I just took a look at Michelmersh Brick Holdings (LSE: MBH), on my penny shares watchlist. And I see it’s not a penny share any more!

Well, it’s actually only just out of the ‘less than 100p share price’ limit, exactly 100p at the time of writing.

But it is, for me, a top example of why we should ignore the share price and look at the underlying company.

Tough few years

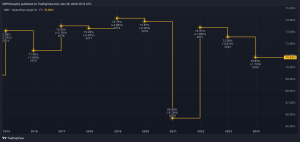

That chart shows the share price has had a tough few years.

The name gives it away a bit, but Michelmersh makes bricks and similar things, including roof tiles. And the building business hasn’t exactly been sparkling since, first, the pandemic gave it a kicking.

And now inflation and interest rates are so high that fewer people can afford to pay builders to cement Michelmersh bricks together for them.

But here’s where the investing lesson comes in. I reckon Michelmersh in the past few years has provided a great example of how investors should approach a penny stock.

Valuing penny shares

Penny stocks usually get to be penny stocks by having a hard time, like this. And the trick for us is to decide whether they’re going to the wall, or have a better long-term future ahead of them.

For me, the balance sheet is key. Profits might be down. But if a company has the means to make it through the hard times, it can shine when things look brighter.

Between early 2021 and late 2022, the Michelmersh share price pretty much halved to around the 75p mark. So what did things look like at the end of that period?

I think excellent, in one crucial way.

It’s cash that counts

The company recorded positive cash flow, and posted 2022 year-end net cash of £10.6m. Net debt can kill a down-and-out company, so net cash that year was tops.

I see the books had carried net cash in 2021 too. Not as much, at £7.7m, but pretty good in such a painful time. Remember, Rolls-Royce Holdings saw its net debt spiral to over £5bn that year.

In fact, perhaps ironically, the company was buiding up net debt going into the pandemic. But from 2020 onwards, every year has ended with net cash.

And that happy situation has persisted right up to interim results in 2024.

The future

There’s a forecast 4.6% dividend yield on the cards.

Earnings are predicted to rise, dropping the 2024 price-to-earnings (P/E) ratio of 14.5 down to 10.3 by 2026. Perhaps not super cheap, but I’d say fair value.

Volatility is my biggest fear in the next few years. Until we get back to a lower interest rate environment, I expect more ups and downs here. And there’s potential for competition with such a small-cap company, plus the industry this company operates in is very dependent on consumers feeling good about the economy.

But can anyone think of an industry that’s more likely to still be around a century from now than building? It’s got to be up there with energy, finance and food.

I considering a purchase here.

This post was originally published on Motley Fool