Friday was a bad day for the FTSE 100, which fell 1.31% as investors fretted over a potential US meltdown. Some London-listed blue-chips felt a lot faster than that, including two that have been at the top of my ‘buy’ list for months.

I’ve resisted buying them so far because I decided I was coming too late to the share price party. Have I been given a second chance?

Equipment rental specialist Ashtead Group (LSE: AHT) has had a brilliant millennium. In the 20 years to June 2023, it delivered a total return of 45,532%, with dividends reinvested, according to AJ Bell. That would have turned £10k into a staggering £4.5m.

Ashtead Group

The main driver was its US-based subsidiary Sunbelt Rentals, which now supplies 90% of Ashtead’s total group revenues.

Given today’s market cap of £22.52bn, Ashtead is unlikely to repeat its glory growth days. But I’d still like to own it as a long-term buy-and-hold.

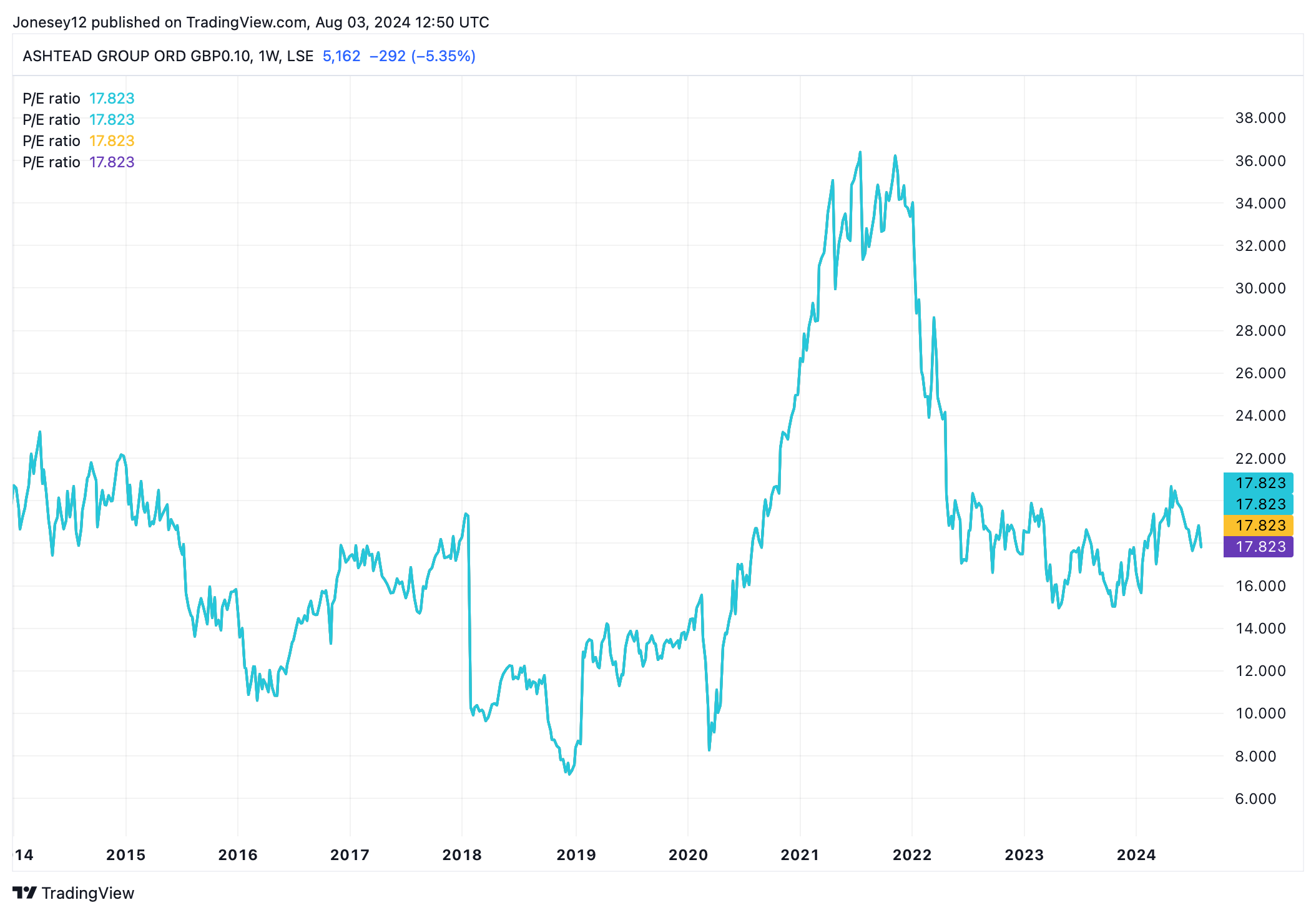

The Ashtead share price fell 5.42% on Friday. Over 12 months, it’s down 9.52% as the US economy finally stutters.

Ashtead’s sales got a kick from Joe Biden’s Inflation Reduction Act, which helped push full-year 2023 revenues to a record $10.86bn, up 12%. Growth is likely to slow this year as higher interest rates finally take their toll on the US economy.

Ashtead’s shares are now a lot ‘cheaper’ than they were in 2021 and 2022, based on its price-to-earnings ratio. Let’s see what the chart says.

Chart by TradingView

I think recent stock market volatility is a brilliant opportunity to get a stake in this top company at a reduced price, and I’ll buy it when I have cash to spare.

I’ve also been keeping tabs on another stellar performer, private equity specialist Intermediate Capital Group (LSE: IG).

On 13 June, I pointed out that it had delivered a staggering total return of 915.1% over the last decade, the highest on the FTSE 100. Over the last year, its shares are up 50.06% ,but they dropped 7.13% on Friday. It was the biggest faller on the index.

Like Ashtead, I was wary of buying on the back of a strong share price run. Today offers a more attractive entry point.

An opportunity?

ICG is a global alternative asset manager supplying capital to growing businesses. It’s a sector that tends to do well when confidence is high, but struggles when investors grow nervous. The new Labour government is looking to tighten tax rules on private equity, which won’t help sentiment.

In June, I concluded it was a frothy time to buy the stock, which had just posted a 132% jump in full-year profits to £258.1m. Some of that froth has gone now.

It’s still growing nicely, with Q1 assets under management up 23.7% to $101bn, even if only $70bn of that sum is fee earning.

Intermediate Capital Group still looks good value trading at a modest 13.05 times earnings while yielding 3.99%. I think it’s even better value than Ashtead. I’m crossing my fingers and hoping it will fall further before I find the cash to buy it.

This post was originally published on Motley Fool