The headlines of the story about Wednesday’s Federal Reserve policy meeting have already been written. The devil, as they say, will be in the details.

On the likely news, it is a “foregone conclusion” the Fed will announce Wednesday that a tapering of asset purchases will begin later this month, according to Michael Gapen, chief U.S. economist at Barclays.

Read: Fed seen announcing start of taper

The Fed has indicated the pace of reduction in its bond buying program is likely to be $15 billion per month. This means that the current pace of $120 billion in monthly asset purchases will end completely in the middle of next year.

Here’s a look at what else economists and investors will be watching for when the Fed concludes the two-day meeting on Wednesday. The Fed will release a statement at 2 p.m. Eastern and Fed Chairman Jerome Powell will hold a press conference at 2:30 p.m. Eastern.

Transitory inflation

A lot has been written about Powell’s view that inflation is “transitory,” which doesn’t mean it will quickly reverse. Instead, it means that within a reasonable timeline, inflation will revert to its 2% target,” says Tim Duy, chief U.S. economist at SGH Macro Advisers.

The Fed’s statement in September said that “inflation is elevated, largely reflecting transitory factors.” and economists are divided over whether it will be included in the statement released Wednesday.

Michelle Meyer, head of U.S. economics at BofA , thinks this key sentence will be edited so that it says “partly” reflecting transitory factors or a sentence is added about signs of more persistent inflation.

Jim O’Sullivan, chief U.S. macro strategist at TD Securities, thinks the Fed will stick with the “largely reflecting transitory factors” language. This will imply no rush for interest rate hikes, he said.

The underpinnings of the “transitory” prediction are staring to “lose its luster,” said said Steve Friedman, senior macroeconomist at MacKay Shields, in an email. Inflation is looking more broad based, with shelter costs and a broader range of goods and services now registering price increases, he said.

The Fed’s favorite inflation gauge, the personal consumption expenditure price index, rose at a 4.4% annual pace in October, the fastest pace in thirty years. In addition, wages had the largest quarterly increases since the early 1990s.

Rate hikes

Powell is likely to emphasize again that the decision to taper is independent from the decision to lift rates. But markets won’t pay much attention to those efforts, said Gapen of Barclays, in an note.

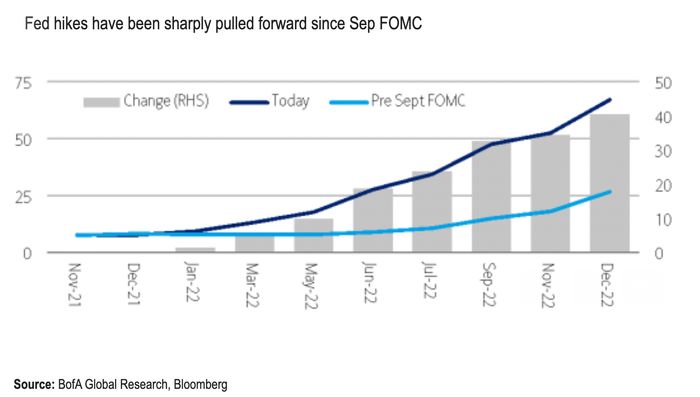

Markets continue to price in about two quarter-point rate hikes in 2022 and see the Fed transitioning quickly from ending asset purchases to raising short-term interest rates.

In September, the Fed was evenly split over whether to raise rates next near and many Fed officials have signaled they want to end tapering in case rate hikes are needed, he said.

Michael Gregory, deputy chief economist at BMO Capital Markets in Toronto said he expects “we’ll still come away with the impression that the chances of liftoff later next year have moved much higher than the 50-50 odds portrayed by last meeting’s dot-plot.”

Balance sheet

In 2016, some economists argued that the Fed should start to actually shrink its balance sheet before it raises interest rates. The central bank didn’t follow that approach but the argument is resurfacing again, said Mark Cabana, rates strategist at BofA Securities. Some Fed officials, including St. Louis Fed president James Bullard, have signaled a willingness for an early move to shrink the balance sheet, which has risen to $8.6 trillion from $4.4 trillion prior to the pandemic.

Cabana said his base case is that the Fed follows the approach of the last cycle in 2017-2019 and moves to reduce the balance sheet once its benchmark rate is above 1%, which he pencils in to happen in the fourth quarter of 2023.

But there are rising odds for an earlier move – in early 2023 – to shrink the balance sheet as it would be a more passive policy tightening that gives the labor market longer to heal. he said.

To shrink the balance sheet, the Fed doesn’t have to sell securities that it holds. It can just let them mature and not reinvest the proceeds.

Ethics concern

Powell is going to be asked about ethics concerns related to Fed officials trading for their personal accounts during the pandemic. Last month, the Fed announced new rules to restrict trading by top officials. Two regional Fed presidents left their positions after their trading behavior in 2020 was criticized. Some progressive Democrats have questioned some of Powell’s own investment decisions, as well as decisions by his No. 2, Vice Chairman Richard Clarida. “We expect the Fed Chair to take time to explain the new procedures and push back against the perceptions that Fed officials were engaged in a form of self-dealing,” Gapen said.

Second term for Powell

Powell’s term as Fed chair ends early next year and some economists believe that Powell’s hands are tied as long as President Joe Biden hasn’t acted to reappoint him.

“He cannot start to be Mr. Tough Guy [on inflation] as long as his reappointment is hanging in the balance,” said Robert Brusca, chief economist at FAO Economics. He added the Fed is under “kind of crazy pressure” from progressives. “I think that’s a really big complication for policy right now.”

At his last press conference in September, Powell demurred from making any statement on the matter. “I think the phrase goes – I have nothing for you on that today. Sorry, I’m just focused on my job,” he said.

The yield on the 10-year Treasury note

TMUBMUSD10Y,

has risen to over 1.5% from low readings below 1.2% in late August.

This post was originally published on Market Watch