If I was starting out as an investor, and only had a small sum at my disposal, I’d consider FTSE 100-listed growth and dividend share Tesco (LSE: TSCO).

It’s the nation’s biggest supermarket. For every £1 the British shoppers spend at the big grocery chains, 28p goes to Tesco, according to analysts Kantar.

Sainsbury’s is the UK’s second most popular grocer but it takes just 15.2p per £1. So there’s a big gap between the winner and runner-up here.

Strength… with risks

If I was starting out, I’d want to buy a stock that was in a run of good form. As I’ve become more experienced, I’ve made a habit of targeting struggling companies in the hope their shares will power on when they sort themselves out.

That’s no strategy for an absolute beginner. The Tesco share price certainly isn’t struggling. It’s up 27.83% over the last 12 months, easily beating the FTSE 100 average return of 11.36%. This isn’t just a flash in the pan, either. Over five years, Tesco is up 45.81%.

Past performance is no guide to the future. For the Tesco share price to rise further, it will have to continue boosting sales and profits, and keep a lid on costs.

It faces a new challenge after yesterday’s (30 October) Autumn Budget, which saw chancellor Rachel Reeves hiked employers’ national insurance contributions. This will hit Tesco harder than most, as it now employs 326,000.

This stock looks good value

Paying extra NI will squeeze margins, which are already wafer thin at 4.1%. Given the competitive nature of the UK grocery market, it may struggle to pass them on to customers. On the other hand, rivals Sainsbury’s, Asda, Morrisons, Aldi and Lidl also have big staff rosters and now face exactly the same challenge.

I’m hoping Tesco’s revenues pick up as the cost-of-living crisis eases. If interest rates start to fall, that should put money into shoppers’ pockets. But there are no guarantees this rosy scenario will pan out.

I wouldn’t want to overpay for my first stock. Despite their strong recent run, Tesco shares are valued at a modest 14.71 times earnings. That’s just below the average FTSE 100 price-to-earnings ratio of 15.4 times.

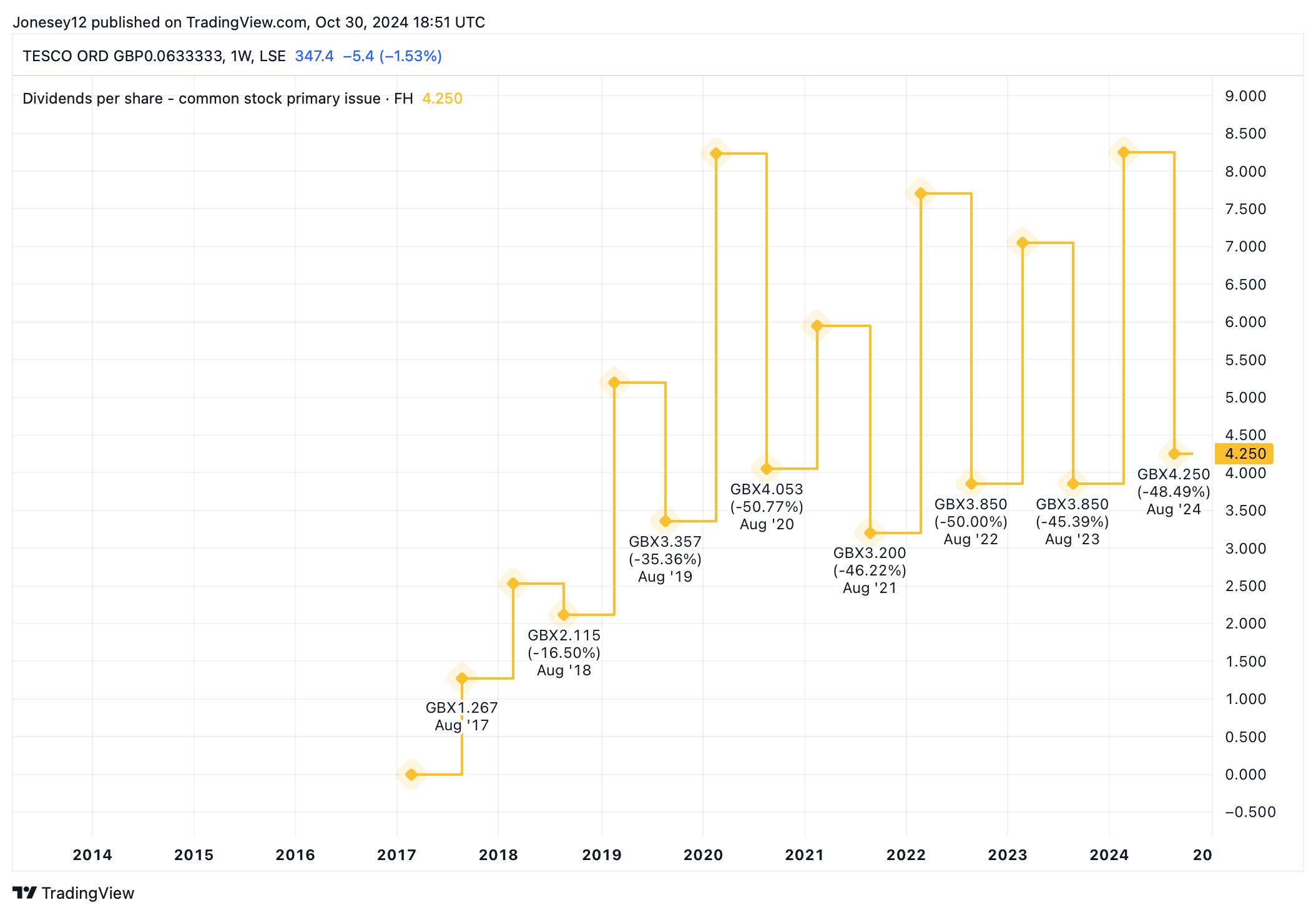

Tesco shares have a trailing yield of 3.71%, a fraction above the 3.5% index average. It’s comfortably covered twice by earnings. When I look for a stock, I’d like to see a nice track record of dividend growth. I’ll admit the Tesco’s has been patchy lately, as this chart shows.

Chart by TradingView

I only buy shares that I plan to hold it for at least five years and ideally a lot longer. Over such a timescale, Tesco will inevitably suffer ups and downs. It’s struggled before, notably under the tenure of Philip Clarke, but bounced back after Dave Lewis replaced him in 2014. Tesco has shown bags of resilience. And that’s why it feels like a solid place to invest my hypothetical first £1,000.

This post was originally published on Motley Fool