Ask the average investor to say which FTSE 100 civil and defence engineer they thought was the best share to buy and most would land on Rolls-Royce or BAE Systems.

So let’s hear it for Melrose Industries (LSE: MRO), the forgotten stock of the aerospace and defence sector. I feel it may offer a better opportunity than both Rolls and BAE, both of which I own but look fully-priced right now.

Shares tend to slip people’s minds when they don’t go anywhere for a while. The Melrose share price has been easy to ignore. It’s down 25.11% over five years, and 0.98% over the last 12 months.

Yet this can make them attractive to contrarian investors, who know the early stages of the recovery are most rewarding.

Can this FTSE 100 stock keep climbing?

That’s the case with Melrose, whose shares have suddenly jumped 16.45% in the last month. What’s going on?

The bounce came after it published figures on the 19 joint ventures it holds with engine manufacturers on 28 October. Under these Risk and Revenue Sharing Partnerships (RRSPs), Melrose shares in the ongoing revenues of the engines it supplies parts for.

The contracts can run for 50 years, and provide a steady stream of cash from maintenance and parts replacements. Melrose anticipates £22bn of RRSP cash flows over the next 25 years. My back-of-a-fag-packet maths suggests this is worth £880m a year. This could be worth investors who buy shares with a long-term view (as all of us at The Fool do) investigating.

Melrose got a further lift on 5 October when Citi named it a “high-conviction” Buy, predicting free cash flow would range from £450m-£550m in 2027/28, beating consensus of £320m-£420m.

Civil aerospace is a bumpy sector, as we saw in the pandemic. The Melrose share price crashed from 570p to 175p during lockdown. It’s struggled since, posting pre-tax losses in the four years to 2023.

Underlying revenues climbed 13% to £3.35bn in 2023 and rose another 6.7% in the first half of this year to £1.7bn. Underlying operating profit hit £247m, as rising aftermarket activity boosted its Engines division. It’s whittled down net debt to £976m. Supply chain issues are proving a drag though.

Melrose Industries ain’t half a mixed bag

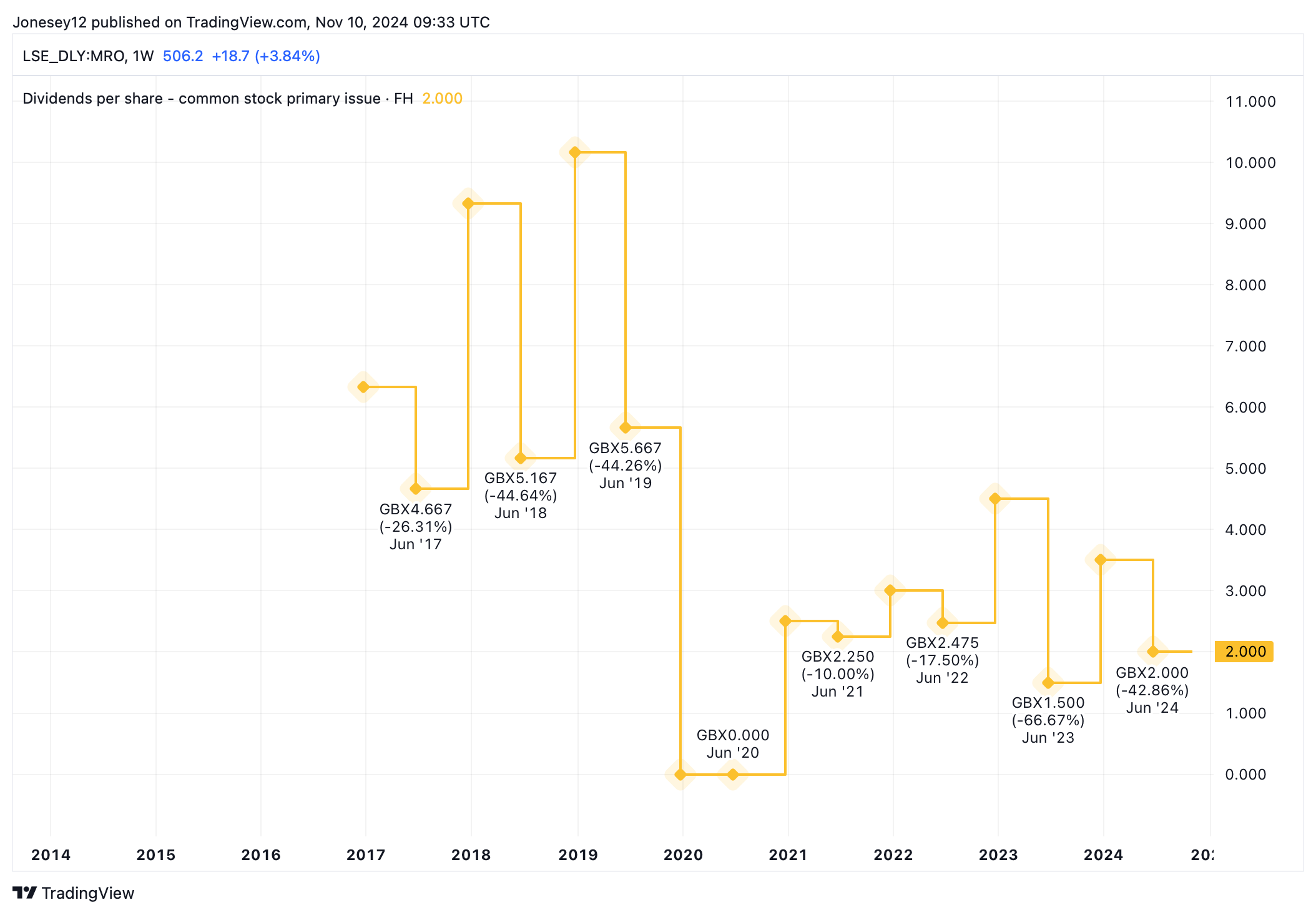

The Melrose dividend took a beating in the pandemic but is steadily recovering. The trailing yield is a lowly 0.99%. Let’s see what the chart says.

Chart by TradingView

Melrose has one thing in its favour. It looks cheap with a price-to-book (P/B) ratio of 1.7 on 30 September. That’s way below the average P/B of 7.6 for the aerospace and defence sector. I imagine it’s probably a bit pricier since the recent share price hop.

However, a price-to-sales ratio of 1.8 is only a tad behind the sector average of 1.9. Its price-to-earnings ratio of 26.45 doesn’t grab me either.

The 10 analysts offering one-year share price targets setting a median figure of 593.6p. That’s up 17.25% today. Promising.

Yet I’m always wary of buying a stock after it’s suddenly jumped, in case I make an instant loss as others take profits. The long-term outlook is positive, but Melrose still has work to do in the short run. I’m tempted, but there are other FTSE 100 shares I’d rather buy today.

This post was originally published on Motley Fool