Why might investors be willing to pay a fee of 1% or more to an active money manager, rather than keep all of their money in a low-cost index fund?

The answer was actually provided recently by a reader. Ideally, you pay an active manager to run a portfolio that outperforms a benchmark index without mirroring the weighting of stocks in that index. This is known as “alpha” in the investment management industry.

An example of a fund that has done this, while producing excellent returns for most periods, is the SouthernSun Small Cap Fund. It had a $352 million portfolio of 22 stocks as of Dec. 31.

SouthernSun Asset Management is based in Memphis, Tenn., and has about $1 billion in assets under management. The firm was founded by Michael W. Cook, who serves as CEO and co-manages the SouthernSun Small Cap Fund with his son, Phillip Cook.

In an interview, Phillip Cook explained how he and colleagues get to know the companies they invest in.

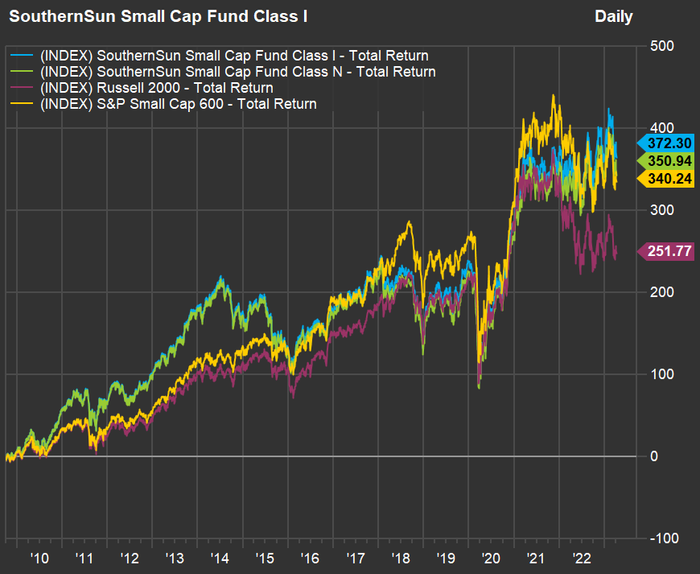

First, take a look at performance for the fund’s Class I

SSSIX,

and Class N

SSSFX,

shares. The class I shares ordinarily have a minimum initial investment of $100,000, however, through brokerage platforms, or through an adviser, you can probably buy shares in much smaller amounts. The Class N shares have a $2,000 minimum initial investment. The return figures below are net of annual expenses, which are 1.04% of assets under management for Class I and 1.30% for Class N. That is a large difference in expenses for a long-term investment, so the Class I shares are clearly the better investment.

The SouthernSun Small Cap Fund is benchmarked to the Russell 2000 Index

RUT,

It was established in October 2003 and the Class I shares became available Sept. 30, 2009.

Here’s how both of the Fund’s share classes have performed against its benchmark and the S&P Small Cap 600 Index

SML,

since Sept. 30, 2009, net of expenses. All returns in this article include reinvested dividends.

FactSet

Both share classes have outperformed both indexes over the long term, and you can see the cumulative effect of higher expenses for Class N. We included the S&P 600 Small Cap Index for comparison because this index takes a more selective approach than the Russell 2000, which includes hundreds of unprofitable companies. S&P Global’s criteria for initial inclusion in the S&P Small Cap 600 Index includes positive earnings for the most recent quarter and for the sum of the most recent four quarters.

When asked why so many small-cap funds benchmark to the Russell 2000 instead of to the S&P Small Cap 600 Index, Cook said: “Most of our clients express preference for the Russell 2000, and the index goes back to the 70s, while SML goes to the 90s.”

More recent returns have reflected the fund’s outperformance during 2022, when rising interest rates helped push the Russell 2000 down 20%:

FactSet

Here are average annual returns for several periods:

| Fund or Index | Average return – 3 Years | Average return – 5 Years | Average return – 10 years | Average return – 15 years |

| SouthernSun Small Cap Fund – Class I | 25.3% | 8.7% | 7.7% | N/A |

| SouthernSun Small Cap Fund – Class N | 25.0% | 8.4% | 7.4% | 9.5% |

| Russell 2000 | 13.8% | 4.2% | 7.9% | 7.8% |

| S&P Small Cap 600 | 17.8% | 5.7% | 9.8% | 9.4% |

| Source: FactSet | ||||

The SouthernSun Small Cap Fund’s active share, relative to the Russell 2000, was 98.8% as of Dec. 31. A fund’s active share is a measure of how differentiated it is from its benchmark. The higher it is, the more differentiated it is.

This isn’t to say that having a low active share is necessarily a bad thing, if a fund is performing well. But Cook made the case for (good) active management: “You need managers that think and behave differently and generate idiosyncratic returns. An active manager needs to supplement the index, rather than look like it. Most managers look like the index, and you are paying it.”

When asked about the fund’s underperformance, relative to the indexes, for the 10-year period, Cook said this reflected the fund’s “outsized weighting in industrials,” which took a hit in the wake of the oil price collapse in 2014. Then in 2015 there was “the first industrial recession, without an overall recession, in 40 years,” which hurt the fund’s performance, he said.

