The stock market does not suffer from seasonal weakness between now and Christmas.

You may have never heard about a supposed pre-Santa lull on Wall Street. Given the media’s relentless focus on a so-called Santa Claus Rally, you probably have been focused instead on the possibility of stock market strength in the weeks leading up to Christmas.

But you should never underestimate analysts’ appetite for slicing and dicing the data in new ways. And one such slice of the historical data is suggesting that, because we’re in the first year of the presidential cycle, stocks will go sideways between now and Christmas, which is when year-end strength kicks in.

Don’t believe it.

There’s no seasonally based reason to expect the stock market’s performance leading up to Christmas to be any different than it is over any other five-week stretch of the calendar. That doesn’t mean the stock market won’t exhibit weakness in coming weeks. But if it does, it won’t have anything to do with it being late November and the first weeks of December in the first year of the presidential cycle.

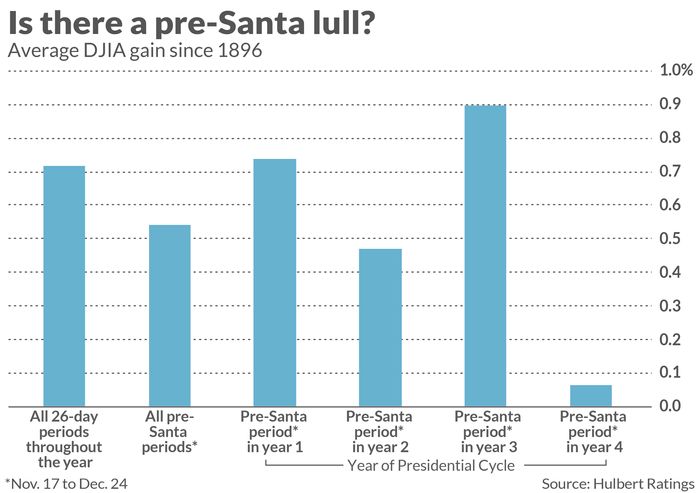

The accompanying chart, below, focuses on the Dow Jones Industrial Average

DJIA,

back to its creation in 1896, measuring its average return between Nov. 17 and Dec. 24. Its average gain over this five-week period is 0.54%, versus an average of 0.72% for all five-week periods across the entire calendar. If I were to have stopped the analysis at this point, you would have some basis for thinking there is a pre-Santa lull — though the difference of 18 basis points is of doubtful statistical significance.

But notice the results when segregated by year of the presidential cycle. The first year of that cycle — this year, in other words — has produced an average DJIA gain of 0.74% in this pre-Santa period. While the 2-basis-point margin above the overall average is not statistically significant, the more important takeaway is that there is no reason to expect this year will be a below-average one for the stock market.

Investment lessons

Even if the stock market’s performance over the five weeks prior to Christmas differed in a statistically significant way from the long-term average, however, the pattern would have to jump over another hurdle before it would make sense to bet on it. That hurdle is the need for a theoretical justification for why that pattern should exist in the first place.

I am aware of no such explanation in the case of a pre-Santa lull in the first year of the presidential cycle. And I’m not holding my breath that any will ever be found.

That’s because this pattern, as well as most other seasonal patterns, are the result of shameless data-mining exercises. As any statistician can attest, upon torturing the data long and hard enough you can get it to say almost anything you want.

My favorite example of data mining comes from David Leinweber, head of the Center for Innovative Financial Technology at the Lawrence Berkeley National Laboratory. He found that you could explain 99% of the variation in the S&P 500’s

SPX,

return with a simple model containing just four inputs: Butter production in Bangladesh, American cheese production, and American and Bangladeshi sheep populations.

This isn’t to say that no seasonal patterns exist. A few do, and they rest on strong theoretical foundations.

But most do not, so you should be skeptical whenever you read or hear of another analyst “discovering” some uncanny pattern in the stock market. Your first instinct should be to think back to Leinweber’s example and how obviously irrelevant to the stock market are butter, cheese and sheep in Bangladesh and the U.S.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com.

This post was originally published on Market Watch