For me, Aviva (LSE: AV) shares are the ones that got away. After adding Legal & General Group and Phoenix Group Holdings to my portfolio, I decided I had enough exposure to FTSE 100 insurers and resisted buying a third.

I chose poorly. Over the last year, the Aviva share price has jumped 21.41%. By contrast, Legal & General has fallen 4.18% and Phoenix has dropped 3.17%.

To a degree, that doesn’t matter. I buy shares with a long-term view. I don’t judge their success over periods as short as 12 months.

FTSE 100 income star

However, Aviva is the easy winner over three years, too. In that time, it grew 33.95%, while Legal & General fell 9.46% and Phoenix plunged 19.19%.

It’s a bit odd. All three are in the same line of business, all three have high yields, all three look cheap. But Aviva has smashed it, and the others haven’t.

If I’d bought Aviva three years ago, when I first considered it, I’d now be sitting on a very pleasant total return of around 55%, with dividends reinvested. That would have turned a £5,000 investment into around £7,750.

So much for past performance. What really matters is where Aviva goes in future – and whether I should buy it today.

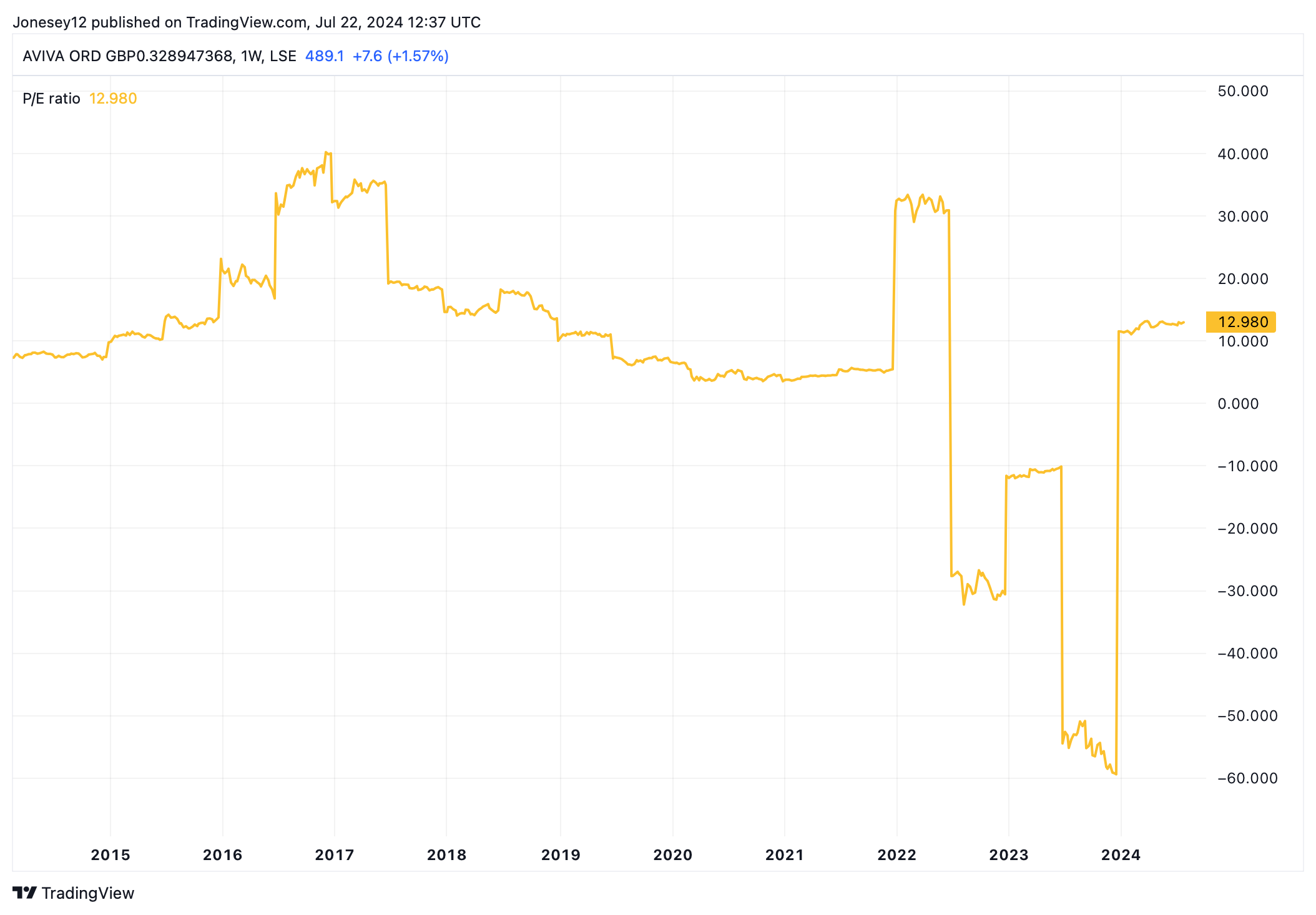

Trading at 11.2 times forward earnings, the shares aren’t as cheap as they were, with the price-to-earnings ratio rebounding sharply over the last year, as this chart shows.

