It’s time I cast a critical eye over a FTSE 100 share in my portfolio that’s failed to move up lately. Is it time to sell or buy more?

Interest in commodity giant Glencore (LSE: GLEN) has faded lately judging by Fool traffic and its own share price performance. Yet I have a big position that I still expect to pay off over time.

There are times when the Glencore share price can shoot the lights out, but this isn’t one of them. That’s a shame, because I bought it last year hoping for growth and income, but have been disappointed on both fronts.

LSE hidden gem

Glencore shares have fallen 1.77% over the last year, against a 10% rise on the FTSE 100 as a whole. They’ve thrashed the index over five years though, up 68.15% against 8.59%. I think they’ll do it again, when conditions change.

I judge the success or failure of my investments over a minimum period of five years, ideally much longer. Patience is particularly important when investing in cyclical stocks, and the natural resources sector is arguably the most cyclical of all.

For years, Glencore boomed on demand from China, which gobbled up around two thirds of all global commodity production. China isn’t booming any more. While its GDP looks set to grow a solid 5% this year, we have to recalibrate our sights.

China has a more mature economy. Growth has to slow. Its shrinking population won’t help.

These concerns are reflected in Glencore’s share price, with the stock trading at just 13.7 times forward earnings. In April last year, its price-to-book ratio spiked to 2.34. Today, it’s back down to 1.63. It has been cheaper though. Let’s see what the charts say.

Chart by TradingView

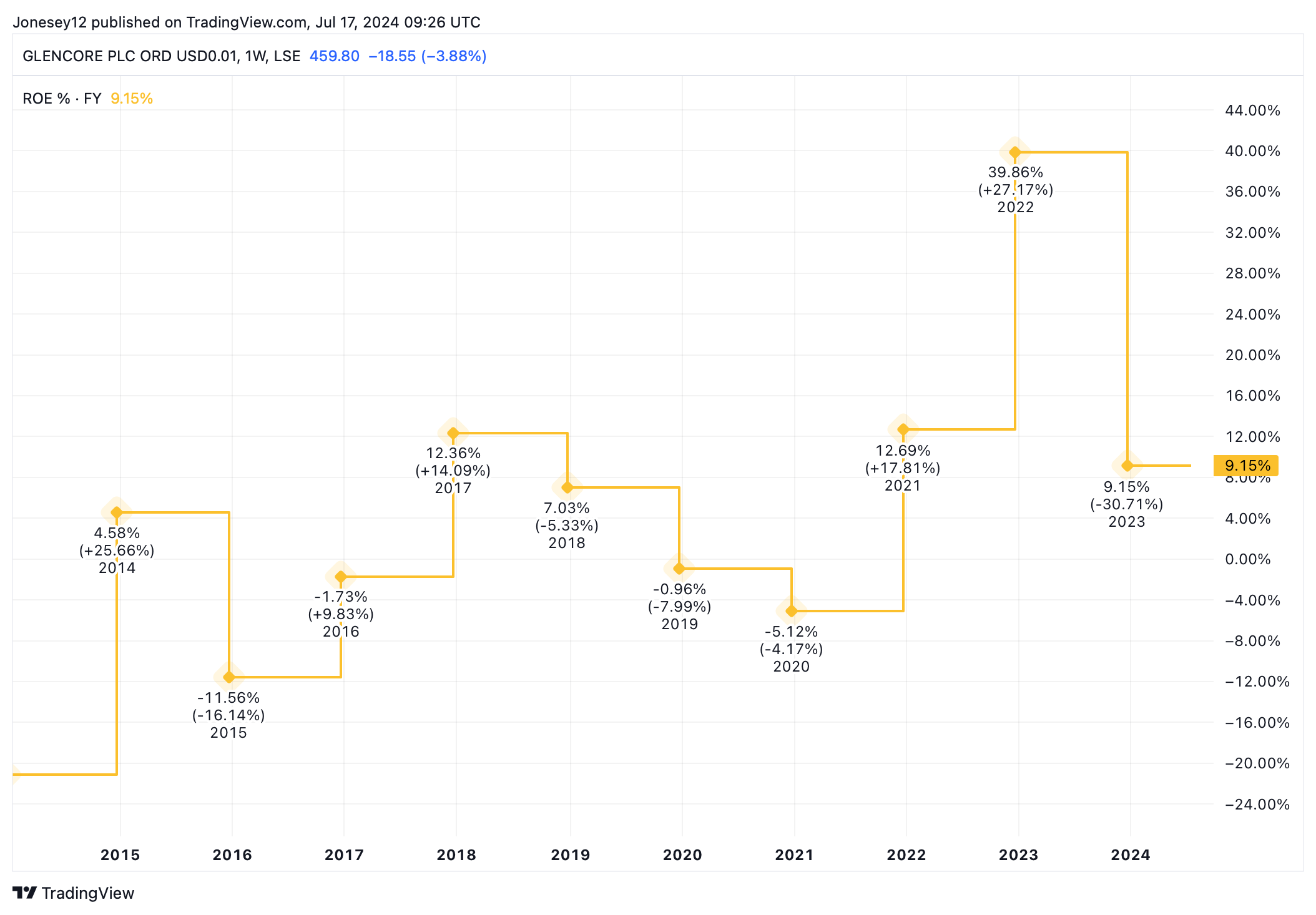

The group’s return on equity has also slumped, as this chart shows.

