I invest in my ISA with retirement in mind. One day, when I decide to give up work, I’ll have a large nest egg that I can rely on to supplement my income and live a more lavish lifestyle. While it may seem like a sacrifice now, I know it’ll be worth it.

But what if that day were tomorrow? I have a while until retirement, but it’s a fun exercise and, more importantly, allows me to focus on stocks I think have real long-term growth potential. Here are two I’d buy today.

Tesco

I’d want to focus on blue-chip companies that I think can provide solid returns, like Tesco (LSE: TSCO). In the last year, the stock is up 25.6%.

At 309.4p, I think its shares look like good value at the moment. They have a price-to-earnings (P/E) ratio of 12.6.

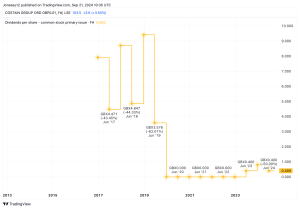

For my retirement, I wouldn’t also mind making some passive income. That’s why I like Tesco’s 3.9% dividend yield. That’s above the FTSE 100 average. Last year, its dividend per share payment rose 11% from 10.9p to 12.1p. After selling Tesco Bank, it also announced a special £250m dividend.

Dividends are never guaranteed. So, since I’m targeting stability, it’s good to see management has had an appetite to reward its shareholders in the last year or so. More widely, since October 2021, the business has bought back £1.8bn worth of shares.

The largest risk I see for Tesco in the years to come is competition, especially from budget rivals. They’ve become more popular in the last few years and have been successful in stealing market share.

But Tesco has incredible brand recognition and a massive customer base. That’s why I’d back it to succeed in the long run.

BP

With the theme of well-known blue-chip companies in mind, I also like BP (LSE: BP.). It hasn’t performed quite as well as Tesco over the last year. But it’s still up 7.9%.

I’m bullish on the stock for similar reasons I like the supermarket giant. For one, its shares look like good value with a P/E of 11.8. Its forward P/E is 7.4.

What’s more, it boasts a 4.7% yield. Just like Tesco, BP has also shown its willingness to give back to investors.

For example, the company has the aim to buy back $14bn worth of shares by 2025. It’s on track to buy back $3.5bn over the first half of the year. For 2023, its total dividend grew by 18%.

The biggest challenge for the company is the ongoing transition to renewable energy. You’d expect that as the world becomes greener, demand for BP’s products will dwindle. BP is cyclical too. So, I’d expect some volatility with its share price.

But, while the green transition poses a threat, demand for oil is actually set to rise over the next decade, which will benefit BP massively. With the original 2050 target for net zero now looking likely to be set back, that will also help the business.

This post was originally published on Motley Fool