Investing strategists have been highlighting the importance of owning “quality” companies in the current economic cycle.

But what are quality companies and can their definition be clearly outlined?

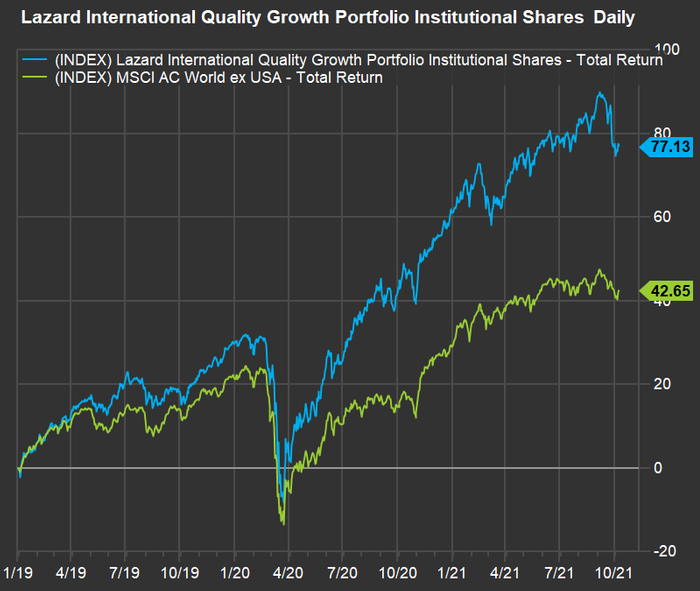

Louis Florentin-Lee and Barnaby Wilson, managing directors of Lazard Management’s International Quality Growth strategy, seem to have done so — and successfully — as you can see on this chart:

FactSet

Florentin-Lee and Wilson, who are based in London, manage about $700 million in the International Quality Growth strategy, with $32 million in the Lazard International Quality Growth Fund

ICMPX,

which follows the same strategy and was established Dec. 31, 2018. The fund’s performance benchmark is the MSCI All Countries World x-USA Index

899901,

The fund managers discuss several stocks held by the fund, below.

From the end of 2018 through Oct. 8, 2021, the fund’s institutional shares returned 77%, while the MSCI All Countries World x-USA Index returned 43%. That is excellent performance for an investment that is completely diversified outside the U.S. (All investment returns in this article include reinvested dividends.)

Investment firms including Blackrock have been touting quality stocks as interest rates rise and the Federal Reserve begins to taper its stimulus. For Blackrock, quality companies have stable cash flows and earnings growth, and can raise prices without squelching demand.

Seeking ‘exceptional businesses’

During an interview, Florentin-Lee explained that the strategy is to hold a portfolio of about 40 “exceptional businesses” for periods of five to 10 years. The managers believe those companies have competitive advantages, including high barriers to entry in a market, strong brands, pricing power and technology.

But the most important selection criteria are driven by the numbers: high returns on capital that are well above the companies’ cost of capital and expected to continue for many years.

“The combination of high returns on capital and reinvestment gives you this beautiful compounding that drives share prices,” Florentin-Lee said.

The reinvestment is essential, Florentin-Lee said, because “the market generally applies the economic law of competition that says supernormal profits attract competition and capital, which ultimately drive returns on capital down.”

He doesn’t believe the phenomenon applies to all companies. “When companies beat the fade, they tend to beat the market,” he added.

So when the strategy’s managers select stocks for the portfolio, based on the recommendations of nearly 100 analysts covering various industries for Lazard, they also try to identify what Florentin-Lee calls “investment opportunities for them to turbo charge their growth,” while maintaining high returns on capital.

Fund holdings

Two in China: Alibaba and Tencent

Given all the concern about China recently, in light of the bond payment default by Evergrande and the regulatory crackdowns on several industries, your first question about the Lazard International Quality Growth Fund might be how much of the portfolio is made up of Chinese companies. Wilson said the fund holds American depositary receipts of Alibaba Group Holding Ltd.

