Cue the selling again.

Moderna

MRNA,

CEO Stéphane Bancel brought the mood down early Tuesday with a prediction that current COVID-19 vaccines will struggle against the omicron coronavirus variant, due to its high mutations, and that it will take months to mass produce new immunizations.

“There is no world, I think, where [the effectiveness] is the same level…we had with delta,” he told the Financial Times, adding that “all the scientists I’ve talked to…are like ‘this is not going to be good.’”

Initial reports of “mild” symptoms among some South African patients helped cheer markets on Monday. “In reality, the evidence is still incredibly limited on this question, and nothing from the Moderna CEO overnight changes that,” said strategist Jim Reid and his team at Deutsche Bank, whose poll showed just 10% of investors see the variant as a major market threat by year-end.

Indeed, the show must go on, with Wall Street banks continuing to churn out forecasts for the coming year. In our call of the day, JPMorgan predicts a 5,050 finish in 2022 for the S&P 500

SPX,

which matches RBC’s forecast and looks among the most optimistic on Wall Street so far.

Read: Omicron may delay ‘breakout’ performance of these stock trades, RBC says

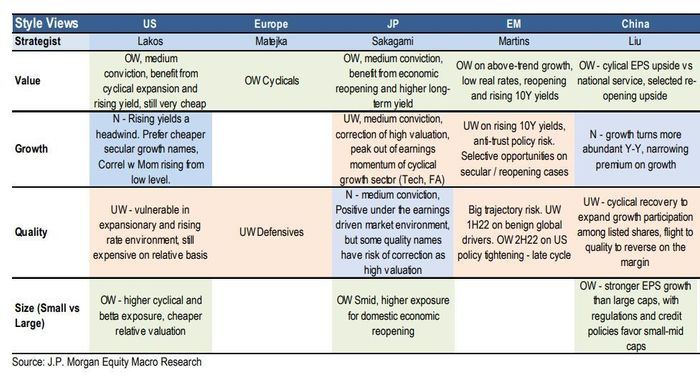

A JPM team led by Dubravko Lakos-Bujas, chief U.S. equity strategist, sees further stock upside ahead, albeit more moderate, on better-than-expected earnings growth, easing supply shocks, improved background on China (which JPM upgraded to overweight on expectations for policy easing and as equity risk premiums from regulatory moves are priced in) and emerging markets, normalizing consumer spending habits and, most important, accommodative central banks.

The team offered some comfort over recent market stress. “While there have been sporadic setbacks with COVID-19 variants (e.g. delta, omicron), this needs to be seen in the context of higher natural and vaccine-acquired immunity, significantly lower mortality, and new antiviral treatments,” said the team, which hammered home the important role of central banks.

“With this in mind, the key risk to our outlook is a hawkish shift in CB [central bank] policy, especially if post-pandemic dislocations persist (e.g. further delay in China reopening, supply-chain issues, labor shortages continue),” said Lakos-Bujas and the team.

The bank sees “broadly accommodative” Federal Reserve policy despite tapering, and especially ahead of next November’s midterm elections, with an extra $1.1 trillion in developed market central bank balance sheet expansion through 2022. It expects “inflation rotation rather than broad-based accelerated in prices,” and sees record corporate liquidity driving capital investment, shareholder returns and mergers and acquisitions.

Most of the upside for U.S. stocks should be seen between now and the first half of 2022, “when monetary and fiscal policy tailwinds will be strongest, followed by sideways action in 2H22,” when Fed liftoff could drive some de-risking and intra-cycle correction.

As for stocks and sectors, the bank likes long equity exposure to rising oil prices (the bank predicts oil prices will hit $150 by 2023), financials, consumer services, healthcare and small-caps. The travel, leisure and experiences theme has “extremely attractive risk-reward, while momentum is “again getting increasingly correlated and crowded with growth stocks,” the bank cautioned.

A few stocks that ended up on its charts included a batch of global beneficiaries of easing supply-chain pressures — Dollar Tree

DLTR,

Tapestry

TPR,

Johnson Controls

JCI,

Masco

MAS,

Under Armour

UAA,

and Tyson Foods

TSN,

Among those that stand to benefit from a global reopening in services are Disney

DIS,

Las Vegas Sands

LVS,

and Expedia

EXPE,

Beneficiaries of higher oil prices include Halliburton

HAL,

Baker Hughes

BKR,

and Occidental Petroleum

OXY,

The markets

Stock futures

YM00,

NQ00,

are pointing to fresh losses for Wall Street, a day after staging a partial comeback from Friday’s meltdown. European stocks

SXXP,

are under pressure, with oil

CL00,

BRN00,

down over 2%, and investors taking shelter in gold

GC00,

the yen

USDJPY,

and bonds

TMUBMUSD10Y,

The buzz

Apart from Moderna, Pfizer

PFE,

CEO Albert Bourla told Bloomberg it would take a few weeks to gather data that will tell whether the omicron strain is more virulent, replicates faster or will overtake the delta strain.

Regeneron

REGN,

said its COVID-19 antibody drug cocktail appears less effective against omicron in initial testing.

Omicron headlines are setting up travel stocks American Airlines

AAL,

United Airlines

UAL,

and Delta Air Lines

DAL,

for another rough day.

In brief remarks prepared for delivery on Tuesday to the Senate Banking Committee, Fed Chair Jerome Powell, who will appear along with Treasury Secretary Janet Yellen, had this to say: “Greater concerns about the virus could reduce people’s willingness to work in person, which would slow progress in the labor market and intensify supply-chain disruptions.”

Investors will also hear from Fed Vice Chair Richard Clarida and Cleveland Fed President Loretta Mester. Data ahead include the S&P Case-Shiller home price index and consumer confidence.

The U.K.’s competition regulator has ordered Facebook parent Meta

FB,

to sell social-media animated images company Giphy over competition concerns.

China’s manufacturing gauge showed a surprise November rebound, and eurozone inflation surged a record 4.9%.

The markets

Elsewhere in commodities, here’s what’s been going on with cocoa prices

CC00,

which have been falling even with deliveries down, point out Commerzbank strategists. Prices hit a four-month low in New York of $2,372 per ton on Monday.

Random reads

It’s no more monarchy for Barbados, as the island country officially becomes a republic.

A TV reporter has been crowned Miss USA.

Meet the new cinnamon roll.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Want more for the day ahead? Sign up for The Barron’s Daily, a morning briefing for investors, including exclusive commentary from Barron’s and MarketWatch writers.

This post was originally published on Market Watch