The perfect inflation hedge hasn’t been found. That’s unfortunate, since U.S. inflation has taken a big jump, intensifying the search for an investment that will thrive during times of high inflation.

A perfect inflation hedge should satisfy two distinct criteria, and no one yet has figured out how to construct an investment vehicle that does more than satisfy just one of these two goals. These two criteria consist of a short-term goal of being correlated with inflation, and a long-term goal of outperforming inflation.

Stocks provide a good illustration. Over the past 200 years they have produced the highest real return of any major asset, which is why equities are considered by many to be a good inflation hedge. Yet, when measured over the short term, stocks typically are inversely correlated with inflation — falling when inflation heats up, and vice versa.

Gold

GC00,

doesn’t do much better, despite its reputation as the ideal inflation hedge. On the one hand, its short-term correlation with inflation is better than stocks, but not by much. The correlation coefficient between monthly changes in gold bullion and the Consumer Price Index (CPI) is just 0.12 since 1970, versus minus 0.06 for the S&P 500

SPX,

If gold were perfectly correlated with inflation, of course, this coefficient would be 1.0.

On the other hand, gold over the long term hasn’t produced a real return as good as stocks: Over the past 50 years, the S&P 500’s annualized total return has been three percentage points better than gold. In other words, gold does a better job satisfying one of the ideal inflation hedge’s two goals while doing a worse job on the other.

What about TIPS — Treasury Inflation-Protected Securities? They are an extreme example, since they do an unparalleled job of satisfying the short-term goal while failing to satisfy the long-term goal. That’s because, by design, the TIPS yield is pegged to changes in the CPI. Yet TIPS do a very poor job of fulfilling the long-term goal. In fact, their real yield currently is negative.

ETFs designed to be inflation hedges

Several different exchange-traded funds have been created in an attempt to fill this void in the investment landscape. Yet they largely come up short, according to an analysis conducted by Nicholas Rabener, founder & CEO of FactorResearch in London. He reports that the correlations of these ETFs with the CPI are surprisingly low, and the funds have a spotty record at best of producing positive real returns.

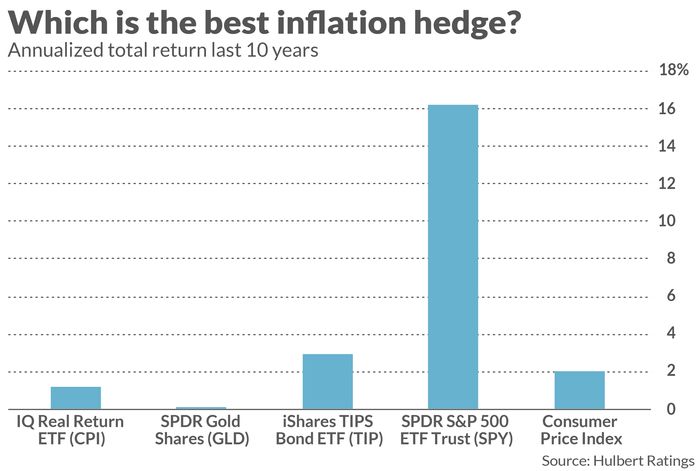

The inflation-themed ETF with the longest record is the IQ Real Return ETF

CPI,

which was created in October 2009. The ETF’s goal is to “provide investors with a hedge against the U.S. inflation rate by providing a ‘real return,’ or a return above the rate of inflation, as represented by the Consumer Price Index (the ‘CPI’).” Over the past decade this ETF has produced a 1.2% annualized return — 0.8 percentage points below the CPI’s 2.0% return on an annualized basis.

At the same time, this ETF has shown a low correlation with inflation. Over the past decade, for example, the correlation coefficient of monthly changes in the ETF and the CPI is 0.14 — barely higher than the 0.12 coefficient I found in the case of gold.

I reached a similar conclusion when correlating this ETF with changes in expected inflation, rather than realized inflation. For expected inflation, I focused on the inflations expectation model constructed by the Cleveland Federal Reserve Bank. The correlation coefficient in this case was 0.12, worse than the 0.14 figure that emerged when focusing on realized inflation.

Another inflation-focused ETF is the ProShares Inflation Expectations ETF

RINF,

which was created in January 2012. Since then it has lagged the Consumer Price Index by 2.8 annualized percentage points, with a return of minus 0.8% annualized versus plus 2.0% for the CPI.

On the upside, the RINF’s correlation with inflation is higher than for the IQ Real Return ETF, though still low. The correlation of monthly changes for RINF and realized inflation is 0.30, and 0.23 when focusing on expected inflation.

To be fair, the jury is out on these two ETFs, since most of their history has been in a low-inflation environment. It’s impossible to know how they will perform if higher inflation turns out to be more than transitory. The jury is also out in the case of several inflation-themed ETFs with even less history.

But we nevertheless have enough history to be skeptical that there’s an investment instrument which simultaneously satisfies both the short- and long-term goals of an ideal inflation hedge. You therefore need to decide which of the two goals is most important to you, and then find the investment which most satisfies that goal for the least risk.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

More: This is your brain on high inflation: ‘scarcity’ and financial anxiety

Plus: Why the hottest inflation in 3 decades isn’t rattling stock-market bulls

This post was originally published on Market Watch