High-poverty neighborhoods in the Twin Cities have seen an explosion of investor-owned homes since the Great Recession, a trend that has caught the attention of the Federal Reserve Bank of Minneapolis.

Sections of north Minneapolis already had higher-than-average rates of investor-owned homes before the subprime mortgage crisis, but a new Minneapolis Fed report shows the rate “grew worse as homes were foreclosed and scooped up by landlords.”

One concern is that deep-pocketed investors “make it harder for families, particularly lower-income households who are more likely to be people of color, to compete in the home-buying process,” according to the report.

Take northeast Minneapolis, with its high 41.7% poverty rate. Investors now own 30.7% of residential properties in the area, the highest level out of 20 Twin Cities-area census tracks studied by the Fed, using a new housing data tool it developed to study the impact of investor-owned homes on local communities.

Another concern is that investors flocking to poor neighborhoods with higher crime rates may lead to “a deterioration of housing quality,” according to the report, which pegged the overall investor ownership rate in the Twin Cities area at 4.1% this year, up from 1.8% in 2006.

“That is, they buy cheap properties, charge relatively high rent to tenants who have few housing alternatives, and provide minimal maintenance to maximize their profits,” the report said.

“Since the properties were bought cheap and there’s little prospect they’ll appreciate much in value for resale, there’s no incentive to take care of them.”

Housing inflation

The U.S. already faced an affordability crisis in housing long before the pandemic set in, sending prices through the roof.

In August, nominal U.S. home prices jumped a record 20.7% in the past year, resulting in a 17% decrease in the housing affordability rate in the past year through August, according to the latest edition of the Real House Price Index from title insurance company First American Financial Corp

FAF,

Institutional landlords in the past decade entered the fray, first by snapping up foreclosed homes for rental income. Most favor properties in lower-poverty areas with good schools — including Invitation Homes Inc.

INVH,

and American Homes 4 Rent

AMH,

— while successfully raising billions on Wall Street for their strategies.

A record of $13.7 billion of single-family rental bonds have been sold so far this year, according to Deutsche Bank data.

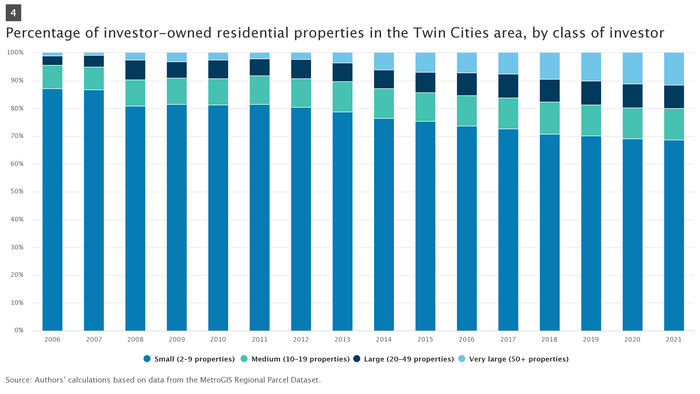

Importantly, the Minneapolis Fed report also breaks down homeownership by county and investor type. The results underscore the large, but declining, ranks of small landlords in the Twin Cities area, but also the growing segment of very large investors who own 50 or more homes.

Small owners cede ground to medium- and big-time landlords.

Federal Reserve Bank of Minneapolis

Lately, it hasn’t entirely been smooth sailing for some institutional players in the red-hot U.S. housing market. Earlier in November, Zillow Group Inc.

Z,

ZG,

announced it would abruptly end its home-buying business and that it expects to take a roughly $550 million loss on homes it bought.

Read: Zillow’s $1.2 billion of mortgage bonds in focus after company abruptly exits home-buying business

This post was originally published on Market Watch