Investors are generally sour when it comes to bank stocks, and the financial sector as a whole trades at a low valuation to expected earnings.

But the great expansion of U.S. household wealth points to an opportunity for long-term investors to ride a wave of stable and growing earnings for certain financial service companies. These companies are de-emphasizing riskier and lower-margin lending businesses and cyclical investment-banking activities, while focusing on growing more stable fee-generating business.

Macrae Sykes Macrae Sykes manages the Gabelli Financial Services Opportunities ETF

GABF,

Most exchange-traded ETFs are passively managed to track a broad index, such as the SPDR S&P 500 ETF Trust

SPY,

or a more focused index or sector, such as the Financial Select SPDR Fund

XLF,

which tracks the S&P 500 financial sector.

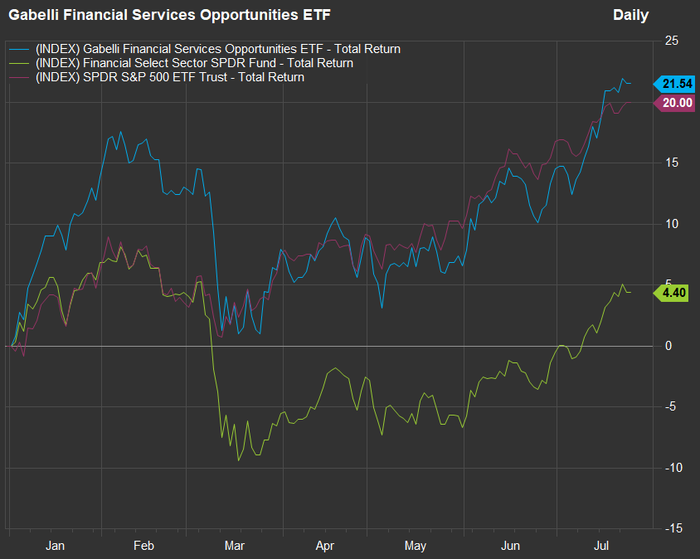

Here’s how the three ETFs have performed this year:

FactSet

All three show the pattern of recovery from March, especially XLF. But the Gabelli ETF has avoided heavy exposure to regional banks suffering deposit flight earlier this year, and a more general increase in funding costs as interest rates have continued to rise.

GABF is still a new fund. It was established in May 2022 and Gabelli has temporarily waived its management fee, which would ordinarily be an annualized 0.90% of assets under management. For now, the total expense ratio is only 0.04%. The fund only has $7.1 million in assets. While Morningstar won’t assign a rating to a fund until it is three years old, the firm ranked GABF as the top performer among 101 funds in its “U.S. Fund Financial” category year-to-date, ranking it fourth in the category for one year through July 25.

Coverage of financial companies will often center on credit — after all, nearly everyone will borrow money at some point. Borrowing is risky for everyone, and low credit quality was a driving factor in the 2008 financial crisis, but banks and other financial service companies have learned that other financial services are less risky and more profitable.

During an interview, Sykes described his strategy and cited projections prepared by Cerulli Associates that $84 trillion of household wealth would be transferred by people in the U.S. to heirs through 2045.

That type of transition of wealth to younger generations makes for continuing opportunities for financial advisers and wealth managers to attract new clients and grow assets under management, making for predictable and increasing revenue streams.

“We see a significant tailwind for investment advice and asset management services,” Sykes said. He named Morgan Stanley

MS,

as a beneficiary of the “wealth gathering trend.” An important part of its renewed focus on advisory services and asset management was its acquisition of E-Trade in 2020. Sykes also holds shares of Charles Schwab Corp.

SCHW,

in the GABF portfolio. Schwab made a similar acquisition of TD Ameritrade in 2020.

For financial innovation, Sykes named Blackstone Inc.

BX,

and Apollo Global Management Inc.

APO,

both of which “are broadening their product base to include retail investors.”

“So their share of managed assets will increase. That comes with favorable economics,” Sykes said.

Another holding of GABF that has been a strong performer is American Express Co.

