I’ve been hunting for a UK growth stock to buy recently. These tend to be a bit cheaper than their US counterparts and I reckon they could get a decent boost once the Bank of England starts cutting rates.

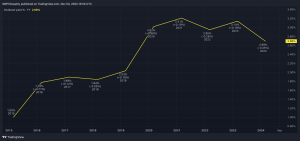

Today (24 July), Oxford Nanopore Technologies (LSE: ONT) posted a half-year trading update. The stock responded positively, rising 4% to 125p. This takes its gains to an incredible 43% in just the past month!

Zooming further out though, the share price is still down 79% since the innovative firm went public in 2021. So, is this the UK stock I’ve been looking for?

What it does

Firstly, a quick explanation about the name. The ‘Oxford’ part relates to it being spun out of Oxford University in 2005. The ‘Nanopore’ bit refers to the company’s novel technology that reads DNA using tiny holes, or nanopores, embedded in a membrane.

The firm’s devices are used in over 100 countries to understand the biology of humans, plants, animals, bacteria, viruses, and diseases like cancer. Its pocket-sized MinION device weighs under 100g and plugs into a laptop via a USB cable. This allows real-time sequencing anywhere, even in remote locations like jungles.

In 2023, over 2,800 research studies using Oxford Nanopore’s technology were published, reflecting its increasing importance across multiple fields.

Why has the stock struggled?

So, if the company’s tech is so cutting-edge, why is the share price down 79% in less than three years? Well, the firm lost £154.5m last year, wider than £91m the year before. That was almost the same as it reported in annual revenue (£170m). Yikes!

It isn’t expecting to break even on an adjusted EBITDA basis until the end of 2027. By that point, it reckons that its life science research tools (LSRT) gross margin will be 62%, up from 53.3% last year. Forecasts I’m looking at suggest revenue of £385m by 2027. So plenty of growth is expected here.

Unfortunately though, due to higher interest rates, the market is struggling to find the patience to wait that long for potential profits. Most loss-making growth stocks have plunged over the past two years.

Of course, investor sentiment is out of the company’s control. All it can do is continue to grow, innovate and stick to its medium-term schedule. And in H1, we saw evidence of progress.

Guidance reaffirmed

For the six months ended 30 June, it expects to report revenue of approximately £84m, broadly flat year on year at constant currency. However, underlying LSRT revenue (which strips out prior revenue from Covid and a large genome project), grew by 12.4%.

Growth was strongest across its PromethION franchise (benchtop sequencers), while the launch of multiple new products is expected to drive near and medium-term growth.

For the full year, it expects underlying revenue growth of 20%-30%, despite a challenging macroeconomic backdrop. And it expects gross margin to be approximately 57%, while its medium-term (2027) guidance remains intact.

My decision

The stock has a price-to-sales (P/S) ratio of 6.2. That’s more than US rivals Illumina (4.1) and Pacific Biosciences of California (2.4).

Oxford Nanopore is growing faster than those, but the stock still looks pricey. So, while I love this innovative British tech firm, I’m going to continue watching its progress from the sidelines (for now).

This post was originally published on Motley Fool