Kendra Brooks arrived at John F. Kennedy Boulevard in Philadelphia’s Center City, the downtown corridor bustling with shops and office towers, with a single goal in mind.

“I needed to make more money,” Brooks, a Black single mom of four, said of her mindset.

Brooks walked into an office building that housed a Philadelphia branch of Eastern University and did exactly what she was supposed to do, at least according to policymakers, educators and the data. She got more education by enrolling in an MBA program. It was 2007, and Brooks wanted to cash in on a deal fundamental to our nation’s understanding of itself: If you go to school, study hard and graduate, your life will be financially stable, your children’s lives even better.

But the MBA wasn’t enough to get Brooks the raise she wanted at the nonprofit organization where she worked for 17 years, coordinating programs for children with disabilities. Without the extra money she was counting on, Brooks found managing her roughly $80,000 in student debt, along with paying for housing and providing for her kids, impossible. Brooks fell severely behind on her payments and became victim to one of the harsh consequences of defaulting on a federal student loan — the government started seizing her wages to repay her debt. As the Great Recession raged, Brooks lost her job amid government funding cuts.

“I had exhausted my savings, I lost my house, lost everything,” Brooks said.

More than a decade later, Brooks is current on her student loans, but the specific challenges student debt poses to Black women persist. Over the past few years, there has been a growing recognition among policymakers, scholars and educators that student debt, a tool originally conceived to increase economic mobility, is instead exacerbating the racial wealth gap. It’s a dynamic that underpins many of the arguments in favor of canceling student debt.

For Black women, the weight of the loans can be particularly heavy. They face racial and gender discrimination in the labor market, where an advanced degree is often the only way for them to compete. There is also pressure on Black women to care for their families and communities. These systemic factors create obstacles for Black women as they try to realize the promise of higher education. Many are looking to the government to act.

“It feels like we have set up a terrible bargain with people and just blame them for doing the thing we always told them to do,” said Dominique Baker, an assistant professor of education policy at Southern Methodist University.

There is also a growing tension between those who see the drive for advanced or otherwise costly degrees that may not pay off as a sign the college finance system is broken and those who see the credentials as an investment individuals chose to make — and for which the government shouldn’t be responsible for bailing them out.

“The idea that you go to Penn and you’re paying a total of 70,000 bucks a year and the public should pay for that? I don’t agree,” President Joe Biden said earlier this year, referring to the Ivy League institution in Brooks’ home city.

To some, Brooks’ challenges with student loans may seem like bad luck or a quirk of graduating from school during an economic downturn. Brooks, however, contends that there must be significant changes to assist people struggling under the weight of student debt, especially Black women. Her experience is part of what is driving Brooks, now a member of Philadelphia’s City Council, to pressure Biden to cancel student debt.

“We’re taught, especially as a Black woman, that in order to succeed and be able to take care of family, you have to have a college degree,” she said. “People are selling us this American dream that is so hard for us to obtain because we don’t have a lot of generational wealth. We end up taking on so much debt in order to achieve that.”

***

Brooks’ personal experience with student debt haunts her. After years of challenges repaying her debt, she is in good standing on her loans thanks in part to her current six-figure job as a Philadelphia council member. But she is worried about her children’s future.

Brooks’ oldest child left college and returned home when Brooks could not afford to pay her tuition any longer, though she ultimately finished school after joining the military. Brooks’ next eldest daughter decided to skip a traditional college education and instead enrolled in cosmetology school. Now, as Brooks prepares her two teenagers for college, she’s encouraging them to find scholarships so they can avoid taking on loans.

Brooks, 49, is shielding her children from student loans in other ways too. “I’m trying to prevent my daughters from doing the same — I’m trying to prevent them from getting into debt by being the one that is paying off their loans,” she said.