Chart by TradingView

However, Aviva is still cheaper than Legal & General, which trades at 30.87 times earnings, and Phoenix at 16.35 times.

Good value

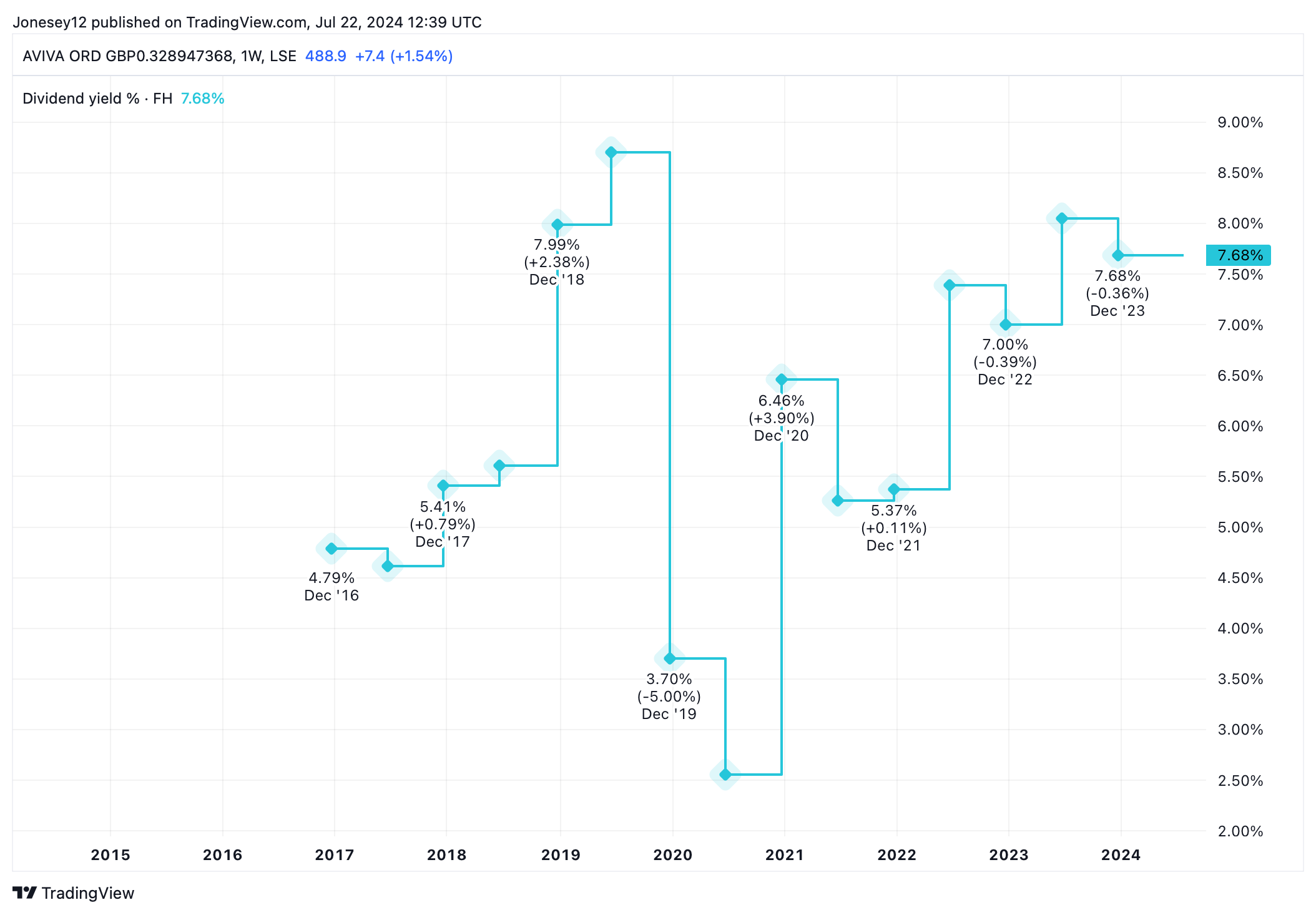

The dividend income is still for to die for. The yield has recovered steadily since the pandemic to 7.68%, as this chart shows.

Chart by TradingView

It may trail Legal & General’s 8.86% yield and Phoenix, which pays a blockbuster 9.73%. However, that is mostly due to their share price slippage. Markets reckon Aviva’s yield is sustainable. It’s forecast to hit 7.97% in 2025. The board also felt able to green light a modest £300m share buyback, too.

