A half-decade after the yield on the German government bond first turned negative, leading the way for a swath of European yields, global investors are starting to feel the “gravitational pull to zero” on returns, according to Deutsche Bank’s Jim Reid.

And it isn’t a pleasant feeling.

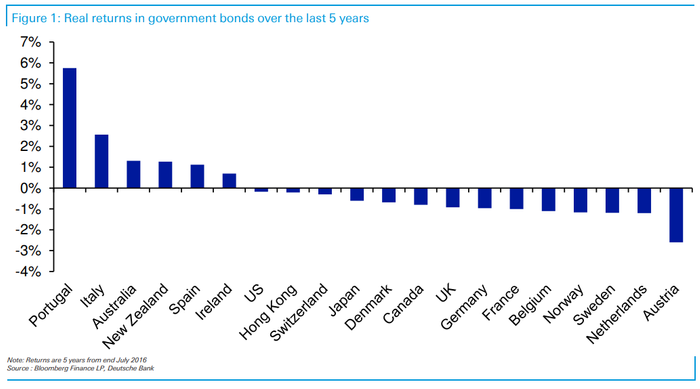

In a Thursday note, the macro strategist — see chart below — shows that real, or inflation-adjusted, returns in government bonds are now negative across a swath of countries in the five years to the end of July (the last point for all inflation data to be available).

Deutsche Bank

Even U.S. Treasurys have seen slightly negative real returns, he noted. Although 10-year Treasury yields

TMUBMUSD10Y,

were still around 1.5% in July 2016, that wasn’t enough to keep up with annual inflation over the period.

The 10-year Treasury yield ticked up around 2.2 basis points Thursday to 1.329%. Stocks were modestly lower, with the Dow Jones Industrial Average

DJIA,

down around 65 points, or 0.2%, while the S&P 500

SPX,

also edged down around 0.2%.

The chart comes five years after the yield on the 10-year German government bond

TMBMKDE-10Y,

fell below 0% for the first time. Although the bund, as its known, was joining Japan

TMBMKJP-10Y,

and Switzerland in subzero territory, the move marked a subsequent move below zero for many other European bond markets, Reid noted.

“These negative returns shouldn’t be a surprise when you have no or negligible coupons and any kind of inflation, but it’s a reminder of the immense financial repression at hand, and it’s probably the first time in over 40 years that the rolling 5-year real return for so many government bonds is now negative,” Reid wrote.

And what about those peripheral European and other high-yielding bonds that have maintained positive real returns over the period? That’s partly explained by their starting point in July 2016, he said, but noted that at current yields they will struggle to replicate past performance.

To add insult to injury, bond-market bulls who defied the consensus and correctly called for yields to remain near rock-bottom levels aren’t benefiting when it comes to returns. Bond prices rise when yields fall, providing capital gains.

“It still seems an asymmetric risk-reward asset class from here unless you believe [central bank digital currencies] will revolutionize interest-rate setting in the years ahead and allow rates to go deeply negative and drag bond yields even further down as a result, thus allowing capital gains to offset large negative carry,” Reid said.

This post was originally published on Market Watch