Chart by TradingView

Glencore’s expected to be a beneficiary of the green transition, as it produces the metals and minerals required by renewables infrastructure and electric vehicles, but it’s not all one-way traffic. Legal & General recently sold its stake due to concerns over its shift into thermal coal.

My big recovery play

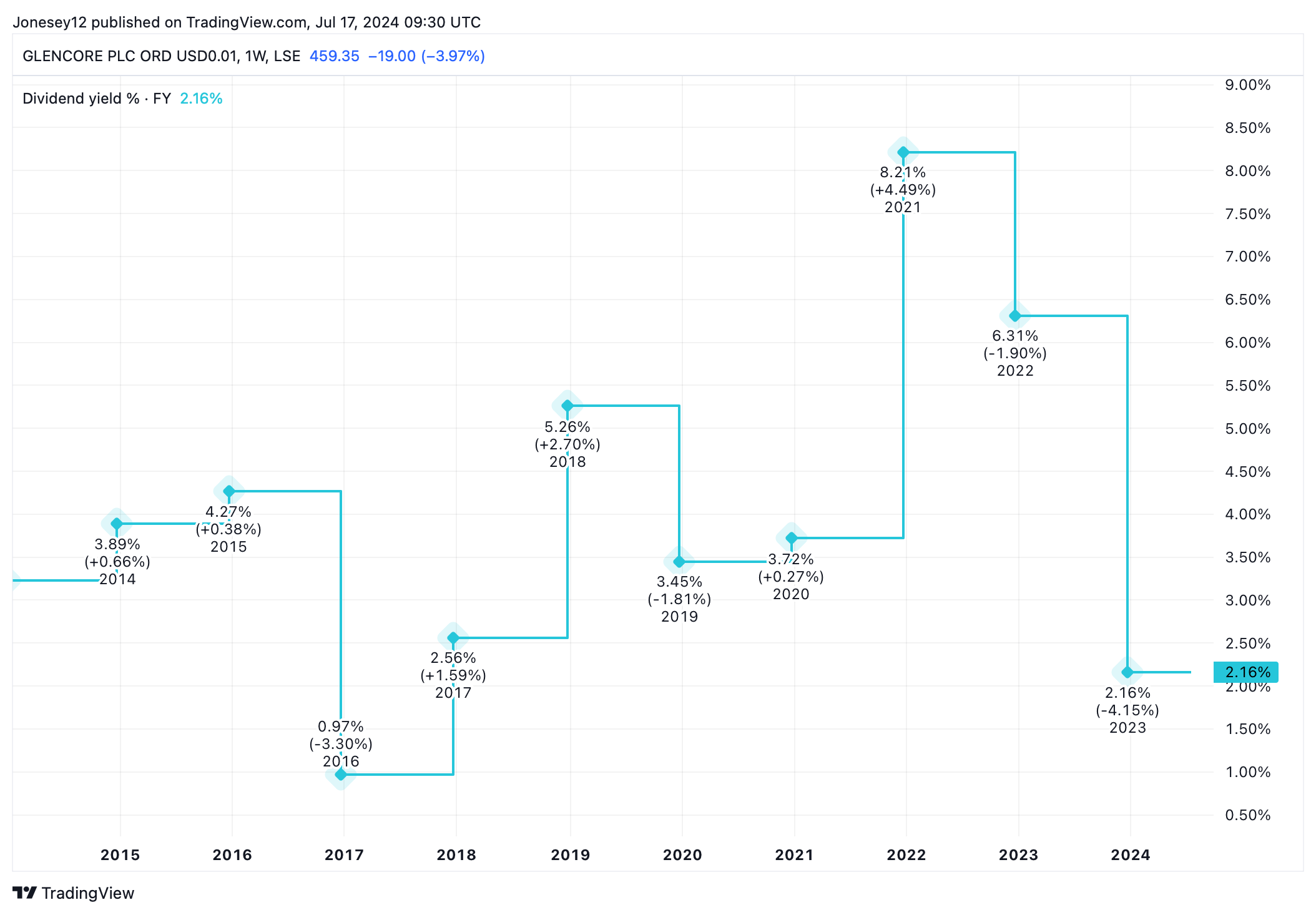

When I bought Glencore, the shares were yielding almost 6%. Dividend forecasts have now dropped sharply to just 2.23% in 2024 and 3.3% in 2025, as this chart shows. That’s a crushing disappointment for a dividend hound like me.

Chart by TradingView

Looking at these figures, it isn’t hard to see why Glencore has fallen out of favour.

Analysts are optimistic though, with 14 setting an average price target of 526.3p. That’s more than 15% higher than today’s price of 456p.

I’m optimistic too. Selling a commodity stock at this point in its cycle would be daft. Also, I believe Glencore will revive when interest rates are finally cut, and investor sentiment picks up.

I expect my shares to recover at pace. I just don’t know when. I have a large position so don’t need to buy more. But I’m definitely not selling.

This post was originally published on Motley Fool