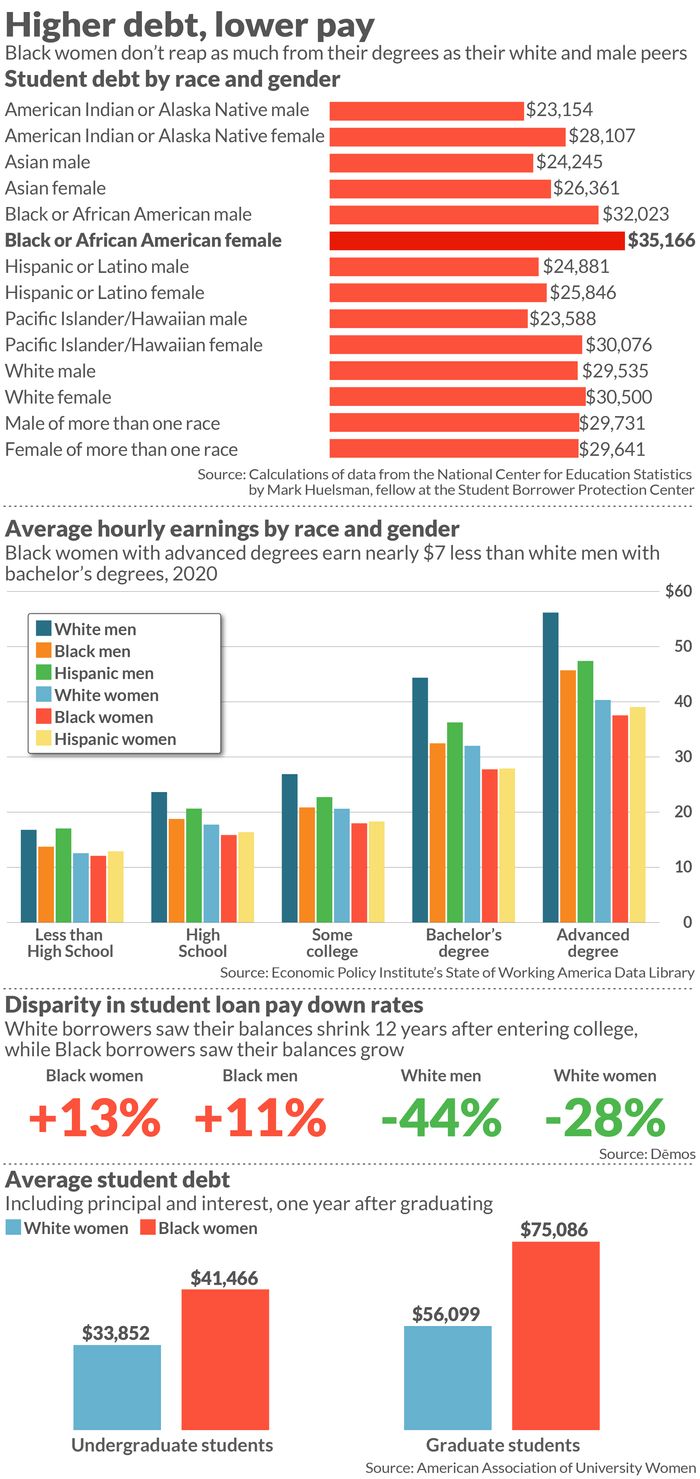

Black women face a unique combination of barriers when it comes to succeeding in the marketplace and paying off their student debt. For one, they borrow more on average. Black borrowers, regardless of gender, tend to have higher student debt loads than their white peers because of decades of policies that blocked Black households’ access to wealth building, such as redlining. But of those students who graduated with a bachelor’s degree in 2016 and borrowed, Black women had the highest average debt load of any demographic group at $35,166, according to an analysis of data from the National Center for Education Statistics by Mark Huelsman, a fellow at the Student Borrower Protection Center.

Once Black women graduate, they can face labor market discrimination that limits how much they earn. A Black woman with a bachelor’s degree was paid $27.76 an hour on average in 2020, according to the left-leaning Economic Policy Institute’s State of Working America Data Library, compared to $44.37 for a white man and $32.02 for a white woman. Black women with advanced degrees were paid $37.55 an hour — nearly $7 less than white men with only a bachelor’s degree.

Fused together, these factors make it difficult for Black women to make progress repaying their loans. Twelve years after entering college, the student loan balances of Black women grew by 13% on average, according to a 2019 analysis from Demos, a left-leaning think tank. During the same period, white men paid down 44% of their balances on average.

