Amazon (AMZN) is a leading e-commerce business, with $482 billion in annual online gross merchandise volume.

While Amazon is a global mega-cap, most of its revenue comes from the United States. Amazon’s revenue is divided into two main sources of income: non-Amazon Web Services and Amazon Web Services.

Amazon’s market capitalization currently makes it one of the largest companies in the world. (See AMZN stock charts on TipRanks)

In addition to e-commerce and e-commerce-related revenues, Amazon also profits from industries like cloud computing and food retail.

I am bullish on Amazon due to its overwhelming competitive advantages, strong growth momentum, and reasonable stock price.

Recent Results

For Q2, Amazon reported a trailing 12-month operating cash flow of $59.3 billion, a 16% increase year-over-year. Free cash flow dropped from $31.9 billion to $12.1 billion over the last year, but this is understandable given Amazon’s aggressive growth investments.

Net sales surged by 27% year-over-year to $113.1 billion, and operating income was up 32.8%. Best of all, net income per share improved by 46.8% year-over-year, reflecting robust growth, and impressive operating leverage for the company.

Amazon’s e-commerce business benefited from continued growth in Prime, as Prime Day saw more than 250 million items purchased in 20 different countries. Amazon Prime recently became available in Portugal, bringing the country count to 22, and Business Prime continues to grow as well.

Amazon’s entertainment business also made progress, as it released a lot of new content during the fiscal year, earning 20 Emmy Award nominations. Prime Video also won streaming deals with the NFL beginning in 2022, as well as the U.K.’s Premier League.

Amazon Web Services continued to generate strong growth, with major new customer commitments and migrations across several industries, including Ferrari (RACE), BMO Financial Group (BMO), Bell Canada (BCE), the National Hockey League, and many others.

Valuation Metrics

Given Amazon’s considerable competitive advantages, and impressive growth momentum, its valuation is looking quite reasonable.

The EV/forward EBITDA multiple still looks a bit high at 22.3, and the price-to-forward-normalized-earnings multiple also appears high at 62.1.

However, the company’s numerous competitive strengths, and expected strong revenue growth (23.3% in 2021 and 18.1% in 2022), and normalized earnings-per-share growth (27.2% in 2021 and 26.8% in 2022), make it look reasonably priced.

Wall Street’s Take

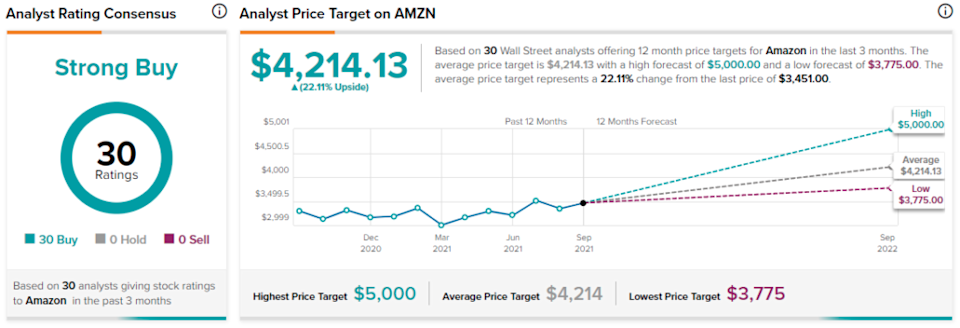

From Wall Street analysts, AMZN comes in as a Strong Buy, based on 30 unanimous Buy ratings. Additionally, the average AMZN price target of $4,214.13 puts upside potential at 22.1%.

Summary and Conclusions

Amazon certainly faces its fair share of challenges today, especially on the regulatory front. There is also concern that founder Jeff Bezos’ recent disengagement from the company, in order to pursue his Blue Origin space business, could cause the company to lose some of its competitive edge.

However, Amazon is showing no signs of letting up, and is likely to see its moat get even wider as data-driven technology advances, providing Amazon with the tools it needs to better leverage its abundance of consumer data.

Furthermore, its stock price looks reasonable right now, and Wall Street is unanimously bullish overall, making it a good time to buy the stock.

Disclosure: On the date of publication, Samuel Smith had no position in any of the companies discussed in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates, and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices or performance.