I like buying FTSE 100 companies on a dip and with BT (LSE: BT) shares sliding in recent weeks is it the opportunity I’ve been waiting for?

I’ve been waiting for the right moment to add BT to my portfolio for several years, alerted by a 75% crash in its share price as revenues slipped, management strategies misfired, and net debt headed towards £20bn.

I’ve come close on a few occasions, but never screwed up the courage to click the ‘buy’ button.

So why is this FTSE 100 recovery play falling again?

BT fits the profile of the type of share I like to buy. It’s an established UK blue-chip that’s fallen on hard times but has recovery potential.

It’s cheap, with a price-to-earnings (P/E) ratio of just 7.45, almost exactly half today’s average FTSE 100 P/E of 15.1. Plus it offers a trailing dividend yield of 5.85%, comfortably above the index average of around 3.5%. It’s covered 2.4 times by earnings.

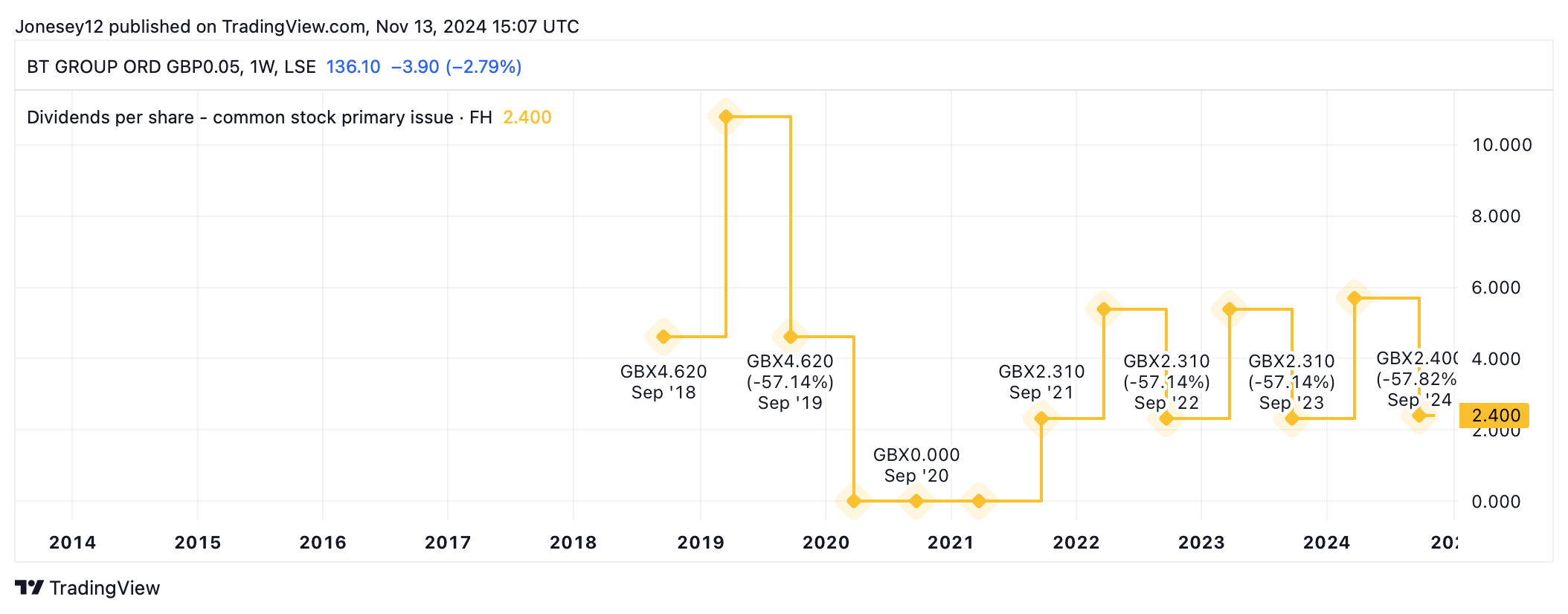

Better still, the dividend looks like it might just be sustainable. While the board suspended shareholder payout during the pandemic, they’ve edged up since, as this chart shows.

Chart by TradingView

Analysts reckon BT shares will yield 5.93% in 2025, and 6.06% in 2026. As ever, dividends aren’t guaranteed but these numbers are tempting.

BT got a lift over the summer when it emerged that two telecoms billionaires were taking a stake in the company – Carlos Slim and Sunil Bharti Mittal. If they had the courage to buy the stock, surely I did?

Yet, I didn’t and I’m glad. On 7 November, BT downgraded its full-year revenue guidance citing weaker non-UK trading a “competitive retail environment”. Interim pre-tax profits slumped 10% to £967m.

High dividends at a low price

The board still hiked its interim dividend by 3.89% to 2.40p as free cash flows jumped 57% to £700m. That was down to higher EBITDA earnings, working capital timing, and a tax refund. CEO Allison Kirkby declared the group is “firmly on track to meet our long-term cost savings and cash flow targets”. Am I feeling brave?

With the market falling generally, the BT share price is down 6.48% over the last week. It’s still up 13.46% over one year, though.

Now here’s the exciting bit, for those who put their faith in broker forecasts. The 12 analysts following BT have set a median one-year share price target of 199.15p. If correct, this would mark a 45% jump from today’s price.

Kirkby still has plenty of challenges, including hitting her target of shedding 55,000 jobs by 2030, streamlining an organisation that has tendency to sprawl, and shrinking that debt pile.

BT may have hit the “inflection point” on Openreach spend but now it has to hold onto its customers. Instead, it seems to be losing out to smaller broadband suppliers.

I resisted the temptation to buy BT shares after the excitement over Slim and Mittal, to give it time to die down. That’s happened now. I’ve screwed up my courage and I’m ready to buy BT shares. All I need now is the cash.

This post was originally published on Motley Fool