Getting to know the companies

A portfolio of 22 companies is concentrated. Morningstar rates the SouthernSun Small Cap Fund four stars (out of five) in its “small blend” fund category. According to Morningstar, the fund’s annual turnover of its portfolio is 37%. To put this number into perspective, Cook said annual turnover for a typical actively managed small-cap fund is “closer to 200%” on average.

Cook said that he and colleagues will typically identify companies that are important and stable suppliers in various industries. One way to find those: The SouthernSun team attends various trade shows.

Before considering a company for investment, Cook said he and colleagues will call and ask to meet with management and “build our own model” as part of a decision making process. He said his firm will typically hold a small-cap stock investment for seven to 10 years, but that they have held several for even longer periods.

Here are his comments on three of the fund’s holdings:

Murphy USA Inc.

MUSA,

is the “downstream” business that was separated from Murphy Oil Corp.

MUR,

in 2013. Murphy USA operates 1,712 retail stores in 27 states (as of Dec. 31) that are mostly gas stations combined with convenience stores close to Walmart

WMT,

stores.

Cook said he had recently met with Murphy USA’s senior management, maintaining a long-term relationship because SouthenSun has been a long-term shareholder.

“Companies will potentially change they way they think about capital allocation because of the conversations we have with them. We talk with the boards of directors. Companies are not as willing to allow this access for shorter-term investors,” he said.

Cook pointed to an advantage for Murphy USA, which he said owns about 80% of the land their stores are on. He said that in general, competitors lease their locations, which means they face higher expenses as rents rise.

When asked about the long-term viability of Murphy USA, in light of the expected adoption of electric vehicles, Cook said “double digit cash flow growth is still likely” for the company for many years, in part because much of their customer base is in states such as Texas, Florida and Tennessee that may not be so quick to make the switch to EVs.

“My experience is the charging stations are empty,” in Walmart parking lots, while the Murphy gas stations are full of customers. So he doesn’t expect Murphy USA to change its strategy to invest in charging facilities.

Ingevity Corp.

NGVT,

was spun out of WestRock Co. in 2016, with WestRock being a corporate successor to MeadWestvaco Corp.

“This is a paper and package company that spun out a specialty chemicals company. That was the reason we became interested,” Cook said. The processing of wood to create paper gives off byproducts with various other uses. According to Cook, Ingevity has “a dominant market share in activated carbon,” which is used to capture fuel emissions and lower pollution.

This means using a byproduct that is produced naturally, but has no other use, to capture emissions, and Ingevity makes the entire system, including the filters. “All of their products are byproducts of the pulp and paper process,” Cook said.

Companies producing parts for vehicles with internal combustion engines have an obvious need for this technology, and Cook estimates Ingevity serves about 90% of that market.

Ingevity has other business lines making use of wood pulp byproducts, including various road pavement ingredients, adhesives, inks, bioplastics, medical devices and additives to improve efficiency and stabilize emulsions of oil wells.

This is the type of company that fits in with one of the core questions Cook and his colleagues ask when seeking out new investments. “Who in the value chain is critical and fits out investment profile?,” he asked.

Then he gave another example: MGP Ingredients Inc.

MGPI,

which makes distilled spirits and food ingredients.

According to Cook, most companies making craft bourbon or other spirits actually don’t distill their own alcohol — they add the ingredients for their finished products, and MGP is the “majority” supplier of distilled spirits to these producers.

Top holdings

The SouthernSun Small Cap Fund publishes a full list of its holdings 45 days after the end of each quarter. Here are the fund’s top 10 holdings as of Dec. 31:

| Company | Ticker | Industry | % of portfolio | Total return – 3 years | Total return – 5 years |

| Darling Ingredients Inc. |

DAR, |

Feed, food and fuel ingredients | 7.1% | 184% | 242% |

| Dycom Industries Inc. |

DY, |

Engineering and construction | 6.0% | 203% | -14% |

| Timken Co. |

TKR, |

Metal fabrication | 6.0% | 128% | 82% |

| Stepan Co. |

SCL, |

Chemicals | 5.7% | 9% | 26% |

| Enerpac Tool Group Corp. Class A |

EPAC, |

Industrial machinery | 5.6% | 41% | 5% |

| Univar Solutions Inc. |

UNVR, |

Wholesale distributors | 5.2% | 168% | 24% |

| Crane Holdings Co. |

CR, |

Industrial machinery | 5.1% | N/A | N/A |

| Ingevity Corp. |

NGVT, |

Chemicals | 5.0% | 67% | -6% |

| Murphy USA Inc. |

MUSA, |

Specialty stores | 4.9% | 146% | 277% |

| MGP Ingredients Inc. |

MGPI, |

Agricultural commodities/milling | 4.9% | 182% | 19% |

| Sources: SouthernSun, FactSet | |||||

As of Dec. 31, the fund’s seventh largest holding was Crane Holding Co. This company was split last week into Crane Co.

CR,

which is made up of old company’s Aerospace & Electronics, Process Flow Technologies and Engineered Materials segments, while Crane NXT Co.

CXT,

operates the old company’s Payment & Merchandising Technologies segment.

Don’t miss: These 7 tables show just how bad this ‘crisis quarter’ could be for earnings of the 20 largest banks

This post was originally published on Market Watch