Lloyds is one of the most popular income stocks on the London Stock Exchange. The bank plays a critical role within the UK economy as a business and mortgage lender generating a steady stream of cash flow.

It pays a healthy dividend and as such, shareholders have enjoyed a fairly consistent stream of payouts over the years.

Yet, despite its popularity, Lloyds hasn’t actually been a particularly good investment overall, lagging the FTSE 100 for more than a decade. That’s why when hunting for passive income opportunities it’s not a stock I’m tempted by, even with a 5% yield.

Instead, Howden Joinery (LSE:HWDN) looks like a far better buy, in my eyes.

4,100% dividend growth

As a designer and supplier of fitted kitchens, Howden’s not the most exotic enterprise on the stock market. But the same can’t be said about its performance. Even with all the disruptions from the pandemic, supply chains and, more recently, inflation, the firm continues to drive strong performance. And while growth has slowed over the last year, an improving economic landscape’s steadily helping to ramp sales and earnings back up.

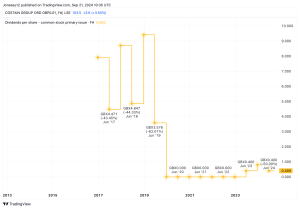

The firm has once again demonstrated its ability to navigate unfavourable economic environments without seeing its bottom line plummet like so many other businesses. And the prudent decision-making from management is how the company’s grown its dividend from 0.5p a share in 2011 to 21p in 2023 – a 4,100% increase!

To put this into perspective, investors who bought and held shares 13 years’ ago are now earning an annualised yield just shy of 20%. That’s more than double the stock market typically generates, just from dividends.

Looking to the future

Moving forward, Howden remains an intriguing opportunity for long-term investors, in my opinion. While another quadruple-digit expansion to dividends isn’t likely anytime soon, there still remains exciting prospects for further yield expansion.

Looking at the business, the avenues for growth are still bountiful. Management’s on track to expand its depot network to 1,000 within the UK alone and is simultaneously reaching out to international markets as well. At the same time, the group has just begun testing out the fitted bedrooms market, broadening its total addressable market.

Of course, no enterprise is without its risks. We’ve already seen the impact that an unfavourable economic environment can have on this business, particularly its profit margins. Don’t forget the majority of its sales stem from home renovation projects rather than new builds.

Therefore, should household budgets continue to be constrained, the return to historical growth in sales, earnings and dividends may end up being a protracted process. Nevertheless, the firm’s impressive track record makes it a risk worth taking, in my mind. That’s why I’ve already added this stock to my income portfolio.

This post was originally published on Motley Fool