This article is reprinted by permission from NextAvenue.org.

Some people think high health care costs aren’t a problem for Americans 65 and older because Medicare pays all their medical expenses. But a new eye-opening report from the Commonwealth Fund, a nonprofit health care think tank, shows just how wrong that presumption is.

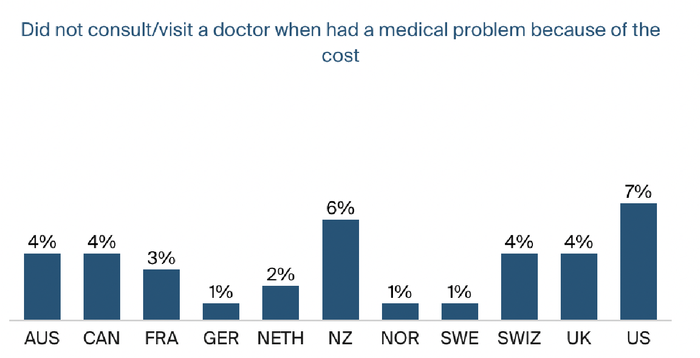

In reality, Americans 65 and older were more likely to postpone or forgo health care in the past year because of cost than people their age in 10 other high-income countries, according to the Commonwealth Fund’s survey.

What’s more, the survey of 18,477 adults found, 20% of Americans 65+ had out-of-pocket health costs exceeding $2,000 last year. That’s higher than in nine of the 10 countries (the outlier: Switzerland, at 34%). In France, Germany, the Netherlands, Norway, Sweden and the United Kingdom, just 4% to 5% did.

Unaffordable health care for people 65+

“Americans 65 and older often simply can’t afford the care and they don’t get the care that they can’t afford,” Gretchen Jacobson, the Commonwealth Fund’s vice president, Medicare, told me.

Jacobson noted that the average Medicare recipient makes about $30,000 a year. “So, when you talk about $2,000 or more out of pocket, that’s a significant amount of money,” she said. That $2,000 tab works out to about 7% of their income.

And these steep out-of-pocket health expenses can also harm Americans’ retirement security. According to the financial services firm Fidelity, the average 65-year-old couple may need about $300,000 saved for health care costs in retirement.

The Commonwealth Fund’s report comes on the heels of another one it published that I recently wrote about in “Older Americans Are Getting Slammed Financially During COVID-19 Times.” That one also found that Americans 65+ were faring worse than others their age in 10 wealthy nations.

So, what’s causing the financial stress for Medicare beneficiaries?

It’s a combination of three things, mostly: the types of care Medicare doesn’t cover; the 20% of bills beneficiaries must pay (known euphemistically as cost-sharing) for Medicare Part B expenses like doctor’s visits, mental health and preventive care and the cost of Medicare’s annual deductibles (what beneficiaries pay out-of-pocket before coverage kicks in) and premiums.

See: The twists, turns and myths of applying for Medicare: How we navigated the enrollment road

Unlike in many other countries the Commonwealth Fund studied, America’s Medicare system generally doesn’t pay for long-term care. Nor does it usually cover dental, vision or hearing costs which, a recent Kaiser Family Foundation report said, “can run into the hundreds and even thousands of dollars for expensive dental treatment, hearing aids, or corrective eyewear.” (Private insurers’ Medicare Advantage plans, the alternative to Original Medicare, often do cover dental, vision and hearing expenses, though you usually must see health care providers in their networks.)

“It seems that other countries are providing more comprehensive care for seniors in their health care,” Jacobson said.

The Commonwealth Fund

What Medicare doesn’t cover

Only about a quarter of retirees can cover severe long-term care needs for at least five years and roughly another quarter can’t afford even minimal long-term care needs, a recent report from the Center for Retirement Research at Boston College said. Just 5% of Black and Hispanic retirees have the ability to cover severe long-term care costs, this study also noted.

The Medicare coverage gaps are meaningful: 44% of Medicare beneficiaries have difficulty hearing and 35% have difficulty seeing, according to the Kaiser Family Foundation.

The Commonwealth Fund

Just 53% of Americans aged 65 to 80 have dental coverage (often through employers, spouses’ employers or Medicare Advantage plans), according to the University of Michigan’s Institute for Healthcare Policy & Innovation.

And more than one of six older Americans skipped a dental visit last year because of cost, the Commonwealth Fund found. By contrast, just 1% to 2% of older adults in Germany and the Netherlands did.

“In the countries that provide more generous dental care, not too surprisingly, only a small percentage of people skip needed dental care,” Jacobson said.

Dr. Domenica Sweier, a University of Michigan School of Dentistry professor who helped develop the National Poll on Health Aging’s dental care study, has said: “Health care providers and policy makers should seek solutions to better identify and address how cost and other factors act as barriers to dental care among older adults.”

Also see: How climate change could impact your retirement plans

President Joe Biden’s Build Back Better plan, currently being debated in Congress, would add dental, vision and hearing coverage to Medicare. That would be the largest expansion of Medicare benefits in 15 years and cost somewhere around $358 billion over 10 years.

But some legislators and analysts think this expense would be too high for the federal government, especially since the Medicare Hospital Insurance Trust Fund is estimated to become insolvent in 2026, according to its trustees.

“It’s a constant balance, I think, between beneficiaries’ affordability and affordability for the federal government,” said Jacobson. “This is a struggle that has been longstanding, since the inception of Medicare [in 1965].”

The high costs of delaying health care

But, she adds, “it comes down to what are the repercussions down the road of delayed care, delayed diagnoses and worse health outcomes.”

Studies have repeatedly determined that putting off or forgoing medical and dental care can lead to worsening physical health problems and to mental health problems. Washington Post opinion columnist Helaine Olen recently noted that people with gum disease, for example, are at higher risk for heart attacks and strokes than others.

“We know that delayed care can lead to delayed diagnoses, so that can result in poor health outcomes and also higher health care spending down the road,” said Jacobson. “So, what’s delayed today can really have important implications in the future.”

Then there are the rising costs of Medicare premiums and deductibles that eat into the wallets of beneficiaries.

The 2022 annual premium for Medicare Part B is expected to be about $1,900, which would be up nearly 7% from 2021. For Medicare Part D (prescription drugs), it’s likely to be nearly $400, an increase of about 5%.

Read next: I never expected to retire to Panama — but we are living ‘very comfortably’ on $1,200 a month

The 2022 annual deductible for Medicare Part A (hospitalization) will be roughly $1,400, the Part D deductible is expected to run about $485 and the Part B deductible will be around $217. Medicare beneficiaries will also probably need to pay $7,050 in prescription drug expenses in 2022 before the program’s catastrophic drug coverage kicks in.

Medicare is clearly a huge help for many Americans 65 and older. Even so, Jacobson said about Medicare beneficiaries: “It’s stunning how many people end up skipping needed health care because they can’t afford it.”

Richard Eisenberg is the Senior Web Editor of the Money & Security and Work & Purpose channels of Next Avenue and Managing Editor for the site. He is the author of “How to Avoid a Mid-Life Financial Crisis” and has been a personal finance editor at Money, Yahoo, Good Housekeeping, and CBS Moneywatch.

This article is reprinted by permission from NextAvenue.org, © 2021 Twin Cities Public Television, Inc. All rights reserved.

More from Next Avenue:

This post was originally published on Market Watch