In general, I share Warren Buffett’s aversion to airline stocks. But I have one exception to this rule and with the Ryanair (NASDAQ:RYAA.Y) share price at its current level, I’m looking to buy.

Even with the industry as a whole set for yet another downturn, I think there’s an opportunity here. The near future looks challenging, but I’m much more positive about the long-term outlook.

Weak demand

Air travel is a cyclical industry. When household budgets come under pressure, consumers often find themselves looking to be more cautious with their spending.

This, according to Ryanair, is what’s happening at the moment. And the effect is the company’s profits for the second quarter of 2024 fell by 46% compared to the previous year.

In response, the business is looking to reduce its fares for the summer. That’s likely to mean lower profit margins, but there’s a positive that investors should take note of.

Weak travel demand isn’t a good thing for Ryanair, but it’s much worse for other airlines. As a result, I think the company might well emerge from this year in a stronger competitive position.

Low costs

Ryanair has two major advantages that equip it better than other airlines to deal with cyclical downturns. The first is that it has lower costs than its rivals.

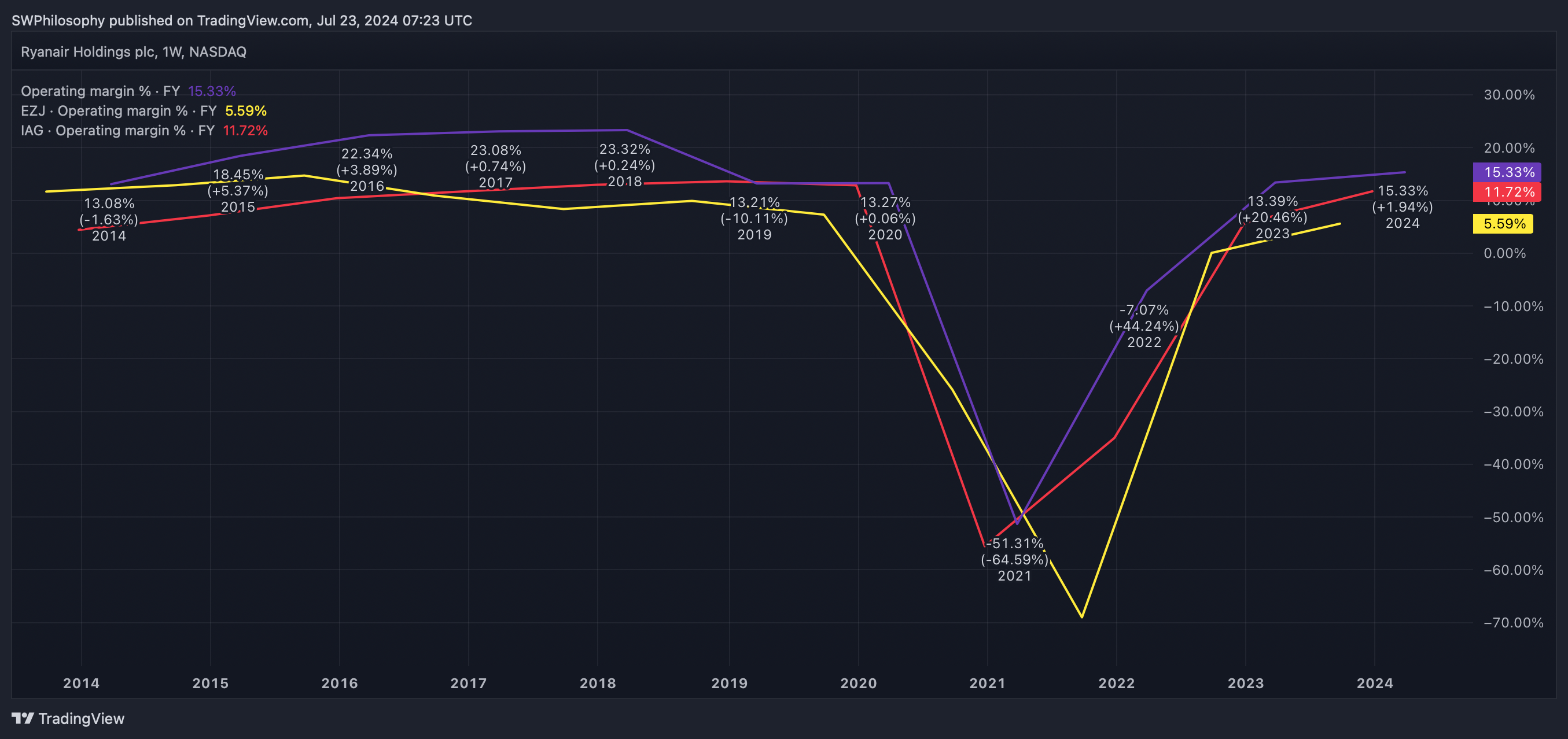

Ryanair vs. easyJet vs. International Consolidated Airlines Group Operating Margin 2014-24

Created at TradingView

Despite having the lowest fares, Ryanair maintains wider operating margins than easyJet or International Consolidated Airline Group. This is because it has the lowest costs in the industry.

