Over the last five years, the FTSE 250‘s fallen by almost 6%. But one stock in particular has managed to outperform the likes of Alphabet, Apple, and Microsoft.

It’s up 393%, which is enough to turn a £5,000 investment in 2020 into something worth more than £24,000. And the company isn’t involved in artificial intelligence (AI) or even technology.

What’s the stock?

The stock in question is Premier Foods (LSE:PFD) – a manufacturer of both branded and non-branded food products. And there are three reasons the stock’s up so much over the last five years.

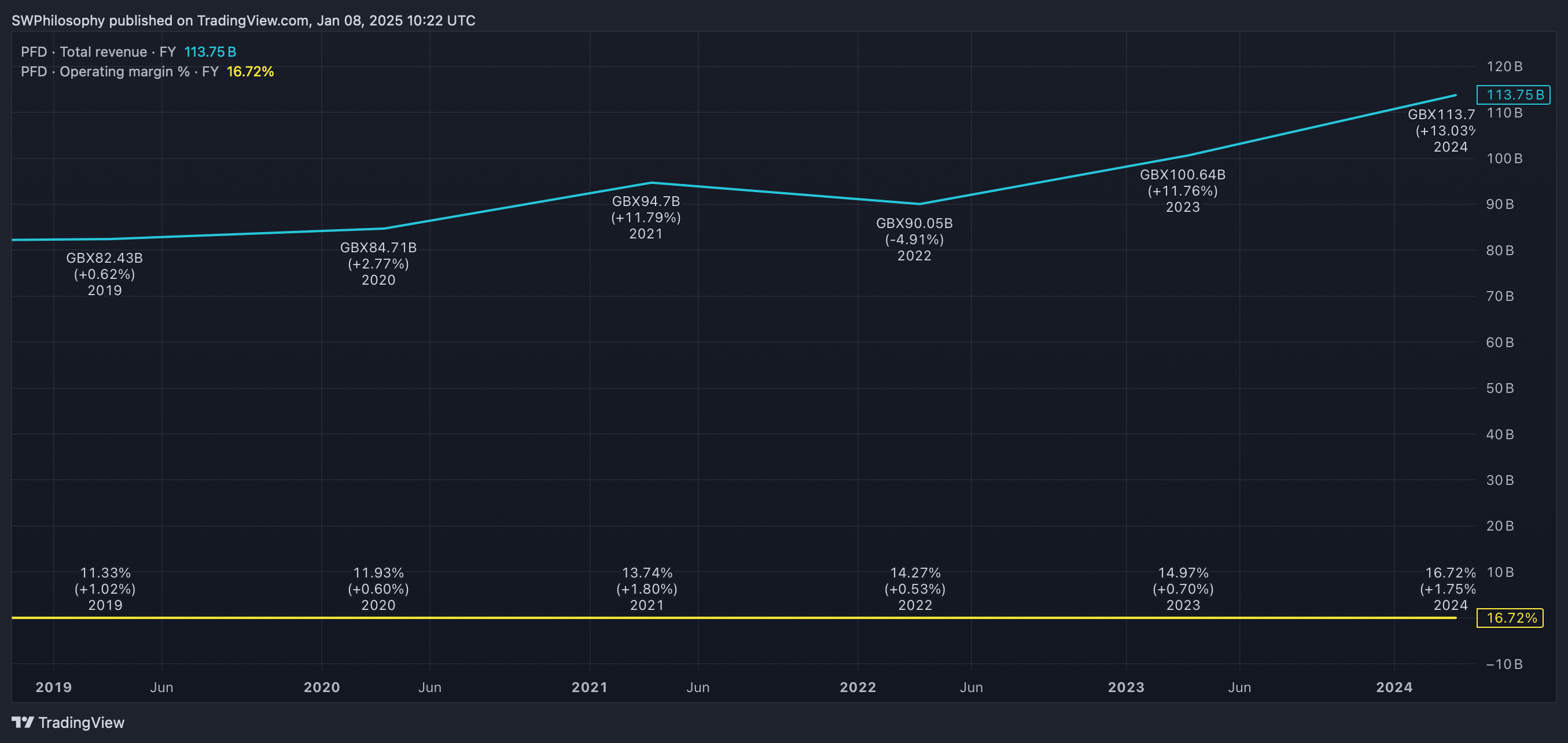

One reason is that revenues have grown. Since 2020, sales are up 35% in the firm’s branded foods division and 16% in its non-branded unit, resulting in overall revenue growth of around 33%.

On top of this, margins have expanded. This is partly due to branded sales growing faster than non-branded ones, but also the result of Premier Foods reducing its long-term debt from £500m to £326m.

Premier Foods Revenue & Operating Margin 2020-24

Created at TradingView

The last reason is the stock now trades at a higher multiple. The firm made a loss in 2019, complicating the price-to-earnings (P/E) ratio. But on a price-to-book (P/B) basis, the stock’s gone from 0.3 to 1.12.

The outstanding returns for investors have therefore been driven by the underlying business as well as the stock market. The big question for investors though, is whether or not it can continue.

Outlook

I think it’s hard to see how shares in Premier Foods can do as well over the next five years as they have over the last five. A number of the catalysts pushing the stock along seem to have worn off.

The firm’s balance sheet is much stronger than it was in 2020 and the stock’s trading at its highest P/B multiple in a decade. As a result, I don’t think either of these is likely to keep pushing the shares higher.

Premier Foods Total Debt & P/B ratio 2020-24

Created at TradingView

Despite this, there are still encouraging signs. In its latest update, Premier Foods reported revenues continuing to climb, with management indicating consumers are trading up to branded products.

As a result, margins are still expanding, leading to headline profits continuing to grow faster than sales. This is being masked to some extent by amortisation costs, but the underlying signs are very positive.

Investors would be unwise to overlook the risk of consumers trading up further – to fresher products. But for the time being, a shift away from non-branded products continues to help Premier Foods.

A missed opportunity?

For me, Premier Foods is something of a missed opportunity. Back in 2020, I anticipated a strengthening balance sheet leading to higher margins and the return of its dividend – but I didn’t invest.

That’s been a big miss on my part. However, with the share price having climbed 393% in the last five years, attempting to make up for the error by buying the stock now might well be a mistake.

I expect Premier Foods to be a durable business going forward. But with some of the major catalysts behind the stock having run their course, I also think there are better opportunities for me at the moment.

This post was originally published on Motley Fool