Investors continue piling into money market-mutual funds, causing assets to swell to more than $5.6 trillion as of Tuesday, a record level, according to data provided by Crane Data, a longtime chronicler of the money-market fund space.

While the pace of inflows slowed during the second half of March, investors added an additional $242 billion to money-market funds since March 15. These funds typically see outflows in the weeks leading up to tax day, according to Peter Crane, founder of Crane Data, who has been tracking the sector for about 25 years.

Much of this is being parked at the Federal Reserve via its overnight reverse repo facility, or “RRP,” where funds can reap returns as high as 4.8% on an annualized basis, according to data from the New York Fed.

The concern is that if investors and savers can nab such attractive yields in money-market funds, they might continue to migrate away from the banking system into a venue where it can’t be recirculated into the economy in the form of loans.

See: Why bank savings deposit rates aren’t keeping up with the Fed’s rate hikes

U.S. money-market funds have roughly 40% of their holdings parked in the RRP, Crane said. These funds make up almost all of the $2.2 trillion in the RRP as of Wednesday, per the Fed’s data.

As a result, their weighted average maturity, or “WAM,” the shorthand used by money-market pros, has declined to just 15 days for the 100 largest money-market mutual funds tracked by Crane, down from 35 days on average in the past decade.

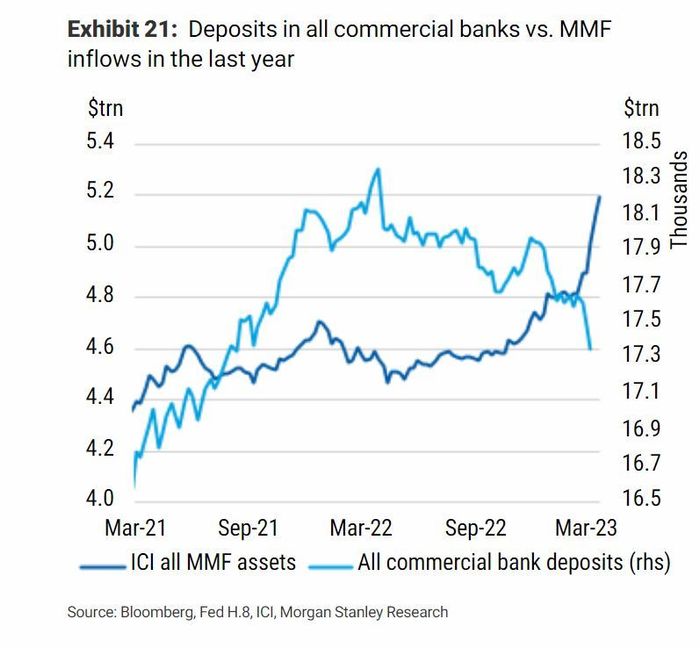

Analysts and money-fund portfolio managers say that much of their inflows are coming from bank deposits, which have continued to see outflows.

Savers pulled $125.7 billion from the banking system in the week ended March 22, the latest data available from the Fed, representing outflows from banks for nine straight weeks.

MORGAN STANLEY

While higher returns might be a welcome change for savers and investors who earned essentially nothing from their deposits for more than a decade following the financial crisis, some experts worry that relatively attractive yields on offer at the RRP could exacerbate concerns about stability in the banking system.

After all, both money-market funds and short-dated Treasury bills offer yields that are substantially higher than the average interest rate offered to customers by U.S. banks, which currently stands at less than 0.5%, according to data from Bankrate.com.

“It’s cash under the mattress, but on an institutional level,” said Steven Kelly, senior research associate at Yale’s program on financial stability, about money parked in the RRP. “It’s dead money.”

Treasury Secretary Janet Yellen recently highlighted similar issues during a speech about financial stability, where she cited money-market funds as a potential source of risk to the banking system, saying “the financial stability risks posed by money market and open-end funds have not been sufficiently addressed.”

What’s more, if banks curtail lending because their deposit base shrinks, it could further tighten financial conditions and potentially lead to a deeper economic recession.

What’s a ‘reverse repo’ and why is the Fed involved?

In September 2013, the Federal Reserve launched its daily reverse repo facility to allow money-market funds, banks, primary dealers of Treasury securities, government-sponsored enterprises and other eligible counterparties an avenue to soak up a surfeit of cash flowing into the financial system via the Fed’s bond-buying program, known as quantitative easing, according to Kelly and a Q&A published last month by the New York Fed.

It’s called the reverse-repo program because the Fed is putting up the securities, while money-market mutual funds and other counterparties are putting up the cash, at a set rate of return. Each counterparty is limited to pledging $160 billion to the RRP per day.

Shawn Lyons, portfolio manager at Franklin U.S. Government Money Fund, which has roughly $5 billion in assets, said his fund started using the RRP back in the months after it was introduced.

“We’re definitely using [the RRP] and we have for a long time,” Lyons said in a phone interview with MarketWatch. “You can get 4.8% overnight, that’s really attractive right now,” he added.

One benefit of using the RRP is that funds like Lyons’ can avoid the duration risk that comes with buying Treasury bills and bonds. As with the collapse of Silicon Valley Bank, investors risk booking losses if they must sell older, low-coupon bonds that have fallen in value in the past year.

With the RRP, “you park the money overnight, and then you get your money back, whereas with a T-bill, they’re weekly or monthly,” Lyons said.

“If you need that liquidity, you don’t have to sell your bill, which could lead to a gain or a loss,” he said.

This post was originally published on Market Watch