There are a number of FTSE 250 shares I like very much. While it’s certainly a close call, I’d say my favourite (from an investment perspective) is Greggs (LSE:GRG).

The business has a simple, powerful model that has caused the share price to rise 58% over the last five years. And I think there could well be more to come.

Business model

Greggs has a proposition to customers that has stood the test of time. It makes popular products that consumers enjoy and it sells them at lower prices than its competitors.

The company’s low prices are important in a couple of ways. First, it means demand holds up relatively well in an economic downturn. This is especially true in the food industry. While consumers can pull back on their discretionary spending in a recession, everyone still has to eat.

It also means the increases needed to offset inflation are relatively small. Raising the price of sausage rolls from £1.20 to £1.25 probably doesn’t put too many people off.

Growth investing

Shares go up for one of two main reasons. Either the company grows its earnings per share income, or investors decide they’re willing to pay a higher multiple for the same profits.

When a rising share prices is just the result of multiple expansion, that can be a risk for investors. But with Greggs, the underlying business has been doing well.

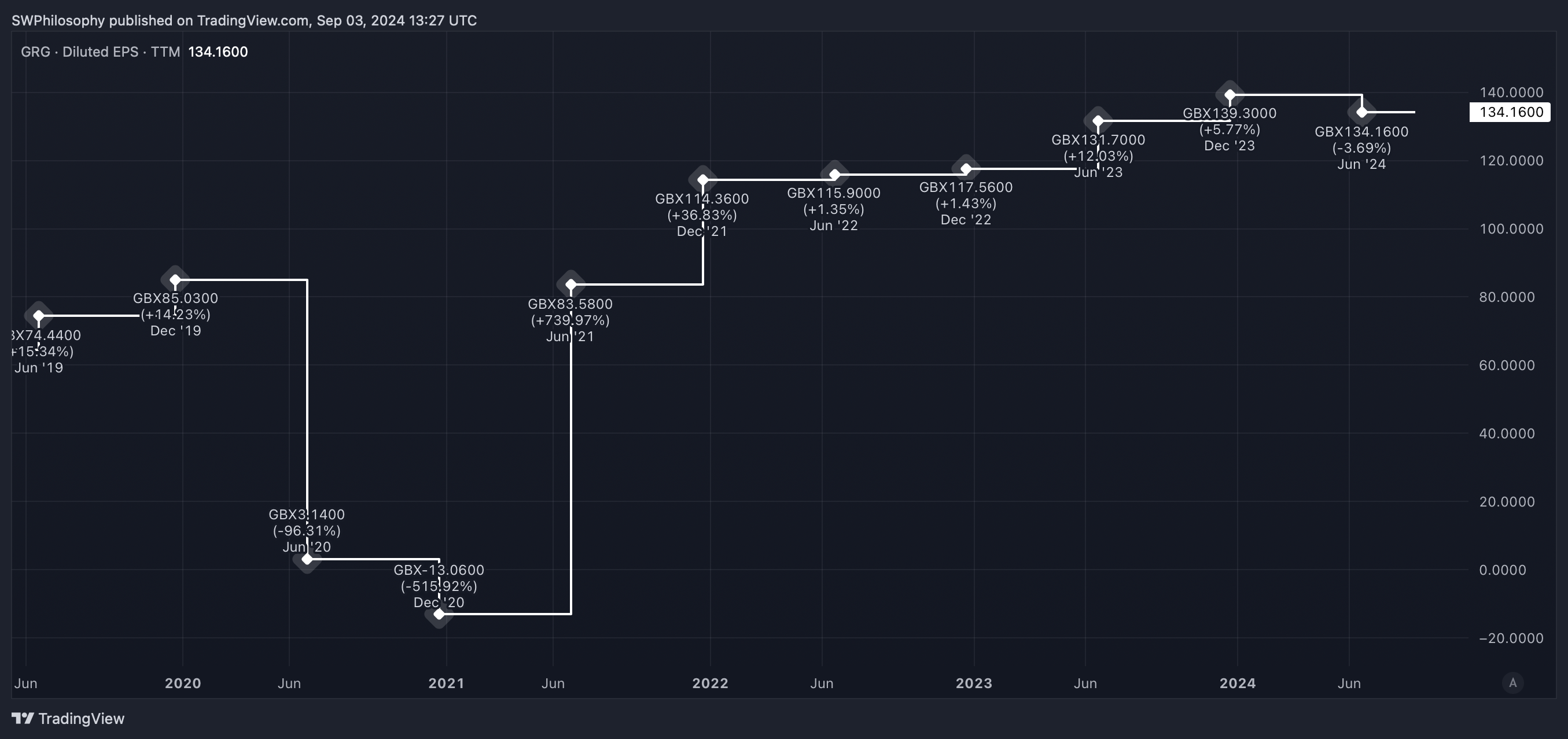

Greggs earnings per share 2019-24

Created at TradingView

Despite a downturn during the Covid-19 pandemic, the company’s increased its earnings from 85p to £1.34. By contrast, the price-to-earnings (P/E) ratio’s virtually the same.

