% this year to 4.7% in 2022.

This is an alarming amount of “fiscal drag.” Everyone is fixated on inflation and the Federal Reserve, but maybe they should be asking how, with the government vaporizing 9% of GDP, this lost spending will be made up.

But isn’t debt spiraling out of control? Having rocketed past 100% of GDP, public debt in the hands of the public is at unprecedented levels. Yet debt service as a share of GDP has barely budged since the turn of the century, because interest rates today are just a third as high. On current law, the CBO sees publicly held debt as a share of GDP falling between 2022 and 2024, as the economy expands and interest rates trend up only modestly.

In fact, between now and the end of the decade, the CBO’s projections show debt in the hands of the public as a share of GDP—wait for it—falling from 102.7% this year to 102.6%. In other words, there is no immediate crisis of debt sustainability.

Budget for surprises

Prudent governments budget for surprises. An energy shock or geopolitical event could precipitate a recession. There could be another novel coronavirus. Interest rates could rise faster than expected. It has happened before. It is entirely appropriate for governments to borrow to finance essential spending during an emergency. And once the emergency has passed, it is equally essential for governments to restore and enhance their ability to borrow so that they can deploy the same fiscal resources when the next crisis hits.

The challenge for the U.S. is to do so gradually, so that consolidation of public finances does not aggravate an already existing problem of fiscal drag. And that means not sacrificing productive public investments that more than pay for themselves.

Barry Eichengreen is professor of economics at the University of California, Berkeley, and a former senior policy adviser at the International Monetary Fund. He is the author of many books, including In Defense of Public Debt.

This commentary was published with permission of Project Syndicate—Where America’s Fiscal Debate Goes Off the Rails.

Get more from MarketWatch

House rule vote sets stage for action on ‘Build Back Better’ bill by midmonth

Opinion: The policy pendulum has swung wildly from austerity to euphoria and back to austerity again

Opinion: Broken supply chains are a market failure. What’s the right way to restore resilience?

This post was originally published on Market Watch