AXP,

which always ranks near the top for bank holding companies by returns on assets and equity, because such a large portion of its revenue is derived from its charge business (through which customers pay their entire card balances to zero each month), which has lower risk than traditional credit-card lending.

American Express was the best earnings performer among all U.S. banks with at least $20 billion in assets, based on returns on average assets for 15 years through 2022.

GABF is a concentrated fund. It holds 39 stocks, and its top 10 holdings make up 50% of the portfolio. The largest holding is Berkshire Hathaway Inc.

BRK.B,

According to Sykes, the conglomerate’s core insurance business is better-positioned than it was two years ago, because premiums have been invested in bonds with much higher yields as the Federal Reserve has continued to tighten monetary policy to fight inflation. He also said Berkshire’s reinsurance business was benefitting from “a very hard market” for property insurance.

Longer term, Skyes echoed Berkshire CEO Warren Buffett’s theme of having confidence in the continued “prosperity of the U.S.”

Here are the largest 20 holdings of the Gabelli Financial Services Opportunities ETF, along with forward price-to-earnings valuations and projected two-year compound annual growth rates (CAGR) for earnings per share from 2023 through 2025, based on consensus estimates among analysts polled by FactSet. Valuations and projections for the full S&P 500 and the S&P 500 financial sector are at the bottom of the table:

| Company | Ticker | % of the Gabelli Financial Services Opportunities Fund | Forward P/E | Two-year estimated EPS CAGR through 2025 |

| Berkshire Hathaway Inc. Class B | BRK.B | 7.8% | 21.0 | 12.3% |

| FTAI Aviation Ltd. | FTAI | 7.2% | 21.8 | 52.9% |

| First Citizens BancShares Inc. Class A | FCNCA | 6.5% | 8.5 | 4.9% |

| Blackstone Inc. | BX | 4.7% | 20.1 | 27.1% |

| Blue Owl Capital Inc. Class A | OWL | 4.3% | 16.8 | 24.1% |

| Interactive Brokers Group Inc. Class A | IBKR | 4.2% | 14.0 | 4.0% |

| American Express Co. | AXP | 4.1% | 14.2 | 12.5% |

| Sculptor Capital Management Inc. Class A | SCU | 3.8% | 5.1 | N/A |

| JPMorgan Chase & Co. | JPM | 3.7% | 10.4 | -0.9% |

| Charles Schwab Corp. | SCHW | 3.6% | 17.7 | 28.2% |

| S&P Global Inc. | SPGI | 3.5% | 31.2 | 14.5% |

| Apollo Global Management Inc. | APO | 3.5% | 11.1 | 17.6% |

| Moody’s Corp. | MCO | 3.4% | 33.3 | 14.5% |

| Fiserv Inc. | FI | 3.2% | 15.8 | 14.4% |

| Silvercrest Asset Management Group Inc. Class A | SAMG | 2.8% | 12.4 | 14.9% |

| Affiliated Managers Group Inc. | AMG | 2.8% | 7.0 | 16.6% |

| FactSet Research Systems Inc. | FDS | 2.7% | 26.6 | 10.8% |

| Paysafe Ltd. | PSFE | 2.7% | 6.7 | 44.2% |

| Cohen & Steers Inc. | CNS | 2.6% | 21.1 | N/A |

| Morgan Stanley | MS | 2.3% | 14.0 | 19.4% |

| S&P 500 | spx | 19.7 | 12.4% | |

| S&P 500 Financials | 13.9 | 11.3% | ||

| Source: FactSet | ||||

Click on the tickers for more about each company, fund or index.

Notes about the data:

-

Sculptor Capital Management Inc.

SCU,

-0.09%

said on Monday that it had agreed to be acquired by Rithm Capital Corp.

RITM,

+0.84% . - Looking at the forward price-to-earnings ratios at the bottom of the table for the S&P 500 and for the benchmark index’s financial sector, the financials trade at a valuation of 71% of the index’s P/E. That is a typical discount for the group.

- Morgan Stanley trades at a forward P/E of only 14 — a slight premium to the financial sector and a large discount to the full S&P 500, despite being expected to grow earnings much more quickly than either.

This post was originally published on Market Watch