Raspberry Pi Holdings (LSE: RPI) in the FTSE 250 index is causing a bit of excitement.

Maybe the home-grown technology stock’s about to offer British investors the chance to participate in eye-popping multi-year investment returns. You know, just like our American cousins enjoy from their many mega-sized technology companies.

The signs are encouraging with this one. Although the business has only been listed since June, it’s far from being a profitless start-up.

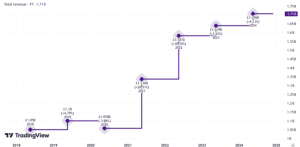

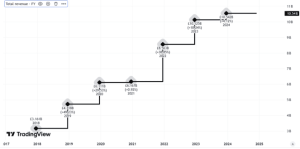

Fast-growing financials

The business has been building its mini-computers since 2012. Now it’s well-funded with a strong balance sheet. Additionally, it’s selling products like mad, is profitable, and has been throwing out the kind of earnings growth figures even a US tech company would be proud of.

There are some influential believers out there too. Technology giant ARM Holdings holds a slug of the shares, and ARM processors are built in to Raspberry Pi products. Meanwhile, investment bank Peel Hunt is acting as joint broker for the British company and has been super-enthusiastic about the business.

Raspberry Pi is one of the “best-known” tech brands born in the UK, the bank said. The company has already sold more than 60m of its “innovative” single-board computers (SBCs).

The enterprise creates semiconductor intellectual property (IP), optimised software, and engineers its supply chain to boost the unit economics of its SBCs. Okay, but the commercial bit is that SBCs help people to use cost-efficient computers in industrial and other settings — known as Edge computing.

The idea is that companies, organisations and individuals can better take advantage of the artificial intelligence and machine learning revolution. SBCs can also help to make the much talked about internet of things (IoT) happen. To me, that sure sounds like it’s giving people an edge in the game!

Raspberry Pi’s been selling these things like hot cakes. Around 72% of sales have gone to industrial and embedded applications around the world via a network of approved resellers and licensees.

A future tech giant in the making?

Peel Hunt argues the company is serving a large and growing market and tips it as having the potential to become a tech powerhouse just like some of its big US cousins. If that happens, it’s possible the stock may transform my portfolio over the next decade.

But there are risks, as always. One is the current valuation. With the share price in the ballpark of 500p, the forward-looking price-to-earnings (P/E) for 2025 is around 45. That’s pricey.

On top of that, earnings have been volatile and forecast to come in down a bit for 2024 with a rebound next year. So that’s a bit unsettling.

Another risk is that well-minted competition may swoop in and eat into Raspberry Pi’s market share.

Nevertheless, to me, this looks like an exciting long-term growth proposition. So I’ve decided to embrace the risks of holding the stock with a 10-year time frame in mind.

This post was originally published on Motley Fool