BABA,

and Hong-Kong-listed shares of Tencent Holdings Limited

700,

which together make up about 5% of the portfolio. (For Tencent, the ADR is

TCEHY,

)

Wilson emphasized that the portfolio selections are centered around quality and not exposure to particular countries. When asked about the possibility that the U.S. will force the delisting of Chinese companies over the next three years because of the lack of compliance with the Security and Exchange Commission’s reporting requirements, he said: “I don’t think there is a case where the U.S. investors will lose their value,” because other investors would be ready to buy those shares.

Tencent has a diversified online business, including advertising, cloud services, social media and content distribution. It is the largest distributor of video games in China, which is a concern because of the government’s efforts to limit the amount of time children spend playing games online.

Wilson said the regulatory moves by the Chinese government create volatility for stocks, but that he doesn’t expect much of a detriment to large, diversified companies, such as Tencent and Alibaba. When discussing the video-game regulations meant to reduce activity among children under age 18, he said “this represents low single digits of revenue” for Tencent.

“Arguably, that regulation enhances Tencent’s competitive position,” he said, because the cost of required systems to monitor children’s gaming activity will be spread over a very large revenue base.”

RELX

RELX PLC

REL,

is based in London and has two main business lines. The company publishes medical journals, which account for about 90% of its revenue, according to Florentin-Lee. It also compiles and sells automobile accident data to insurance companies. The fund holds the locally listed shares but they are also listed on the New York Stock Exchange under the ticker RELX

RELX,

The medical-journal publication business is sticky because universities and scientists need them to keep abreast with the latest developments. This also helps RELX maintain a high pre-tax profit margin on this business of about 40%, Forentin-Lee said. He added that the university business is stable because the cost of the journals is a relatively small item for them.

Florentin-Lee said RELX has “the biggest database of claims history for accidents in the U.S.” Any auto insurance company will have its own accident history for its customers, but obtaining information about competitors’ accident claims improves its ability to set prices. In turn, an insurance company that is a client of RELX will provide its own data for RELX’s database.

The pre-tax margin for RELX’s insurance data business is about 35%, Florentin-Lee said. He added that the company is “one of the leading players” in the industry, with Verisk Analytics Inc.

VRSK,

a competitor in the U.S.

Toei Animation

Toei Animation Co. is based in Tokyo and is the leading Japanese animation company with several competitive advantages, according Florentin-Lee. The stock trades in Tokyo under the ticker 4816. One advantage is that its major shareholders include TV Asahi Holdings Corp.

9409,

THDDY,

and Fugi Media, two major broadcasters in Japan.

These broadcasters provide “a platform to attract viewers to create loyalty and following of the characters,” Florentin-Lee said, adding that they also help Toei attract “the best animators.”

He said the bulk of Toei Animation’s profit comes from the licensing of its content, especially in China and in the U.S. One example of a long-lived series, licensed to various media, is Dragon Ball.

This is a niche business, Florentin-Lee said, making competition from media companies with deep pockets unlikely, which should allow Toei Animation to continue operating with “fantastic” profit margins.

Clicks Group

Clicks Group Ltd.

CLS,

is headquartered in Johannesburg and operates a chain of pharmacies that emphasize health and beauty products. The fund holds the locally traded shares and the ADR is CLCGY

CLCGY,

Wilson described a fascinating set of competitive advantages for Clicks. One is the strength of its health and beauty business, which includes its own house brands. Another is that in South Africa, the pharmacy is closely regulated — you cannot open a store within a certain distance of another.

Taiwan Semiconductor

The Lazard International Quality Growth Fund holds ADRs of Taiwan Semiconductor Manufacturing Co.

TSM,

which is a company Wilson believes is “quite misunderstood.”

Most investors focus on the leading-edge of microchip innovation, design and production, Wilson said, and he believes Taiwan Semiconductor is “completely dominant” there.

But the company will go on producing chips long after they are considered leading-edge, with little to no competition, and that accounts for about two-thirds of its revenue, he said. In other words, when TSM comes up with an innovative design and there is no immediate competition, it tends to remain the sole producer of that design for many years.

“We think most investors don’t focus enough on that tail of business they have,” Wilson said.

When asked about the possibility that China takes over Taiwan and what effect it might have on TSM, Wilson said he didn’t think it was in China’s interest to “shoot down the global semiconductor industry.”

Don’t miss: Energy stocks have perked up — here are Wall Street’s favorite sector plays

This post was originally published on Market Watch