Lloyds of London insurer Beazley (LSE: BEZ) tends to fly under the radar of even the most avid FTSE 100 investors. It’s just not one of those stocks that catches the eye. Until you look at its performance.

The Beazley share price has jumped 32.74% over the last 12 months, at a time when the FTSE 100 rose a modest 7.77%. It’s up 83.84% over three years.

Beazley is a speciality-risk insurance and reinsurance business, which probably explains its unfamiliarity. Those who do know about it often shy away, because this puts it on the front line of climate change.

Can the Beazley share price continue to kick up a storm?

As the world warms, floods, storms and hurricanes and all the other weather woes heading our way are likely to drive up claims costs.

On 6 November the board said it was facing an estimated hit of between $125m and $175m from Hurricanes Helene and Milton. A good insurer should hedge for this, and Beazley breezed through, reiterating full-year profitability guidance after a solid Q3.

Insurance claims may be volatile but premiums have been rising steadily, up 6.9% to $4.63bn year on year. However, rates on renewal business flattened out after rising 5% last year.

As with any insurer, Beazley has to invest the premiums it receives. Here it did jolly well, with returns up 4.7% to $513m year to date amid increased exposure to equities and high-yield credit. Overall, investments and cash rose 15% to $11.43bn, soothing concerns over flat renewals.

When I looked at Beazley in July, I was impressed by a 155% jump in full-year 2023 pre-tax profit to a record $1.25bn.

Time to scope out this FTSE 100 stock

Half-year results published on 8 August showed profit at a record $728.9m, nearly double the previous year’s $366.4m. Beazley’s shares spiked on the day but have since idled (along with the rest of the FTSE 100).

Now here’s the thing. The Beazley share price may have grown more than four times faster than the FTSE 100 as a whole over the year, but it still looks great value to me, trading at just 4.83 times earnings. A price-to-revenue ratio of 1.1 also suggests good value. It means I’ll pay £1.10 for each £1 of sales.

The 13 analysts offering one-year price forecasts are really optimistic. They’ve set a median target of 930.5p per share. That’s up an impressive 25.84% from today.

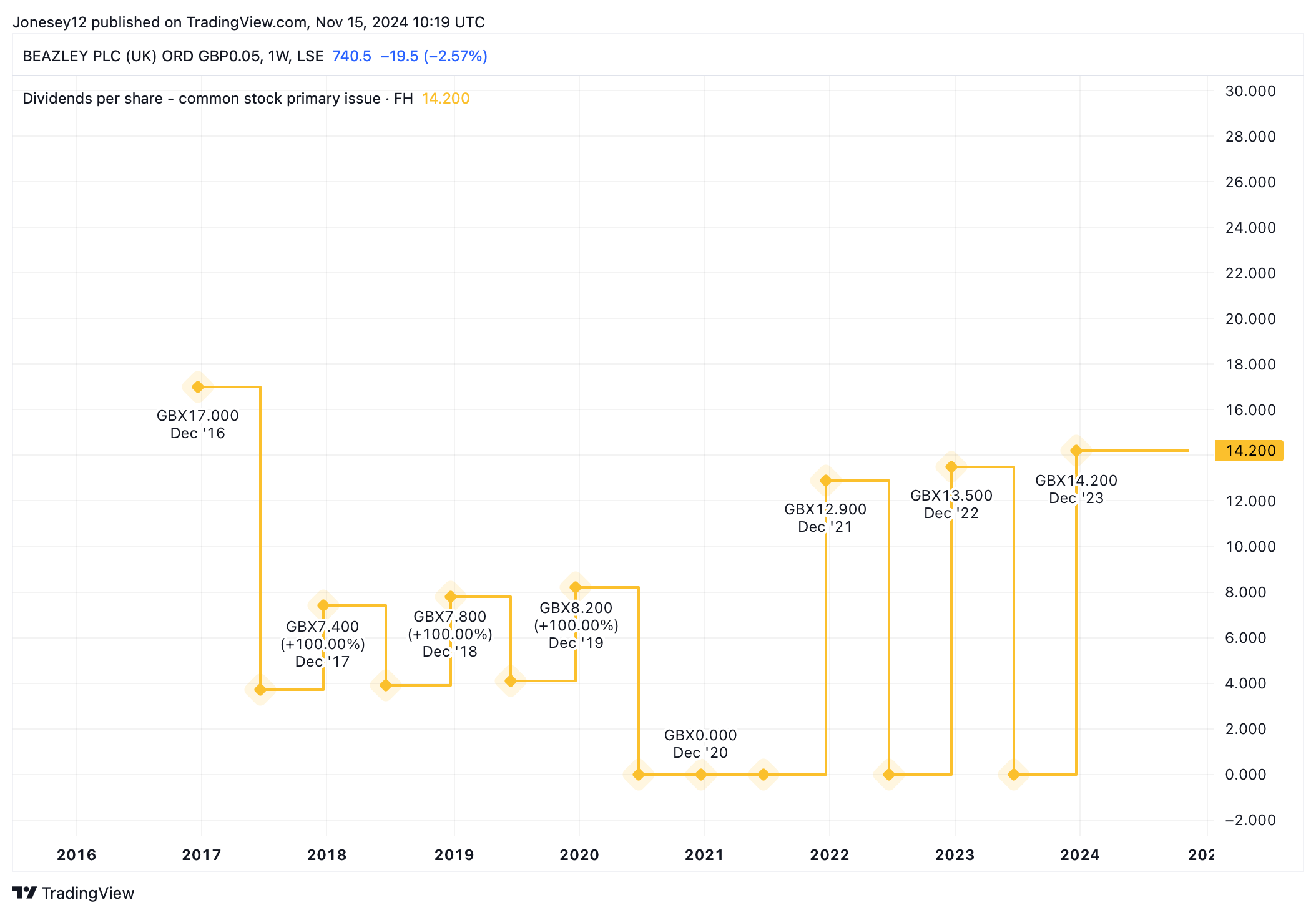

There’s a spot of income on offer, with a trailing yield of 1.92%. Post-pandemic growth has been steady. Let’s see what the chart says.

Chart by TradingView

Risk is Beazley’s business, and a surge in climate-related claims could knock it, of course. Perhaps I shouldn’t get too excited by its low valuation either. It’s been cheap for a while and it may just be that type of stock.

Last year, Beazley suffered an embarrassing blow when the Financial Times spotted an error in its annual report. Let’s hope it’s tightened up procedures since.

Today I’m fully invested, otherwise I’d buy Beazley. I’m keeping it on my watchlist until I get some cash. It still looks like a hidden bargain to me.

This post was originally published on Motley Fool