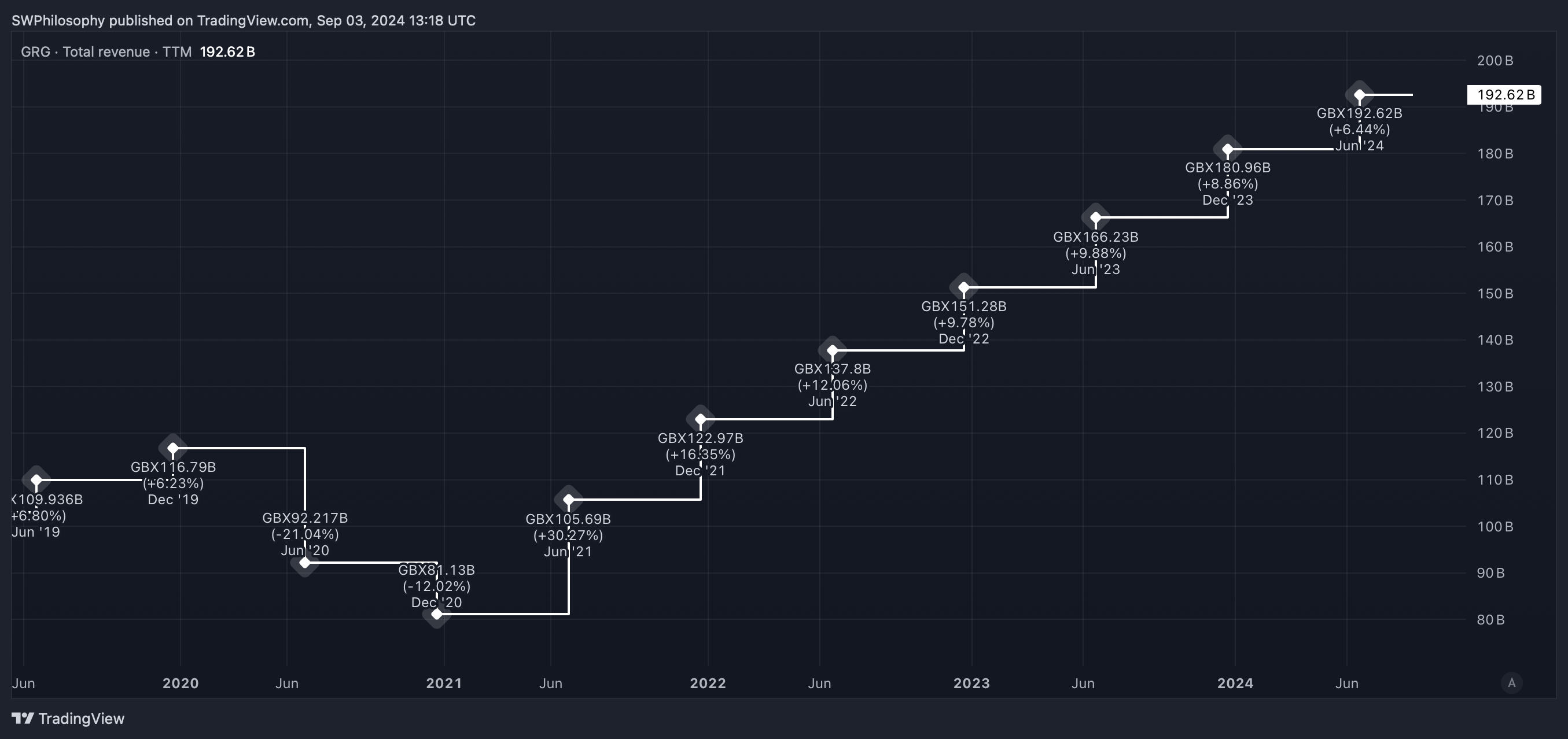

This has been driven by higher revenues as the company increases its store count from 2,050 to 2,450. And this expansion’s been executed in a highly profitable way.

Greggs revenues 2019-24

Created at TradingView

Returns

Over the last five years, Greggs has distributed around a third of its net income to investors. The rest has been reinvested to fund growth.

