At 30, it’s certainly not too late to open a Stocks and Shares ISA and start investing for the long run. With a maximum contribution of £20,000 annually, Britons can supercharge their wealth growing capabilities by using the ISA wrapper.

This wealth could be used to facilitate an early retirement and complement any pensions pots an investor may have. And investors don’t have to max out their ISA contributions to build a portfolio that could generate significant passive income.

Here, I’ll explain how a 30-year-old could build a large retirement pot in a Stocks and Shares ISA by contributing just £500 a month.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Caution to the wind

Many novice investors are motivated by get-rich-quick stories, but this can prove dangerous, especially if the investors in question elect to concentrate their investments in one or two stocks. After all, if an investor loses 50% of their investments, they’ve got to gain 100% just to get back to where they started.

However, the path to success lies in diversification, and diversification doesn’t mean slow or low returns. For instance, my portfolio surged 79% between 1 March and 30 December despite having around 25 stocks, bonds, and funds in my portfolio.

Diversification also protects us against any poor investment decisions we might have made. And trust me, even the best researched investments can go wrong: I thought Vistry Group was a winner in the UK housebuilding sector — it turns out that the company had vastly underestimated costs.

Sensible investments can generate big returns

An investor with £500 a month could look to achieve this diversification by making one or two investments per month. But there’s nothing to stop each of these investments being the next big winners or multi-baggers, even though modest growth is all we need to leverage compound returns over the long run.

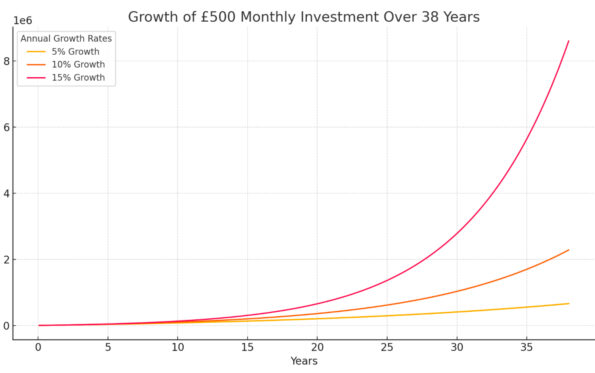

At 30, most people will be expected to work for another 38 years. So, let’s visualise how £500 invested monthly could grow over 38 years.

As we can see, the rate of growth proves to be very important as the portfolio compounds over time.

- 5% growth: the portfolio reaches approximately £574,000.

- 10% growth: the portfolio grows significantly more, reaching around £1,518,000.

- 15% growth: the portfolio soars to a substantial £4,069,000.

This money can be withdrawn tax free!

A starting point

Investors could consider a stock called Celestica (NYSE:CLS) as a starting point with their £500 per month. This Canadian company has surged on the growing demand for computer hardware on the back of the artificial intelligence (AI) revolution.

Driven by growth in its Cloud Computing Solutions, the business has recorded approximately 70% growth in earnings over the past 12 months. And moving forward, the company’s earnings are expected to grow by 28% annually over the next three to five years.

While this stock has surged already, the evidence suggests it’s still undervalued. At 24 times forward earnings and with a price-to-earnings-to-growth (PEG) ratio of 0.88, it trades at a considerable discount to tech peers.

A concentration of sales among 10 clients is one reason for concern, and we could see some profit taking after the recent bull run. However, it’s a stock worthy of consideration. It’s also my biggest holding, which I recently topped up despite a 250% rally since my first investment.

This post was originally published on Motley Fool