Avoiding expensive airports, owning aircraft instead of leasing them, and minimising downtime all support this. And it puts the company in a stronger position than its rivals when demand is weak.

Ryanair cutting prices should force other airlines to do the same. But without the same operating margins, they could find themselves forced into losses, rather than just weaker profitability.

Balance sheet

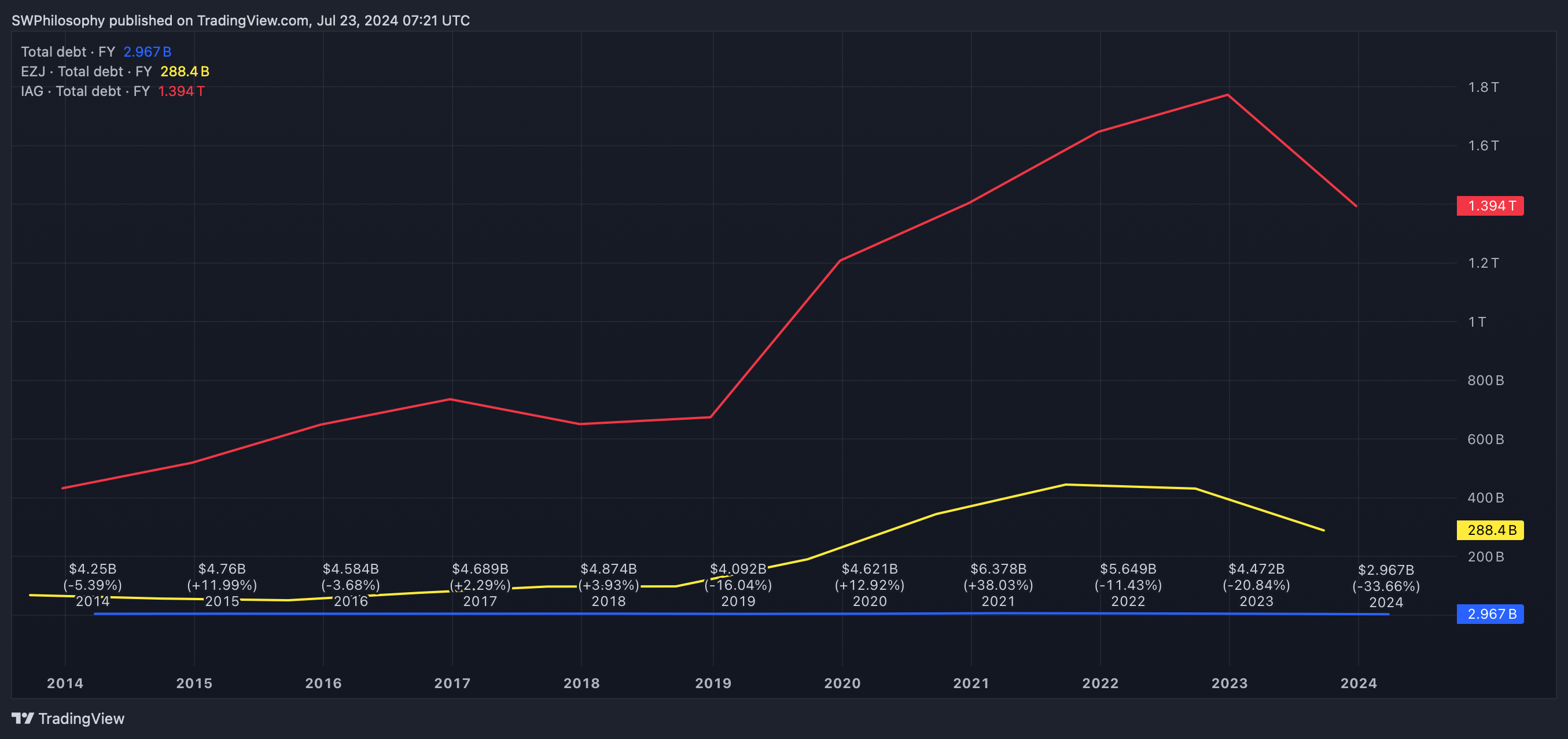

This situation is exacerbated by looking at Ryanair’s financial position relative to its rivals. Unlike other airlines, Ryanair’s balance sheet has recovered well from the Covid-19 pandemic.

Ryanair vs. easyJet vs. International Consolidated Airlines Group Total Debt 2014-24

Created at TradingView

Both easyJet and IAG are still spending a lot on interest payments on debt acquired during 2019 and 2020. With Ryanair, the company’s interest expense is roughly in line with its long-term average.

Not having to worry about interest payments to the same extent also gives the company more scope to lower prices. And there’s another advantage too.

Airlines typically cut back on new aircraft in tough times. But Ryanair’s ability to buy when others can’t allows it to negotiate better prices with Boeing, creating another long-term advantage.

Airline investing

The main risks with Ryanair are events like Covid-19, Icelandic ash clouds, and cyclical downturns. The company can’t do much about these and they can cause profits to fall sharply.

Nonetheless, Ryanair’s business model has allowed it to emerge from each crisis in a stronger position than before. That’s why the stock has climbed 52% over the last five years and also why I’m looking to buy it at today’s prices.

This post was originally published on Motley Fool