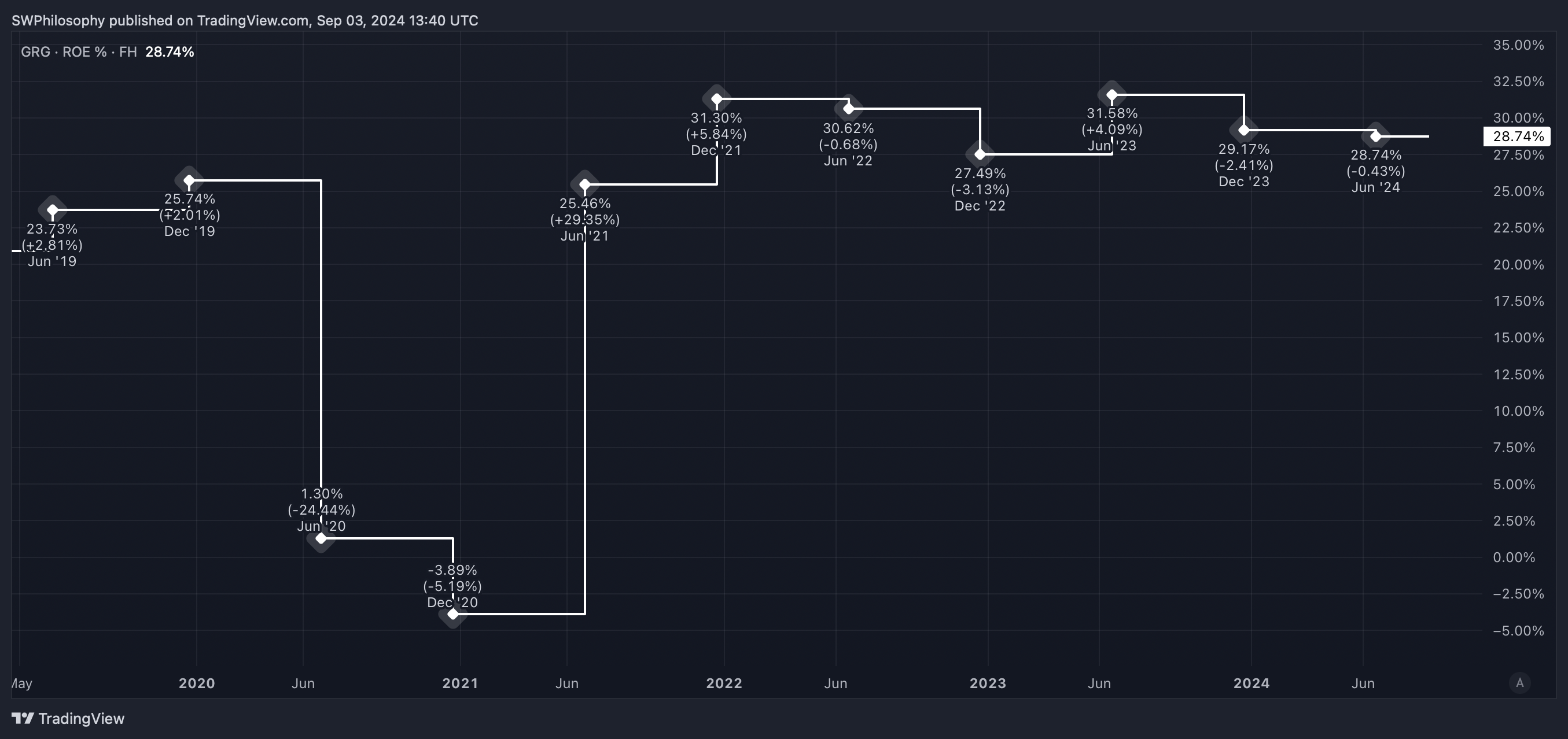

Importantly, the company’s maintained a strong return on equity during this period. That means the stores it’s been building are generating decent returns.

Greggs Return on Equity 2019-24

Created at TradingView

The firm’s success in the past is no guarantee it will be able to achieve something similar in future. Greggs is close to the limits of its manufacturing capacity at the moment.

That means the business needs to increase its production to supply new stores, which will be an additional expense. So it’s not as though the stock’s without risk.

More to come?

Greggs has built its success on implementing its product offering across new locations. And it’s ultimately targeting 3,500 stores across the UK.

Supplying that many locations may well need further investment in manufacturing facilities. But I’m expecting plenty more growth to come.

If that happens, I think the stock could go a lot higher than its current level. That’s why it’s firmly on the list of stocks I’m considering buying for the long term.

This post was originally published on Motley Fool