What do we want from a passive income stock? First we want a good dividend to create the income. And it’s passive because, well, we don’t have to do any work once we’ve bought it.

But then I want a stock that I believe will keep its dividend growing, at least in line with inflation, for the next 10 or 20 years.

And I want it to look cheap on fundamental measures. I know a sustainable high dividend yield can imply that. But I want a chance of stock price appreciation too, as a bonus.

Insurance dividends

I’ve always liked insurance stocks, and I’m thinking of adding Legal & General (LSE: LGEN) to my current Aviva holding.

I am a bit heavy in financial stocks, and that’s a caution for passive income investors. Very often, we’ll see a lot of the biggest dividends coming from the same sector, and that tempts us to focus.

But I’d say diversification is more important than chasing the best dividends. So, if I do buy Legal & General shares, I’ll next look to diversify a bit more.

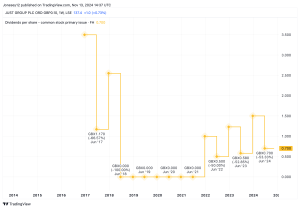

Irresistable dividend?

I find the forecast 9.2% dividend yield very hard to resist. Dividends from the sector can be volatile, and so can share prices. And that’s probably the biggest risk, which can make it easy to think a stock is cheap when maybe it really isn’t.

Still, I can handle short-term volatility, even if a lot of investors don’t like it.

And with forecasts suggesting the price-to-earnings (P/E) ratio could drop to under nine by 2026, there’s enough safety margin in the valuation. For me, at least, if not for everyone.

Sorely tempted

The BT Group (LSE: BT.A) dividend really does tempt me now. For years I’ve thought the company was paying out too much cash, while shouldering too much debt.

But since the board told us we’re passed the point of peak capital expenditure for broadband rollout, I’m seeing it in a new light.

The 5.5% yield isn’t the market’s biggest, and forward P/E multiples of around 10 aren’t the cheapest. But both beat the the FTSE 100 averages in their own ways.

Is there enough safety to beat the threat from debt? Is there more to come from the share price since it started rising this summer, or will the past five years of weakness continue?

I haven’t made up my mind yet. But BT is definitely on my passive income shortlist.

So many choices

I keep thinking of National Grid as possibly the best dividend stock I’ve never bought. I missed the big dip in May, though, as I didn’t have the cash ready.

Is the share price still cheap now the dividend has been diluted a bit? How safe are we from the chance it might happen again? Those are my big unknowns.

Maybe I should simply put more money into City of London Investment Trust, which has raised its dividend for 58 years in a row. But it might be fully valued compared to some of the other bargains out there.

Ah, so many dividend stock options, and not enough money to go round!

This post was originally published on Motley Fool