At the start of 2024, I had a positive view on FTSE 250 pub chain JD Wetherspoon (LSE:JDW). But with the share price down 25%, it’s fair to say that hasn’t worked out… yet.

I’m not above admitting when I’ve got something wrong – that happens to even the best investors. But I think the business is actually in a pretty good position and I’m still looking to buy the stock in 2025.

2024 in review

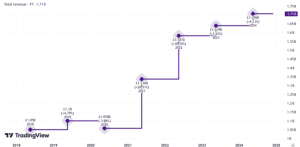

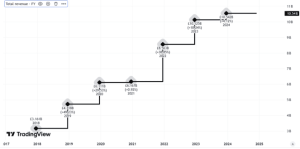

JD Wetherspoon’s share price might have fallen, but the underlying business has done well in 2024. In its annual report in October, the company announced sales up 5.7% and earnings per share up 77%.

The firm also reinstated its dividend for the first time since 2019 and returned £40m to investors via share buybacks. Overall, I thought this was a more than respectable result.

Despite this, the stock fell consistently throughout the year. While I’m not entirely sure why, I suspect the prospect of higher costs had a lot to with it, and these fears were realised in November.

The Budget increased the minimum wage and boosted National Insurance contributions for employers. This looks set to cost JD Wetherspoon around £60m per year, which is the firm’s entire net income.

Price increases

Wetherspoon’s has been investing consistently to keep its prices to customers low. To this end, it has increased the size of its pubs and bought freehold rights to reduce lease liabilities.

Nonetheless, Chairman Tim Martin all but stated in response to Budget that prices will have to go up. And that inevitably creates a risk that the company’s price-conscious customers will disappear.

The Wetherspoon’s business model relies on volume to make money. That’s part of the reason it works so hard to keep prices low. This means losing customers could be a huge blow for the business.

My guess is this is why the share price has been falling throughout 2024. But I think the market is making a mistake and I’m looking to take advantage of it.

Pricing power

I think JD Wetherspoon is in a better position than investors realise. As a result of its investments and its relentless focus on customer value, its prices are a lot cheaper than those of its competitors.

By my estimates, a 5% price increase across the board could more than offset the additional costs coming from the Budget. And the company would still offer customers better value than its rivals.

Importantly, other pubs are also going to be under similar pressure. And with higher prices to start with, I suspect the chances of them losing customers if they try to pass those costs on is much greater.

I therefore think the market is overestimating the risk of the Budget’s higher costs for JD Wetherspoon. These are unwelcome, but the firm is in a better place to deal with them than its rivals.

I’m buying

To make money from shares, it’s important to have a differing view to the rest of the market. In my case, that’s JD Wetherspoon – I think investors are underestimating the strength of the underlying business.

I don’t know when the market will come round to my view, but I intend to keep buying JD Wetherspoon shares until it does. Or until something convinces me that I’m actually wrong about the company.

This post was originally published on Motley Fool