Hidden gems are my favourite kind of investment. The hottest shares of the moment are almost always overvalued. However, I can often find a fast-paced growth stock with an attractive valuation for my portfolio if I look through smaller companies. I’m now wondering whether Alpha Group International (LSE:ALPH) is one such under-the-radar bargain.

High growth at a low price

Alpha Group, a London-based financial services company, specialises in foreign exchange risk management and global payment solutions for corporations.

Over the past three years, on average, it has delivered exceptional revenue growth of nearly 31% annually and earnings before interest, taxes, depreciation, and amortization (EBITDA) growth of 81.5% annually.

Furthermore, its price-to-earnings (P/E) ratio has contracted from 35.5, as a historical median, to 12 today. In other words, this is both a value and a growth opportunity.

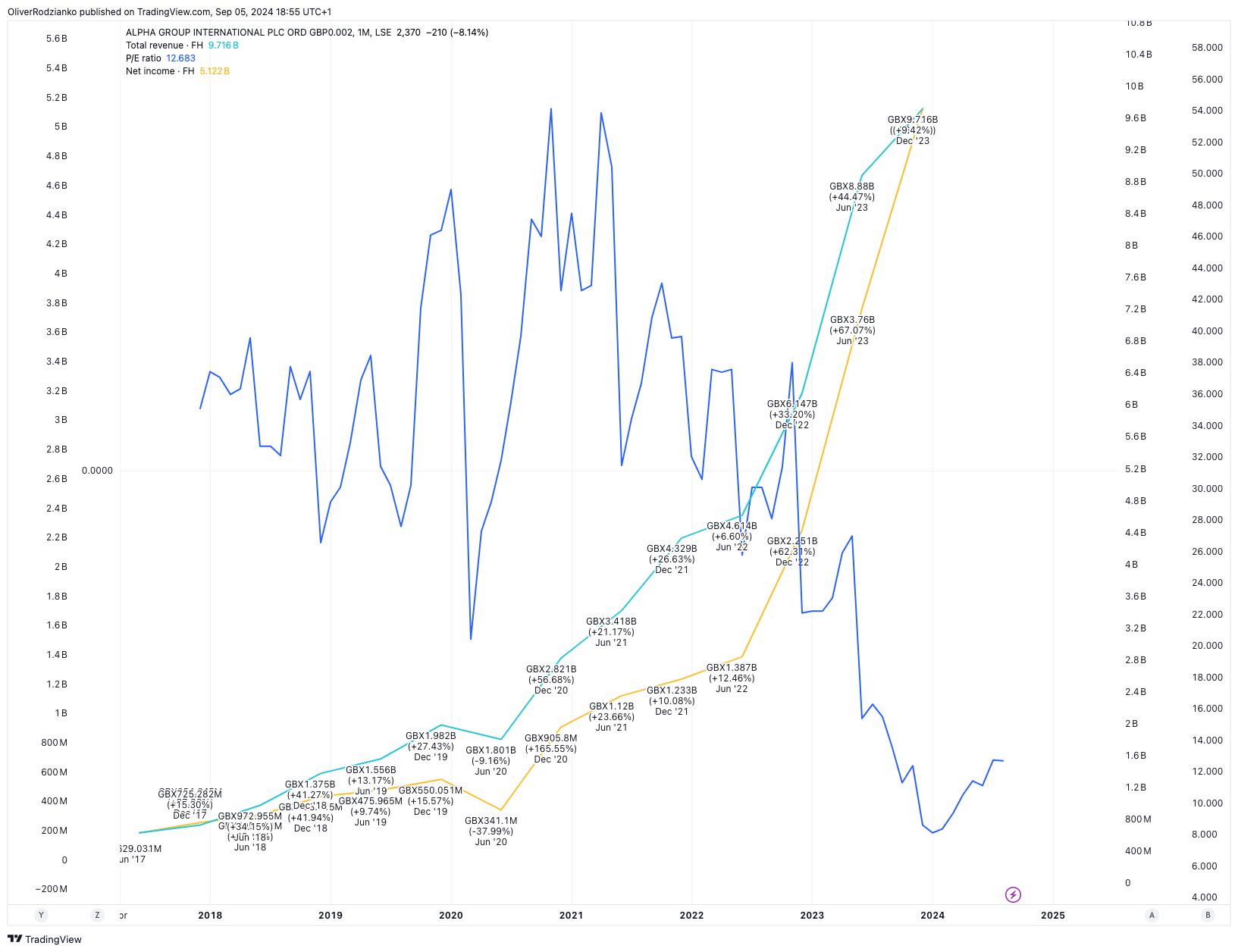

Created at TradingView

The above graph shows a visual representation of the opportunity here. Increasing growth rates and a falling P/E ratio often mean the market is undervaluing a company.

Its price growth is stellar

Furthermore, while its P/E ratio has been contracting, the overall price of the shares has been increasing quickly. Over the past five years, the investment has grown by over 210% in value. In addition, it’s also increased by nearly 40% year to date.

Furthermore, analysts don’t expect the growth to stop now. Of the two bankers covering the company, the average 12-month price target indicates a 24.9% growth potential.

However, there’s no guarantee that this target will be realised. After all, based on analyst estimates, its revenue growth over the next three years is likely to be slower than historically, even though its earnings per share growth rates are likely to see a substantial increase.

The benefits of diversification

I’m a big believer in not tying up too much of my money in any one investment. Instead, healthy diversification is what keeps me protected from unexpected incidents in one business or another.

For example, Alpha Group itself relies on only a small number of key clients for most of its revenue. Therefore, putting too much of my savings into its shares means I’m vulnerable to changes in these agreements.

In contrast, a company like Apple has global operations, with hundreds of billions of pounds worth of annual revenue. Therefore, investing in a big tech company like it, provided the valuation is fair, is a lot less risky.

I consider it among the best

It’s not often I find an investment opportunity that I consider world-class. However, I think this is one of them.

Price growth of 25% in 12 months would indeed be exceptional. After all, the average annual stock market return in the US is around 10%. Based on my analysis, I think the shares can perform to meet or even beat analysts’ expectations.

This investment is at the top of my watchlist, and I’m going to buy it when I next have some spare cash. It’s one I’ll have to monitor regularly because it’s smaller and more vulnerable to risk. But with the right watchful eye, I think these shares are going to be critical in my ambition to achieve 15%+ total portfolio returns this financial year.

This post was originally published on Motley Fool