When I bought Taylor Wimpey (LSE: TW) shares last year, I thought I’d found my perfect FTSE 100 dividend income stock.

They looked fantastic value, trading at around six times earnings, while offering a superb dividend yield of around 6.5%. Better still, the share price looked ready to roll, with consumer price inflation finally in retreat.

I thought peak interest rates would boost Taylor Wimpey in several ways. First, and most obviously, this would cut mortgage rates, boosting buyer demand.

I still love my shares

Second, with inflation on the run, the group’s input costs such as labour and materials would fall, widening margins.

Finally, savings rates and bond yields would slide, encouraging income seekers to take a bit more risk with FTSE 100 stocks like Taylor Wimpey, to generate a superior yield. That would support the share price.

The Taylor Wimpey balance sheet looked surprisingly strong, given the damage inflicted by the pandemic and cost-of-living crisis.

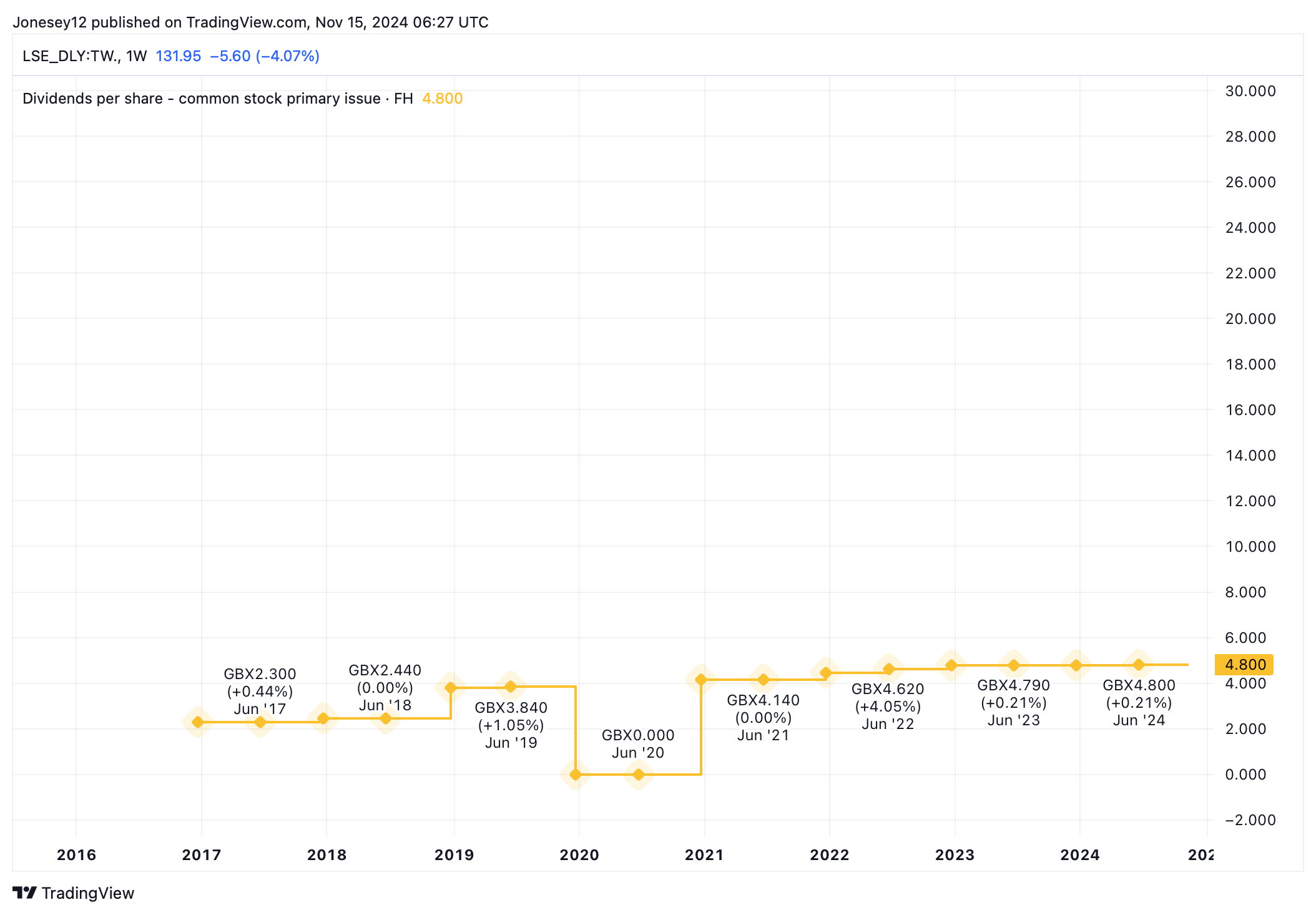

Dividend prospects looked solid too. Apart from the inevitable Covid cut in 2020, the board had made a habit of increasing it slightly every year as this chart shows.

Chart by TradingView

I’ve rarely bought a stock with this much confidence. I enjoyed the experience so much, I bought Taylor Wimpey shares three times in 2023. Just a few months ago I was sitting on a 40% capital gain from the rising share price and had reinvested a few dividends too.

Markets are forward-looking. Interest rates hadn’t actually fallen, but all the anticipated rewards were still coming through. Then suddenly it went wrong.

The share price has slumped by 19.67% in the last three months. It’s up just 6.28% over 12 months. That’s still a total return of around 13%, but it’s way less than I had just a few short weeks ago. Should I turn this short-term volatility to my advantage, by snapping up more stock?

Brilliant buying opportunity? I think so

The main culprit is the Budget, which the Bank of England has warned could increase inflation. That means high interest rates for longer. Labour’s national insurance hike will also drive up staff costs. Taylor Wimpey employs 5,000.

There’s also growing scepticism over whether Labour can hit its ambitious housebuilding targets, and whether builders like Taylor Wimpey are able to scale up and boost completions. Or if they even want to.

On 7 November, the board shrugged off the Budget to maintain full-year outlook as customer demand picked up thanks to falling mortgage rates and improved affordability. Its order book jumped from £1.9bn to £2.2bn. That should have lifted Taylor Wimpey shares but given wider worries, it didn’t.

The stock isn’t as cheap as it was, with a trailing price-to-earnings ratio of 13.28. It still looks pretty good value. The trailing yield is a bumper 7.26%. That’s forecast to hit for 7.42% in 2025. Net debt is down to £84.7m.

Interest rate cut hopes may have dwindled, but I still think Taylor Wimpey shares would be a brilliant buy for me at today’s reduced price. I’d fill my boots if it wasn’t already one of my biggest portfolio holdings.

This post was originally published on Motley Fool