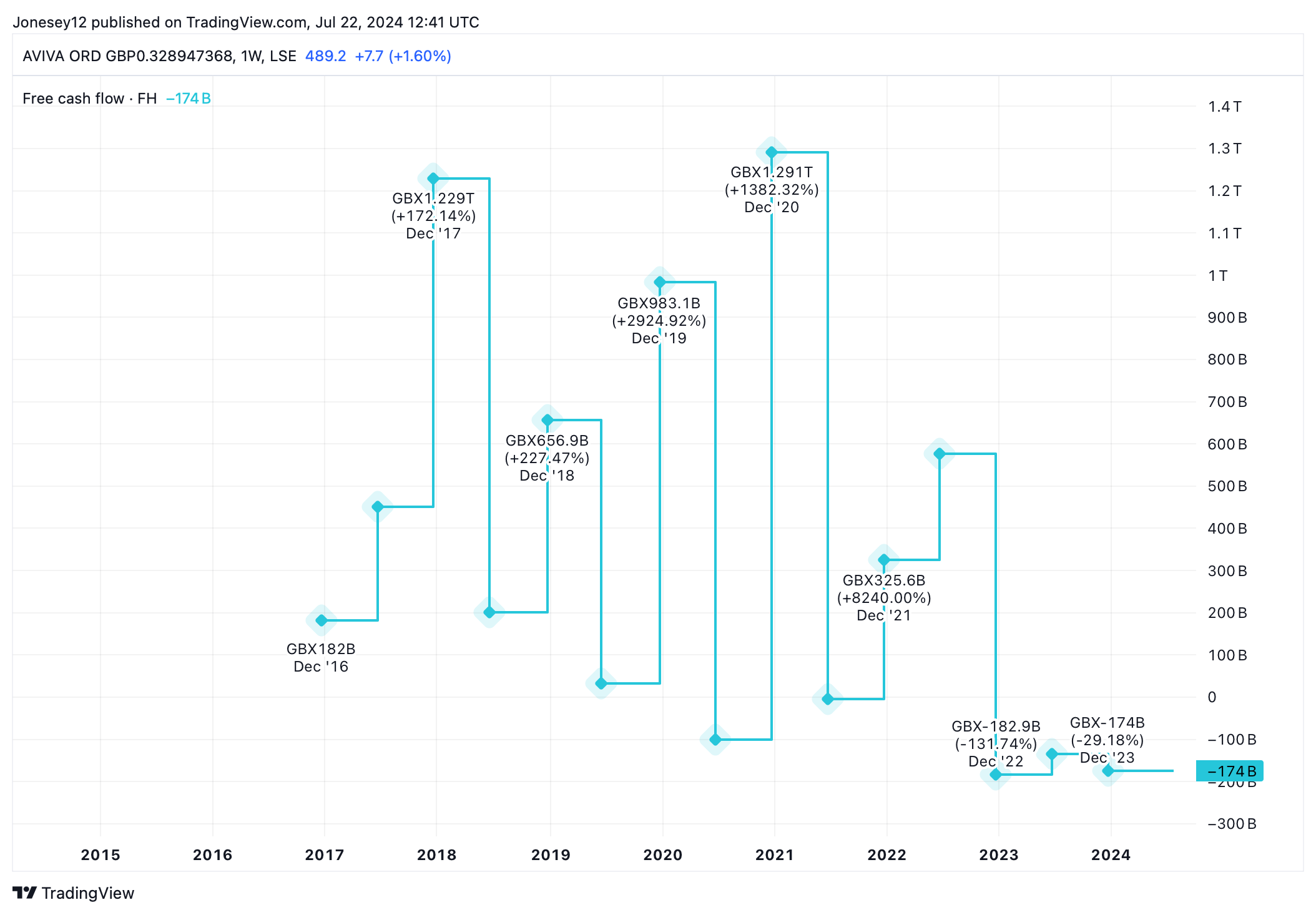

I am worried to see Aviva’s dividend cover slide to just 1.1 times earnings. That is pretty thin. Free cash flows have been falling, too, as this chart shows.

Chart by TradingView

Aviva’s enjoyed a strong start to 2024, with Q1 general insurance premiums up 16% year on year to £2.7bn, helped by strong rate discipline and new business. Protection and health sales increased by 5%, while wealth net flows jumped 15%.

Like all the high-yielding FTSE 100 insurers, Aviva’s dividends will look even more attractive when interest rates are finally cut. That might also light a fire under stock markets generally, boosting the value of hundreds of billions of pounds insurers hold to cover their liabilities.

But you know what? I’m not going to add Aviva to my portfolio today. It’s rare for the company’s shares to do this well. I have enough exposure to the insurance sector, and I don’t think it offers quite enough excitement to go seriously overweight. Instead, I’ll cross my fingers and hope my two sector laggards play catch up. It’s about time they did.

This post was originally published on Motley Fool