Terrence Horan/MarketWatch

One of the many arguments against canceling student debt, particularly without limiting the amount discharged or putting a salary cap on who is eligible, is that it’s a policy that will disproportionately benefit the well-off. Borrowers with the highest debt loads will see the most relief as a result of the policy, at least as measured by dollars, the argument goes. A large student loan balance is often the result of a graduate degree, and those with graduate degrees tend to earn more.

But as Brooks’ experience illustrates, a college or graduate degree doesn’t always translate into earnings that are high enough to service the debt.

“Any bit of debt cancellation will be beneficial to this population,” said Fenaba Addo, an associate professor of public policy at the University of North Carolina at Chapel Hill who studies race, wealth inequality and student debt. Not addressing these challenges could have consequences for this group and the economy broadly, she added.

“Do we want to have a generation of, in this case, Black women, who are paying debt throughout their entire adulthood so when we turn around they may not have saved for retirement?” Addo asked.

When Alicia Suggs decided to go to business school, she assumed the degree would come with the trappings society associates with an MBA. “You’re going to leave with a six-figure job and you’re going to work at a Fortune 500 company,” Suggs said she remembers thinking. Still, she kept costs relatively low by attending Baruch College’s Zicklin School of Business, which is part of the City University of New York system.

Suggs graduated in 2011 with more than $100,000 in student loans and discovered the degree wasn’t a ticket to prosperity. Suggs had hoped the MBA would help advance her career in the health insurance industry, and facilitate a transition from the payer side of the business to the provider side.

Suggs landed a job she had wanted, but during the hiring process discovered that a nuance in the job description meant she wouldn’t get the MBA pay bump she desired. The company had said it preferred candidates to have an MBA, but the degree wasn’t technically required. The job did not come with the six-figure salary she coveted.

“I always saw it as, ‘You want the Chanel bag for cheap,’” Suggs quipped. “They want candidates with that degree, but they’re not going to pay for it.”

Alicia Suggs’s first post-MBA job didn’t come with an MBA salary.

Courtesy of Alicia Suggs

As Suggs made her way through the corporate world, she found it would take more than the MBA to break through the close-knit, mostly white and male upper echelon of her industry.

The data backs up her experience. Of the 532 Black women who graduated from Harvard Business School between 1977 and 2015, roughly 13% made it to a high-level executive position, compared to 40% of non-Black Harvard MBA graduates overall. That’s according to an analysis of career pathways at the school by Anthony Mayo, a senior lecturer at Harvard Business School.

“We just thought as long as we cross our t’s and dot our i’s and do everything we’re supposed to do, we’ll be fine,” Suggs said of her mindset. “That’s not the way the cookie crumbles. I realize it’s a lot more political than the piece of paper.”

At 38, Suggs still works in the health insurance industry and has navigated those dynamics to reach a place in her career where her salary can cover her loans and other expenses. She periodically throws bonus money at the debt in hopes of shrinking it more quickly. Still, she doesn’t expect to be free from her loans until her mid-50s. “I’m paying almost $1,000 a month for student loans — it seems like a rent,” she said.

Now, Suggs is hopeful the Biden administration will take action to cancel or mitigate the collective $1.7 trillion in student loans she and other Americans are saddled with — and she doesn’t want to be excluded.

“I just hope that they don’t have a salary cap, because there are some people that have pushed the barriers in terms of getting their career to a certain place that still need that help,” Suggs said.

***

When Heather Pinckney went to law school more than 20 years ago, she noticed the difference between her experience — borrowing for tuition and basic necessities — and that of many of her peers who “had no concerns because their parents were paying their bills,” she said.

Pinckney founded her own law firm specializing in criminal defense and family law, but two decades into her career and now 44, she’s still repaying her student loans. Her bill is about $900 a month, more than half of her monthly mortgage payment. Pinckney said she put off trying to buy a house for years because she was so concerned about her debt.

“It’s crazy that I can’t imagine the day when I’m not paying,” she said. “I’m just so used to giving these people money.”

Heather Pinckney is more than 20 years into her career and still paying her student loans.

Courtesy of Heather Pinckney

Like many Black women, Pinckney can’t shake the idea that both her gender and race have played a role in the way her loans have impacted her. But even as advocates and lawmakers build momentum for broader solutions to the student loan problem, based in part on the experiences of Black borrowers and women generally, little research and advocacy has focused on Black women in particular.

