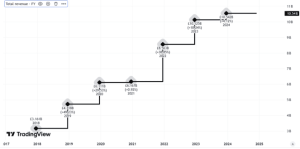

If someone offered to sell me something for 10 or 15 times the price I could have paid for it just a few years ago, I may feel at risk of being seen off. But that is the sort of return seen on Rolls-Royce (LSE: RR) shares in recent years. Having been under 40p at its 2020 low, the Rolls-Royce share price this week hovered close to the £6 mark.

But while that may be welcome news for long-term shareholders, what might it mean for an investor such as myself, hunting for value in today’s market?

Potentially further to run

In fact, I think the Rolls-Royce share price could potentially go even higher from here. For starters, its price-to-earnings (P/E) ratio of 21 while not exactly cheap does not look outrageous to me.

Other FTSE 100 firms have a higher P/E ratio. Fellow engineer Spirax, for example, trades on a P/E ratio of 28.

Rolls’ P/E ratio is based on past earnings. But its prospective earnings may be stronger – potentially much stronger. It is still in the process of undergoing a medium-term transformation programme. Demand for civil aviation engine sales and servicing is high.

Many Western governments are ramping up defence spending. Meanwhile, Rolls’ nuclear business may have large sales potential, thanks to its line of small modular reactors.

I’m hesitant – and here’s why

Still, although I see arguments as to why the Rolls-Royce share price could keep on moving up, I also have some reservations. To start with, the transformation programme remains a work in progress. Rolls is a large, slow-moving and historically unpredictable business in terms of performance. Whether that can change permanently and by how much remains to be seen.

If cost-cutting goes too far, there is a risk of reputational damage. Airline customers pay a premium for Rolls’ engines because they want total peace of mind that their planes have top notch engineering underpinning every flight.

The nuclear business could do very well, but people have been saying that about different nuclear businesses for decades already – with very mixed results. I feel this part of Rolls’ operations still needs to prove it can add significant long-term value for the company.

Meanwhile, in the core civil aviation engine business, Rolls only has so much under its control. Historically, one of the biggest challenges has been unforeseen external demand shocks for the airline industry, from terrorist attacks to volcanic clouds and the pandemic. Indeed, that explains why the Rolls-Royce share price was in pennies in 2020. The company was on its knees.

I see a risk that such events will happen again at some point in future – and there is little or nothing that Rolls can do about it. I reckon the current share price does not offer me a margin of safety considering that risk. So although I reckon the share may move higher still from here, I will not be along for the ride as I have no plans to invest.

This post was originally published on Motley Fool