“We talk a lot about Black student borrowers broadly,” said Baker, the professor at Southern Methodist University. “We have less work that has been done that’s intersectional, that thinks about gender and race.”

Micaela Stevenson, a fourth-year medical student at the University of Michigan, is planning to live like a student once she graduates and opt for a residency program in an area with a low cost of living. Her goal is to aggressively pay down the $150,000 in debt she will likely owe at graduation. Stevenson, 24, wants to be prepared for other life events, like buying a home and starting a family. But she also wants to be in a position where she feels financially comfortable enough to help those closest to her.

Micaela Stevenson plans to live like a student once she graduates from medical school to aggressively pay down her student loans.

Courtesy of Micaela Stevenson

Even in cases where there are men in the family who may have financial resources, “it’s kind of seen as a woman’s responsibility to take care of family in whatever ways that they need,” Stevenson said of the pressures Black women feel. Stevenson has already had experience helping family members get a new computer or car during her time in college and medical school.

“The idea of debt is a really big deal for Black women,” Stevenson said. “The whole idea of having another financial obligation just to get to a place where we can take care of ourselves and our families is really stressful.”

Research by Addo and Jason Houle, an associate professor of sociology at Dartmouth University, indicates that the gap in average student debt levels between Black and white borrowers increases in early adulthood. They also found that the gulf in parental wealth between Black and white households is associated with the racial differences in student debt accumulation and the growth in the Black-white debt disparity over time.

That suggests that one of the factors that may be contributing to the growing gap is that Black borrowers are more likely to use the funds they have to help out their families.

In addition to providing financial help, Black women often also provide another costly form of assistance to their communities: the unpaid labor they devote to building those resources up. There has been a growing movement for years to recognize the unpaid household work that women of all races do as contributions to the economy. But recent research from Nina Banks, an associate professor of economics at Bucknell University, aims to highlight the economic contribution of the unpaid community-building work performed by Black women.

Typically, this work is an effort to counter the impact of racial discrimination, which has led to neglect of or outright harm to the institutions and resources in the women’s communities. This work includes advocating on behalf of school children, organizing to decrease mortality rates among Black mothers and infants, challenging living conditions in public housing and protesting placement of industry that could have toxic impacts on the people and environment in the surrounding neighborhoods.

“Quite often, the reality exists for many Black women that we are seen as the go-to people, providers, people who care for others, people who get things done and take care of family, take care of community,” said Brittany Mobley, a public defender in Washington, D.C. “Black women have always had that burden and taken that on, and done so beautifully.”

Mobley owes roughly $216,000 in student loans. Though she’s hoping she’ll receive debt relief in 2023 through the Public Service Loan Forgiveness program, which allows borrowers to have their federal student loans canceled after 10 years of payments and work in public service, her loans have been a source of stress.

Brittany Mobley started a college fund for her nephew, in part so he won’t experience the emotional toll of excessive student loans.

Courtesy of Brittany Mobley

A few years ago, Mobley, 35, went for the first time to see a therapist, who helped her realize that she possessed a deep fear of spending money that was impacting her well-being. Part of the reason Mobley worries about the debt is because she is balancing the loan obligation with helping her family, by, for example, contributing to her elementary school-aged nephew’s college fund. Mobley started the fund because she doesn’t want him to experience the emotional toll of excessive student loans.

“Black women are going to school; they’re educating themselves at really high rates,” Mobley said. The debt is “another cross to bear along with everything else that we deal with and are forced to take on,” she said.

Given that on average, Black women earn a lower hourly wage than both male and female white or Hispanic workers with similar levels of education, pursuing higher education, even if it means taking on debt, is the rational thing to do, Addo said.

“They’re going to need the degrees; they’re going to need the signals that others don’t have,” Addo said. But the fact that getting the degree often doesn’t translate into a high enough salary to pay off the debt required to go to school indicates to Addo that “the system is broken,” she said. Black women had an average balance of $75,085.58, including principal and interest, in loans for graduate school one year after graduating, according to the American Association of University Women. That’s compared to $56,098.88 for white women.

“We need to think about ways that we can get people the education and the credentials they need without having to incur a lot of debt,” Addo says.

This post was originally published on Market Watch